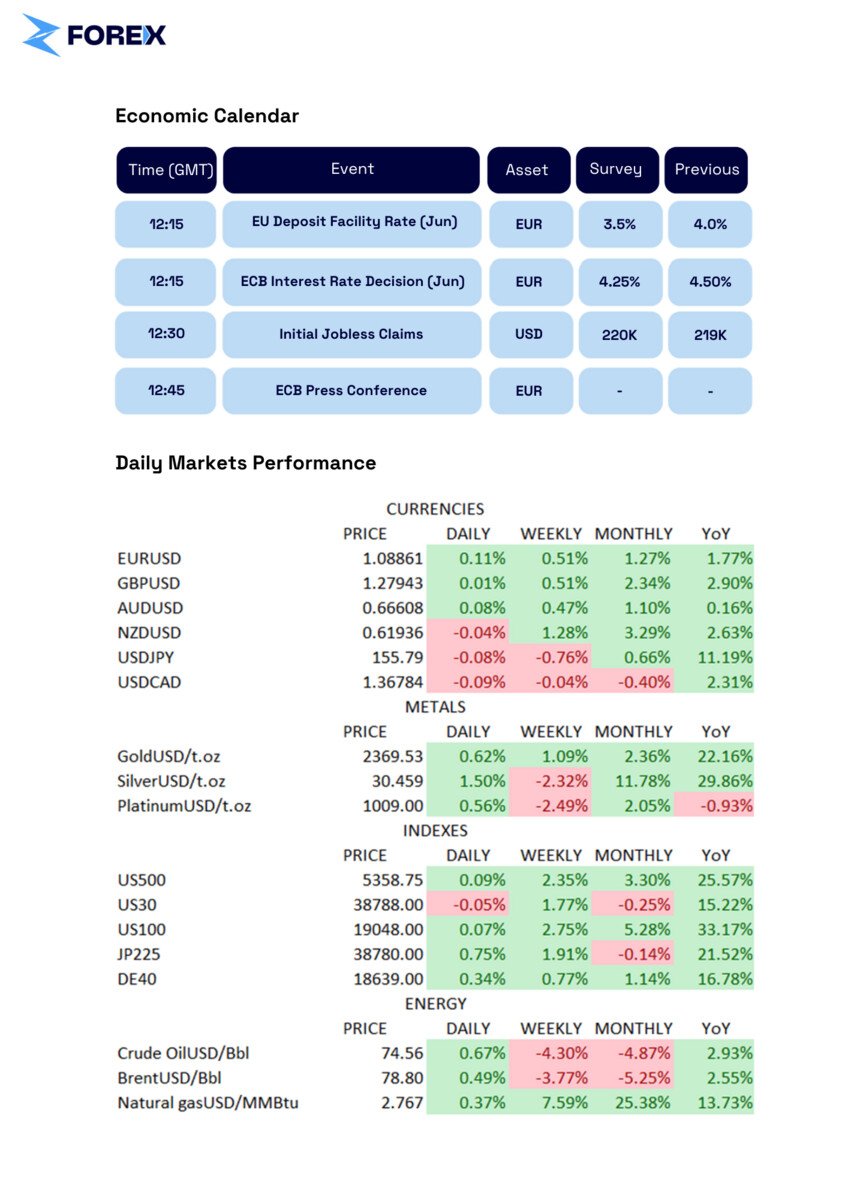

Daily Analysis by zForex Research Team - 06.04.2024

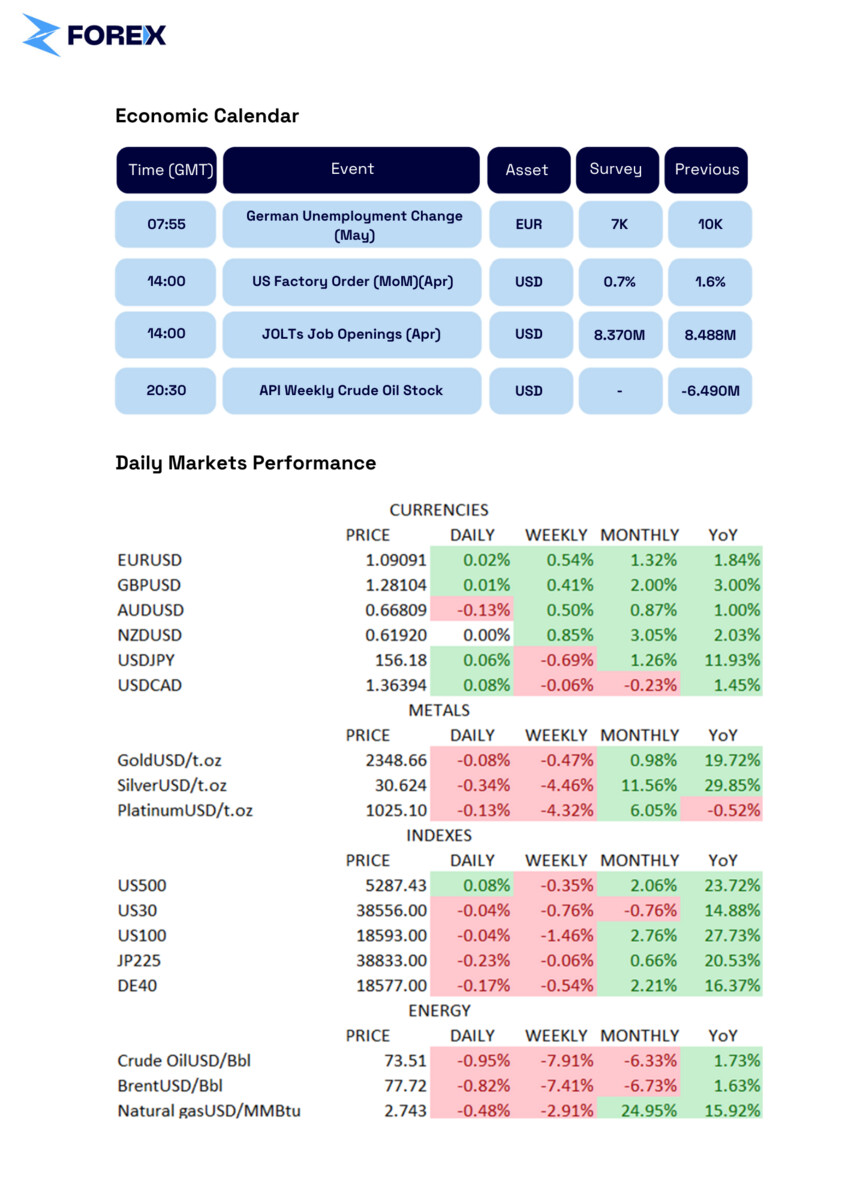

On Tuesday, the dollar index remained steady at around 104, marking its lowest level in almost two months. This drop was fueled by indications of economic weakness in the US, bolstering expectations for Federal Reserve interest rate cuts. Despite forecasts for a slight improvement, data released on Monday revealed a further contraction in US manufacturing activity in May. Consequently, market sentiment shifted, with the probability of a Fed rate cut in September rising to approximately 52%, compared to about 42% on Friday. Investors are now eagerly awaiting key economic reports scheduled for later this week, including the ISM Services PMI, JOLTS Job Openings, and the highly anticipated monthly jobs report, for additional guidance. Additionally, markets are anticipating the European Central Bank’s policy decision on Thursday, with expectations leaning toward rate reductions. While the dollar remained at multi-month lows against most major currencies, it only experienced modest declines against the Australian dollar and Japanese yen, trading at two-week lows.

Gold prices remained steady at around $2,348 per ounce, following gains in the previous session, supported by increasing expectations of relaxed monetary policies from major central banks. Monday’s data revealed a second consecutive slowdown in US manufacturing activity in May, alongside an unexpected decline in construction spending for April, primarily driven by drops in non-residential activity. These developments fueled speculation that the Federal Reserve has the flexibility to implement rate cuts later this year. Currently, traders are estimating a 52% likelihood of a rate cut in September, according to the CME FedWatch tool. Simultaneously, the European Central Bank is anticipated to lower interest rates this week, with similar expectations for easing policies from the Bank of Canada and the People’s Bank of China. Investors are now awaiting Wednesday’s ADP employment report and Friday’s non-farm payrolls data to gauge the health of the US economy and its potential impact on the Fed’s policy trajectory.

On Tuesday, WTI crude futures dropped below $74 per barrel, marking their fifth consecutive decline to the lowest level in four months amidst concerns about a potential increase in global supply later in the year. OPEC+ reached an agreement on Sunday to extend most of their supply cuts into 2025 but introduced the possibility of gradual unwinding of voluntary cuts from eight member countries starting in October. It is anticipated that over 500,000 barrels per day will re-enter the market by December, with a total of 1.8 million barrels per day returning by June 2025. Additionally, signs of economic weakness in the United States, the world’s largest oil consumer, added pressure to oil prices after US manufacturing activity continued to contract in May. Furthermore, recent fears that the US Federal Reserve may refrain from cutting interest rates this year have further weighed on oil markets, potentially slowing economic growth and reducing oil demand.