One thing I disagreed with in Smith’s book was actually taking time off if you’re in a drawdown. Noting the date of which you posted this, taking time off may have meant that you missed the huge moves seen in JPY pairs; one thing Richard Dennis (founder of the Turtles) was big about was trading through the drawdowns, as one big trade could mean the difference between profit and loss for the entire year.

You are right. Making backtest on various pairs found that after a lossing streak there is a huge win that erases all losers and generates profit.

This technique should be traded without a pause if one aims to get profit.

By the way, I’m doing backtest on all the 28 pairs and gold and silver for 6 years. When i finish i will place the results. So far eurusd gave about 30% in 6 years, that is about 5% per year and gbpusd about 1% per year.

Great! I’d love to see it. I just went through a 5 year E/U backtest on the 55/20 breakouts (using all enhancements), and I’m showing a gain of 3168 pips starting from 1/1/2008 until present, with a win rate of 39%. Breakdown:

Obviously this backtest didn’t show account equity progression, but it should show that even in a profitable method, there may be losing years (2009 and 2011). In fact, 2009 and 2011 would have been much worse had the rejection rule, last bar technique, and Bishop not been used. I still haven’t done this for Conqueror or Trend Analysis entries, but it does appear that you would have gotten into significant trends earlier.

Ah, well that makes sense. I actually abandoned C.S/Turtle settings of 55/20 and went back to 20/10, aka the Turtle short term system. This performs much better imo and the backtesting I’ve done so far supports it.

20/10 with rejection rule, Bishop and last or double last bar entry is the best system I’ve encountered yet.

Trend Analysis is a nice approach but it will sometimes miss the great trends because the swings don’t set up right. Conqueror is to jumpy for me, it does what Channel Breakout does, only less well imho.

In the beginning I traded four systems, Ichimoku, Channel BO, Trend Analysis and Conqueror, but now I find that Channel BO makes the others superfluous and I save time and confusion by just focusing on that and nothing else.

So, if you have the extra time, I suggest you test with 20/10 settings and see what results that would yield compared to what you got with 55/20.

I’m doing the rules almost flawless, only thing I’m using “different” is the decision for last bar. Because it is not well defined how to chose a last bar, I’m using previous swing low/high (2 score).

Thanks for the tip, I’ll have a look at that when I get a chance.

I will say one thing, however: Contrary to the heater it’s been on the past several months, 55/20 breakout is a losing strategy for the past 5 years on USD/JPY. I’ll have to run the numbers with 20/10.

Alright, so I just got finished backtesting 20/10 breakouts with full rules on EUR/USD. As o990l6mh said, it has significantly outperformed 55/20 in the last 5 years. I haven’t yet backtested on other pairs. Here’s the breakdown:

2008: +1879

2009: +353

2010: +1580

2011: +566

2012: -395

2013 (up to the last closed trade): +203

Total pips: +4186

This was a 32% increase in total system performance, though I can’t yet say if 55/20 combined with Conqueror and Trend Analysis would have yielded better results. I was happy to see 2009 and 2011 turn into profitable years, though 2012 ended up getting chopped up pretty heavily using the 20/10 breakout, though the rejection rule saved the day several times. 2013 is already looking very nice though, with a settled +203 in the bank, plus another ~450 pips in floating profit out there now that hasn’t yet closed.

IBFX demo account. Full disclosure, this was all manually done on the daily timeframe. Everyone should do his or her own backtest. I intend to backtest each pair that I trade live, at least back 5 years.

To add, USD/JPY performs poorly with a 20/10 breakout as well, though it does turn the unprofitable 55/20 into a barely profitable system on that pair.

The process of backtesting is slow and tedious. The first problem is to download all the historical data (quality data). I’m still downloading that data! That is sloooooow! but the data is from 2007, so it could be a 6 year backtesting

In my fast backtests on various pairs for 1 year data I found that 55/20 is not profitable on various pairs, but it is on others. For example, EURUSD works good, but GBPUSD not.

GBP/USD 20/10 with all rules (except ADX filter; I haven’t found that to be significant, sorry!):

2008: +1384

2009: -475

2010: +907

2011: +1273

2012: -21

2013 (until the last closed trade): +771

Total: +3839

Some whipsaw in 2009 particularly, but overall acceptably profitable over the 5 year period tested. One thing to note was that the Rejection Rule was absolutely crucial in pulling a profit out of this pair. I’ve been testing with continual monitoring of the Rejection Rule, i.e. liquidating a trade at any time the market flattens out for 5 or more days and has a failed breakout. This allowed you to get out at the exact bottom or top of the trend several times.

No problem. Just to be clear, this was a backtest of a 20/10 channel; it’s plausible for the 55/20 to be unprofitable during the same period. I know, not exactly “by the book,” but o990l6mh got me looking at it. From my backtesting so far, 20/10 breakouts with Smith’s rules (with the exception of ADX Filter) far outperforms 55/20.

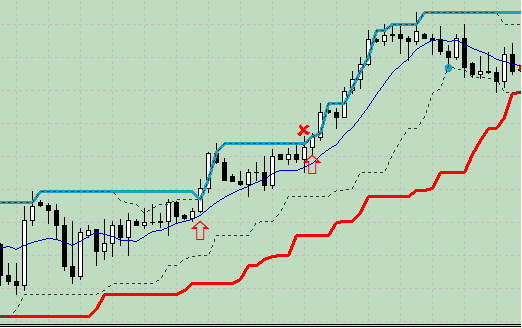

Here’s how I’ve been applying the Rejection Rule:

We go long at the break of the 20 day high (or 55, no matter) at the first red up arrow. The market follows through nicely until selling off and chopping sideways for 10 days. On the 11th day (marked with a red X), the market breaks up through the level of the new 20 day high, but closes below it. Because we had at least a 5 day period of a flat channel (descending would count too, of course), the Rejection Rule activates, and we liquidate the position at the close for a tidy profit.

The next day, the market breaks above the high of that rejected candle, which signals another long entry. We ride it until being taken out by the 10-day low (blue dot).

Not sure if that’s any different than how others are using the Rejection Rule, but this is simply how I read it.

Placement of the Last Bar for me is completely unscientific; I simply use the last “significant” bar before the breakout. I have been noticing that this seems to be around 1x the 40-day ATR.

It’s hard to put it concretely, but I’ve been noticing that my definition of “significant” seems to put the protective stop roughly 1x the 40-bar ATR from the entry price, yes.

No it wasn’t, but that’s something I may very well go back through and check on. My testing was nothing fancy, i.e. no short-term trades such as RRR and Inside Day. This was a plain vanilla 20/10 channel breakout using the Rejection Rule, Last Bar technique, and Bishop.