Dollar Stays Strong as Job Market Data Looms

On Thursday, the dollar index maintained its position above 104, with investors taking a cautious approach. They are waiting for the upcoming monthly jobs report, which is anticipated to offer new insights into the current state of the US labor market. The report, due on Friday, is expected to reveal an increase in employment by 170,000 in November. Additionally, it’s predicted that the unemployment rate will stay at a 22-month peak of 3.9%, and wage growth might slow down to 4%, marking the lowest since June 2021.

Recent data presents a mixed picture. Wednesday’s figures suggested a slowdown in the US labor market, with the ADP report showing fewer job additions in November than anticipated, and labor costs in the third quarter being lower than expected. Despite these indications of a cooling labor market, the dollar has stayed near its highest levels in almost three weeks. This resilience is partly due to traders increasing their bets on rate cuts by other central banks. Currently, the market is pricing in about an 85% likelihood of the European Central Bank cutting rates in March 2024.

Gold Technical Analysis

Gold has been stabilizing its price above the Ichimoku cloud as expected. The pair is currently trading in a narrow range between $2,009 and $2,039. The direction and magnitude of the next breakout are crucial for the future trend.

If the XAUUSD price breaks above the upper boundary of the range, the bulls will have a clear path to the 23.6% resistance level at $2,078.

On the other hand, if the price falls below the lower boundary of the range, the bears will try to push it back into the Ichimoku cloud and test the support level at $1,984. The market sentiment and the global economic outlook will likely influence the price movement of gold in the coming days.

Cotton Futures Reach New Heights Amid Supply Concerns

Cotton futures recently hit a high not seen in over a month, climbing above 82 cents per pound. This surge, the most significant since late October, comes as traders face concerns over the short-term availability of cotton. Recent data from ICE reveals a sharp decline in certified cotton stocks. On December 5th, stocks available for delivery against futures contracts were at just 6,325 bales, a significant drop from the two-year high of 87,770 bales recorded on December 1st.

Adding to these supply worries, the Cotton Association of India (CAI) has lowered its forecast for the 2023/2024 cotton season’s production to 29.4 million bales. This downward revision is due to the impact of the pink bollworm infestation in Haryana and the fact that many farmers have been forced to uproot their plants.

In other developments, Brazil reported its cotton export figures for November. The country shipped 253.71 thousand tons of cotton, indicating a 12% increase from October 2023. However, this figure represents a 5.5% decrease when compared to the exports in November 2022.

Post-Strike Surge: US Adds 180,000 Jobs in November

In November 2023, it’s expected that the US economy experienced a notable upturn in job growth, primarily due to the conclusion of strikes in the automotive and entertainment sectors. It’s estimated that around 180,000 jobs were added, a significant increase from the 150,000 jobs in October. This change can be largely attributed to the return of workers from the United Automobile Workers (UAW) and the Screen Actors Guild‐American Federation of Television and Radio Artists (SAG-AFTRA) after strike settlements.

Despite this improvement, there’s an observable trend of deceleration in the job market. For the second month in a row, the number of jobs added has been below the average monthly increase of approximately 258,800 seen over the previous year, indicating a slowdown. Nevertheless, it’s important to recognize that job growth is still surpassing the monthly requirement of 70,000 to 100,000 jobs necessary to keep pace with the growing working-age population.

On another note, the unemployment rate is projected to be around 3.9%, which is the highest it has been since January 2022. Additionally, there’s an anticipated decrease in annual wage growth, possibly dropping to 4%, the lowest since June 2021. This suggests a complex scenario in the labor market, where job growth persists amidst a backdrop of declining wage increases and a slight rise in unemployment.

EURUSD Dips Slightly, Future Projections Indicate Decrease

On Friday, December 8, the EURUSD pair saw a slight decline, dropping by 0.0008 or 0.07%, to close at 1.0784. This was a marginal decrease from its previous trading session’s level of 1.0792.

Analysts and global macro models from Solid ECN Security are projecting that the Euro to US Dollar exchange rate, commonly referred to as EUR/USD, will hover around 1.07 by the end of the current quarter. As we look ahead, our forecasts extend to 12 months, where we anticipate the exchange rate might further decrease to around 1.04.

DXY Edges Up, Future Projections Show Increase

On Friday, December 8, there was a small rise in the DXY, with an increase of 0.1831 or 0.18%, bringing it to 103.72. This marked a slight upturn from its previous level of 103.54 recorded in the last trading session.

Projections from Solid ECN, based on our global macro models and analysts’ expectations, suggest that the United States Dollar could reach around 104.29 by the end of this quarter. Peering further into the future, our forecasts indicate that in 12 months’ time, the Dollar might increase to approximately 107.58.

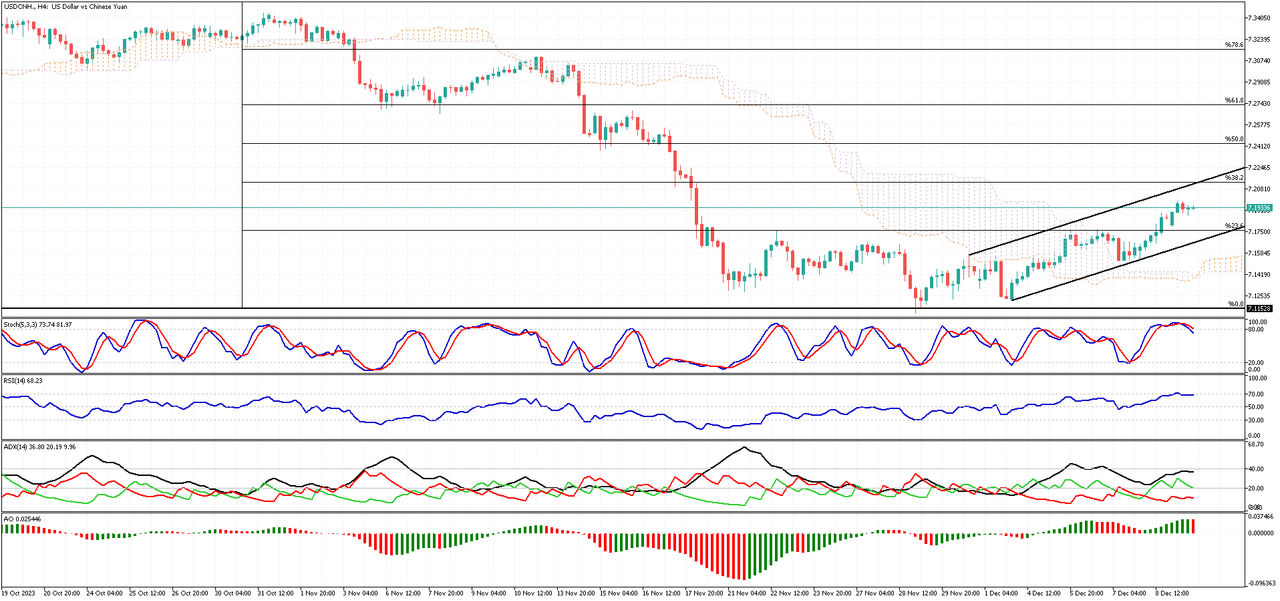

Chinese Yuan Expected to Strengthen in Coming Months

On Friday, December 8, there was a slight uptick in the USDCNY, with the rate increasing by 0.0062 or 0.09%, ending the day at 7.169. This rise was a small change from its previous closing of 7.163 in the last trading session.

Looking ahead, based on the insights from global macro models and the expectations of analysts, the Chinese Yuan is projected to reach about 7.19 by the end of this quarter. Moving further into the future, predictions suggest that in a year’s time, the Yuan could be trading around the 7.38 mark.

GBPUSD Sees Slight Decline, Predicted to Lower Further

On Friday, December 8, the GBPUSD experienced a modest decrease, dropping 0.0046 or 0.37% to close at 1.2544, down from 1.2590 in the previous trading session. This shift reflects a slight downward trend in the currency pair.

It is anticipated that the British Pound will trade around the 1.25 mark by the end of the current quarter. Extending the outlook further, over the next 12 months, the Pound is estimated to potentially trade at around 1.20.

Bitcoin’s Steady Rise: December 9th Update

On Saturday, December 9th, the value of Bitcoin in US Dollars was 44,193, showing a small rise of 33 or 0.07% from the last trading session. Over the past month, Bitcoin’s value increased by 18.51%. If we look at the past year, it went up by 157.98%.

Predictions suggest that by the end of this quarter, the price of Bitcoin in US Dollars might decrease to 37,157 and further drop to 30,991 in a year, as per projections from global macro models and what experts anticipate.

China Experiences Steepest Food Price Fall Since 2021

In November 2023, the cost of food in China experienced a notable decrease, dropping by 4.2% compared to the same time last year. This decrease in food prices was more significant than the 4.0% drop observed in the previous month. In fact, this trend of falling food prices has been ongoing for five consecutive months, marking the most rapid decline since September 2021.

A key factor in this decline was the dramatic fall in pork prices, which went down by 31.8%, surpassing the 30.1% decrease seen in October. This larger drop in pork prices was unexpected and is thought to be due to a combination of unusually warm winter weather and a continued adequate supply following the Golden Week holiday in early October. In addition to pork, other food items also saw price reductions, including cooking oils (down by 4.1%), eggs (decreasing by 8.8%), and milk (a slight decrease of 0.3%).

However, not all food categories followed this downward trend. Fresh vegetables, for example, saw a slight increase in price (0.6%), reversing the previous month’s decline of 3.8%. Similarly, the cost of fresh fruit accelerated, with prices rising by 2.7% compared to a 2.2% increase in the previous month.

In terms of the economic impact, this trend of falling food prices can have mixed effects. On one hand, lower food prices can benefit consumers by reducing their living expenses, potentially increasing their disposable income and encouraging spending in other sectors. On the other hand, for producers and farmers, falling prices can reduce income and profitability, possibly leading to challenges in the agricultural sector. Overall, the impact on the economy would depend on the balance between these consumer and producer effects.

Egypt’s Inflation Eases, Food Prices Slow Down

In November 2023, Egypt saw its annual urban inflation rate decline for the second consecutive month, reaching a six-month low at 34.60%. This decrease from October’s 35.8% rate follows a record peak in September of 38.0%. The current rate remains well above the Egyptian central bank’s target range of 5-9%, yet it still surpasses the anticipated market forecast of 34.8%. A contributing factor to this development is the reduced pace of food inflation, which fell to 64.5% from 71.3% in October. On a monthly basis, consumer prices experienced a 1.3% increase, a slight acceleration compared to October’s 1.0% rise, which was the most modest in over a year.

Turkey Sees Lowest Unemployment Rate in 11 Years

Turkey’s unemployment rate fell to 8.5 percent in October 2023, the lowest level in 11 years. It was 9.1 percent in September 2023. More people found jobs in October 2023, as the number of employed people increased by 246 thousand to 31.835 million. At the same time, the number of people without jobs decreased by 163 thousand to 2.961 million. The jobless rate was lower for men (7.0 percent) than for women (11.3 percent). More people also joined the labor force, as the labor force participation rate rose slightly to 53.1 percent from 53.0 percent in September 2023. The employment rate also improved to 48.5 percent from 48.2 percent. Moreover, the unemployment rate for young people aged 15-24 years went down to 16.3 percent from 16.7 percent.

Impact of US Jobs Report on Australian Currency

The value of the Australian dollar recently dropped to approximately $0.655. This change was largely influenced by a strong jobs report from the United States. In November, the US reported an increase in nonfarm payrolls by 199,000 jobs, which was more than the expected 180,000. Additionally, the unemployment rate in the US decreased slightly to 3.7%, and wages grew unexpectedly. This combination of factors has led to a boost in the US dollar (USD).

Why the Aussie Dollar Weakened

This weakening of the Australian dollar, often referred to as the “Aussie,” was also affected by decisions made by the Reserve Bank of Australia (RBA). The RBA decided to keep its policy rate steady at 4.35%. This decision was anticipated and is seen as a way for the RBA to take time and evaluate how previous interest rate increases are influencing the economy, particularly in terms of demand, inflation, and employment.

The RBA has expressed some uncertainty about future household spending. However, it has also noted that inflation is becoming more moderate and that there are signs of the job market becoming less tight.

Australia’s Economic Growth

Regarding Australia’s economic performance, there was a slight increase of 0.2% in the economy in the third quarter. This growth was less than the forecasted 0.4%, marking it as the slowest growth Australia has seen in a year.

Yen Falls as Dollar Strengthens, BOJ Policy in Focus

The value of the Japanese yen has recently seen a significant decline, falling beyond 145 against the US dollar. This change comes after a period of strength for the yen, which had reached a four-month peak. The shift is primarily due to the robustness of the US dollar, bolstered by unexpectedly strong job data from the United States. This information has altered perceptions, with many now doubting that the US Federal Reserve will reduce interest rates in the early part of 2024.

Furthermore, there’s been a decrease in expectations for interest rate increases by the Bank of Japan, especially as the bank’s monetary policy decision looms on the horizon. Just a week ago, the yen had experienced a surge, jumping by 3.5% to reach about 141.7 against the dollar. This increase was fueled by remarks from Bank of Japan Governor Kazuo Ueda, who hinted that the bank might end its negative interest-rate policy sooner than expected.

In a recent statement to the parliament, Governor Ueda mentioned the potential adjustments in short-term rates, dependent on the prevailing economic and financial circumstances. He indicated that the rates could shift from zero to 0.1%, and eventually to 0.25% or 0.50%. However, he also made it clear that Japan is yet to witness a sustainable increase in inflation that is driven by growth in wages.

Analyzing the Recent Drop in Offshore Yuan Against the Dollar

The offshore yuan has recently experienced a notable decline, reaching around 7.20 against the US dollar. This represents its lowest level in three weeks. The primary reason for this drop is the ongoing deflationary pressures in China, indicating that the country’s economy is grappling with reduced domestic demand.

Economic Data and Its Implications

Recent statistics released over the weekend have highlighted this economic challenge. Consumer prices in China fell by 0.5% year-on-year in November, a more significant decrease than October’s 0.2% drop and below the expected 0.1% decline. Additionally, producer prices witnessed a 3% fall last month. This marks the 14th consecutive month of decline in the Producer Price Index (PPI) and is the most rapid drop since August.

These figures are critical as they reflect the purchasing trends and production costs within the economy. Persistent deflationary pressures can indicate an economic slowdown, as falling prices often lead to decreased consumer spending and business investment.

Future Economic Indicators and External Influences

Investors are now turning their attention to upcoming economic data and the loan prime rate decisions from China’s central bank, which will provide further insights into the economic trajectory. Externally, the yuan is also feeling the impact of a globally strong US dollar. This strength is partly due to unexpectedly robust US jobs data, which suggests that the Federal Reserve might not reduce interest rates as soon as previously thought, in March 2024.

Impact on the Economy

This situation presents a mixed bag for China’s economy. On one hand, a weaker yuan can make Chinese exports more competitive on the global market. However, persistent deflation and reduced domestic demand can hinder economic growth and stability. Moreover, the interplay between domestic economic challenges and external pressures like the strong US dollar creates a complex environment for monetary policy decisions.

Wall Street Braces for Fed Meeting and CPI Data

On Monday, Wall Street’s primary indexes displayed a muted demeanor as investors’ focus turned to significant upcoming events: the Federal Reserve’s interest rate meeting and the U.S. inflation report, both due later in the week. The general market sentiment suggests that a halt in rate hikes is already factored into current prices. However, investors are vigilantly looking for clues about when the Fed might adjust interest rates in the upcoming year.

Inflation Data and Its Impact

The Consumer Price Index (CPI) report, scheduled for release just before the Fed meeting, is crucial as it provides insights into inflation trends. For November, it is anticipated that the headline inflation figures will show no significant change. Such data is vital as it influences the Federal Reserve’s decision-making regarding monetary policy, which in turn affects the economy’s overall health.

Individual Stock Movements

In the realm of individual stocks, Macy’s witnessed a 16% surge after an investor group proposed a $5.8 billion bid to privatize the department store chain. In parallel, health insurer Cigna’s shares climbed 14%. This increase came after the company decided against acquiring its competitor Humana and instead announced a massive $10 billion share repurchase program.

Index Performance and Economic Outlook

As for the broader market indices, the S&P 500 slightly declined by 0.1%, settling at 4,600 points. Meanwhile, the Dow Jones Industrial Average and the Nasdaq Composite showed minimal changes. This subdued activity follows a recent surge that had driven these indices to their highest points since early 2022.

Assessment of the Market Scenario

This cautious approach in the stock market reflects investor sensitivity to macroeconomic indicators and policy decisions. While individual stock movements like Macy’s and Cigna’s provide short-term trading opportunities, the broader market’s performance is more indicative of economic confidence. A stable or declining inflation rate can signal a healthier economic environment, potentially leading to more robust stock market performance in the long term.

Economic Forces Behind the Fluctuating Canadian Dollar

The Canadian dollar has seen a decline in value, reaching around 1.36 against the US dollar. This trend emerges as the strengthening of the US dollar counterbalances the positive effects of recovering oil prices.

Impact of US Economic Data

The US dollar’s strength was bolstered by a jobs report that surpassed expectations. This robust jobs data gives the Federal Reserve room to possibly delay any cuts in interest rates, which in turn supports the value of the US dollar. When the US dollar strengthens, it often leads to a relative depreciation of other currencies, like the Canadian dollar in this case.

Recovery in Oil Prices

Concurrently, there’s been a slight uptick in oil prices towards the end of the week. As a major oil exporter, Canada’s economy and the value of its currency, often referred to as the “loonie,” are influenced by changes in oil prices. The recent recovery in oil prices can potentially boost foreign exchange inflows into Canada, offering some support to the Canadian dollar.

Bank of Canada’s Stance

On the domestic front, the Bank of Canada has indicated a leaning towards increasing interest rates in the future. Governor Tiff Macklem has pointed out that the current economic climate, especially with inflation running significantly above the desired level, does not warrant loosening monetary policies.

Economic Implications

The interplay between the Canadian dollar’s value, oil prices, and monetary policy decisions is a complex one. A weaker Canadian dollar can make Canadian exports more competitive, potentially boosting sectors like manufacturing. However, it also means higher costs for imports, which could contribute to inflationary pressures.

The Bank of Canada’s potential interest rate hike can be seen as a response to control inflation. Higher interest rates can cool down an overheated economy, but they also run the risk of slowing down economic growth.

@SOLIDECN - could you respond to the questions so repeatedly asked of you in this thread ?

Ignoring them and producing irrelevant “information” that doiesn’t answer them won’t make them go away.

That approach really doesn’t speak at all well of your honesty or integrity.

People both here and in other forums are now increasingly pointing this out and my guess is that that process won’t stop until you show some honesty and integrity in your responses to what are totally legitimate, obvious and simple questions.

https://www.wikifx.com/en/dealer/3668502333.html

2 Likes

Analyzing the Recent Depreciation of the Mexican Peso

The Mexican peso has recently experienced a decline in value, now trading beyond the 17.4 mark against the US dollar. This level is close to the lowest it has been since the early days of November. This trend appears to be a reaction to the latest signs of disinflation in Mexico, which is influencing market expectations about the monetary policy stance of the Banco de México (Banxico), Mexico’s central bank.

A closer look at the economic data reveals some shifts. Mexico’s Producer Price Index (PPI), which measures the average changes in prices received by domestic producers for their output, increased by 1.20% year-on-year in November. This rate is a tad lower than the 1.30% seen in the previous month. Moreover, there was a month-over-month change, moving from a 0.5% increase in October to a 0.4% decrease in November.

In terms of core inflation, which is often used as a gauge for underlying long-term inflation trends in an economy, the numbers came in at 5.3% for November. This figure is lower than expected and represents a slowdown from the 5.5% recorded in the previous month.

Banxico’s Response

These developments are in line with recent comments from Banxico’s Governor Victoria Rodriguez Ceja and Deputy Governor Jonathan Heath. They have indicated that the central bank might ease its policies if the trend of disinflation continues, which could lessen the support for the Mexican peso.

Market Anticipation and Outlook

Traders and investors are now keenly awaiting the upcoming policy decisions from both the Federal Reserve and Banxico. The general expectation is that both will keep borrowing costs restrictive. However, there is some uncertainty regarding the tone and approach the officials will take moving forward.

Tuesday’s Triumph: FTSE 100 Soars, Marking a New High

On Tuesday, UK’s stock market witnessed a significant rebound. The FTSE 100 index, a key indicator, increased by 0.4%, reaching 7,570 points. This jump more than made up for the small loss experienced the day before, marking a near two-month high. The rise was largely driven by a recovery in stocks related to commodities. This shift in the market occurred as investors digested the latest UK labor report.

Interestingly, the unemployment rate has remained steady at 4.2% for five consecutive months. However, there’s a twist in the tale of wage growth. While still strong, it has seen its most considerable slowdown in almost two years. This development has led money markets to anticipate the Bank of England’s (BoE) first rate cut in June. However, there’s a general agreement that the BoE will likely follow the Federal Reserve’s lead in terms of timing.

On the corporate front, companies like Rio Tinto, Anglo American, and Antofagasta played a significant role. They each saw gains of over 1.5%, bouncing back from the previous day’s downturn. This recovery was supported by a resurgence in the prices of base and ferrous metals, following China’s recent sharp decline in inflation.

However, not all news was positive. Hargreaves Landsdown, a notable firm, experienced a sharp 8% decline in stock value. This drop came after the Financial Conduct Authority (FCA) raised concerns about the firm’s practice of paying interest on cash balances to customers.