Nikkei 225 and Topix Index Surge on BOJ’s Policy

Solid ECN – On Wednesday, Japan’s Nikkei 225 Index saw a significant rise of 1.37%, closing at 33,676, while the broader Topix Index increased by 0.67% to 2,349. This growth continued from the previous session, spurred by the Bank of Japan’s decision to maintain its ultra-loose monetary policy. The central bank also avoided any hints of potential changes in the coming year. Governor Kazuo Ueda, in his press conference, emphasized a dovish stance, stating the bank’s readiness to implement further easing measures if needed.

Additionally, Japanese stocks were buoyed by positive developments on Wall Street, where optimism grew around the expectation that the US Federal Reserve might begin reducing interest rates next year. This optimism was reflected across almost all sectors in the Japanese market, with notable increases in shares of major companies. Kawasaki Kisen saw a rise of 5.6%, Nippon Yusen surged by 32%, Fast Retailing increased by 3.9%, Shin-Etsu Chemical went up by 4.1%, and Nippon Steel grew by 1.6%.

FTSE 100 Hits 7-Month High on Low Inflation

Solid ECN – On Tuesday, the FTSE 100 experienced a notable increase, rising over 1.5% and reaching a seven-month peak near the 7750 mark. This jump came after the release of inflation data that was lower than expected. The data led to widespread conjecture that the Bank of England might start reducing interest rates as early as March 2023, possibly cutting them by a total of 143 basis points.

The sectors most responsive to interest rate changes were the biggest gainers. Homebuilders saw a 3.6% increase, real estate climbed by 1.4%, and real estate investment trusts (REITs) went up by 1.6%. Additionally, there were significant gains in other areas, with energy stocks growing by 2.5% and banks by 2.1%.

Canadian Dollar Peaks Amid Inflation Concerns

Solid ECN – In December, the Canadian dollar reached its highest level since early August, surpassing 1.335 against the USD. This strengthening is a result of persistent inflation within the Canadian economy, which has reignited expectations for a more aggressive monetary policy from the Bank of Canada. Contrary to market anticipations of a slowdown to 2.9%, headline inflation remained steady at 3.1% in November. Moreover, the trimmed-mean core rate, a key measure of inflation, exceeded forecasts by reaching 3.5%.

These figures support the central bank’s earlier predictions that inflation in Canada is likely to stay high for some time. This situation calls for an extended period of tight monetary policy, possibly including additional interest rate increases. In contrast, the Federal Reserve in the United States has signaled a more cautious approach, with policymakers indicating expected rate cuts totaling 75 basis points for the next year. This difference in policy stances has further amplified the Canadian dollar’s rise in value compared to the US dollar.

Fed’s Rate Cut Speculation Keeps Gold Near $2,040

On Wednesday, gold’s price remained steady at about $2,040 per ounce. This stability is close to the highest it’s been in more than two weeks. Despite comments from US Federal Reserve officials, expectations for interest rate reductions next year haven’t changed much. Atlanta Fed President Raphael Bostic, echoing other US policymakers, mentioned on Tuesday that there’s no immediate need to lower US interest rates, considering the economy’s current robustness.

However, the market still anticipates a high likelihood, roughly 75%, of an interest rate cut by March. Looking forward, investors are waiting for the Fed’s preferred core PCE price index, set to be released later this week, for more direction. In other news, the Bank of Japan has decided to maintain its very accommodative monetary policy and hasn’t hinted at any changes for the coming year. Similarly, the People’s Bank of China kept its key lending rates steady, resisting the push to relax monetary policy further despite a struggling economic recovery.

ASX 200 Dips Slightly, Reflecting Wall Street Sell-Off

Solid ECN – The S&P/ASX 200 Index experienced a slight drop of 0.45%, ending the day at 7,504 on Thursday. This downturn came after the index reached its highest point in over ten months, mirroring a sudden decline in Wall Street due to profit-taking after a significant surge that took US markets to new highs. Caution prevailed among investors as they awaited important economic reports from the US, including GDP and inflation figures, which might affect the Federal Reserve’s financial strategy.

In Australia, the Reserve Bank’s recent meeting notes revealed a debate over raising interest rates for another month in December. However, the decision was to wait for more information, as there were some positive signs regarding inflation. The drop in the index was mainly due to the downward movement in sectors like mining, finance, and consumer goods. Significant losses were seen in companies like Allkem (down 5.6%), Pilbara Minerals (down 3.4%), Commonwealth Bank (down 0.4%), Macquarie Group (down 0.9%), Aristocrat Leisure (down 2.3%), and Woolworths Group (down 0.4%).

France’s Manufacturing Sector: A Mixed Outlook for 2024

Solid ECN – In December 2023, France’s manufacturing sector showed signs of positive change. The manufacturing climate indicator, a measure of the health of the industry, reached 100, the highest level since July. This increase, up from 99 in November, surpassed expectations of 98. Key factors behind this rise included a more positive view from industrialists about recent production, moving from a negative perception (-9) in the past to a neutral stance (0). Additionally, there was a slight improvement in the inventory of finished goods, with the index moving from 13 to 14.

However, not all aspects were upbeat. The overall order books didn’t show any change, remaining at a low level (-17), though foreign orders saw a marginal improvement. Concerns emerged regarding the future, as manufacturers’ expectations for their own production dropped slightly, and their outlook on selling prices also deteriorated.

An encouraging sign was the decrease in perceived economic uncertainty, which fell to 25 in December from 28 in November. This suggests that manufacturers are becoming slightly more confident about the economic environment.

France Manufacturing Sector: Economic Implication

Looking ahead, these mixed signals in France’s manufacturing sector offer a nuanced view of the economic future. The improvement in the manufacturing climate indicator and the reduction in uncertainty are positive signs, indicating potential growth and stability in the industry. However, the stagnant order books and cautious outlook on production and pricing point to ongoing challenges. The sector might experience moderate growth but will likely continue facing hurdles, such as fluctuating demand and pricing pressures.

Overall, while the immediate future seems cautiously optimistic, the long-term outlook remains uncertain, dependent on both domestic and global economic conditions.

EURUSD Trades Below $1.1

Solid ECN – The EURUSD currency pair is currently trading at less than $1.1. The participants are forecasting a potential dip in the Euro zone interest rates. Francois Villeroy de Galhau from France hinted on Tuesday that a rate cut might be on the horizon next year. The goal would be stabilizing inflation at 2% no later than 2025.

However, Yannis Stournaras of Greece has a more conservative approach, insisting that inflation should be kept under 3% by the middle of the following year before considering a reduction in borrowing costs. Despite inflation falling to 2.4% in November, economic analysts are predicting a possible surge in the latter part of the year.

Offshore Yuan Slips to 7.15

Solid ECN – The offshore yuan dropped to around 7.15 per dollar, moving down from its six-month high. This happened because China’s central bank did not change its main lending rates, even though there was pressure to loosen monetary policy due to a weak economic recovery.

The People’s Bank of China kept its one-year rate at 3.45% and its five-year rate at 4.2%, as many had expected. Now, markets are looking forward to possible rate cuts next year and maybe a lower reserve requirement ratio to keep enough money in circulation. Experts believe that China’s low inflation and slow economic growth justify this expectation. However, the yuan is still strong because the US Federal Reserve might start to cut interest rates next year. Also, the Bank of Japan has not said anything about changing its policies in 2024.

Gold Nears $2,040 Amid Rate Cut Hopes

Solid ECN – Gold climbed to near $2,040 per ounce on Thursday. It recovered from earlier losses, driven by strong beliefs that the US Federal Reserve will reduce interest rates next year. Also, a big drop in stocks created a demand for safe investments like gold.

Even though Federal Reserve officials opposed the idea of many rate cuts next year, the market still thinks there’s a 70% chance of a rate cut in March. Investors are now waiting for US economic growth data on Thursday and the core personal consumption expenditures (PCE) index on Friday for more clues. In the UK, inflation in November fell to its lowest in over two years, suggesting a possible worldwide trend of rate cuts. In other news, the Bank of Japan kept its very relaxed monetary policy, and the People’s Bank of China did not change its main lending rates.

Ibovespa Hits Record High

Solid ECN – On Thursday, the Ibovespa index climbed 0.8%. It reached over 131,800, a new high. This rise followed a loss in the previous session. The upbeat mood in Wall Street influenced this. Investors think the Federal Reserve will soon lower interest rates. This hope caused a drop in future interest rate expectations in Brazil. It also supports a positive view of Brazil’s central bank. This mood is good for stocks in emerging markets.

Vale, a big company, saw its shares rise almost 3%. This was due to higher iron ore prices. In other news, Braskem, despite a police probe into its mining in Maceio, saw its shares go up.

Yen Holds Firm as Japan Sees Inflation Ease

Solid ECN – In a recent update, the value of the Japanese yen remained stable at approximately 142.2 against the US dollar. This steadiness occurred despite new data indicating a decrease in Japan’s inflation rates. November saw both the main and core inflation rates drop to the lowest they’ve been in 16 months, recording figures of 2.8% and 2.5%, respectively. Notably, the core inflation rate has been over the Bank of Japan’s target of 2% for twenty consecutive months.

Earlier in the week, the yen faced some downward pressure. This was largely due to the Bank of Japan’s decision to continue its very accommodative monetary policy. The bank did not hint at any potential shifts towards more standard policies in the upcoming year. The Bank’s Governor, Kazuo Ueda, emphasized in a press conference that the bank is prepared to implement further easing measures if they become necessary.

In contrast, recent economic data from the United States has led to speculation that the Federal Reserve might begin to reduce interest rates next year. This expectation has lent some support to the yen.

Economic Implication

From an analytical perspective, the economic future appears to hinge on several factors. Japan’s persistent core inflation above the target suggests an underlying economic resilience, possibly influencing the Bank of Japan’s monetary policy decisions in the future. However, the bank’s readiness to introduce further easing measures could signal a cautious approach towards economic uncertainties. Internationally, the US Federal Reserve’s potential interest rate adjustments could impact the yen, either stabilizing or fluctuating its value against the dollar.

Overall, careful monitoring of these domestic and international economic indicators will be crucial in forecasting the yen’s trajectory and Japan’s economic health.

UK Pound Rises Amid Economic Shifts

Solid ECN – The UK pound recently surged past $1.27, driven by investor reactions to fresh economic data and predictions about future monetary policies. Recent reports have painted a mixed picture of the UK’s economic health. The third quarter showed a shrinkage in the economy, a downturn further emphasized by revised figures from the second quarter, signaling a looming recession risk. On a brighter note, retail sales in November surpassed expectations.

Inflation trends are also shifting. The latest Consumer Price Index (CPI) report indicates a drop in UK inflation to 3.8%, significantly lower than the anticipated 4.4%. Additionally, core inflation has fallen to 5.1%, which is below the forecasted 5.6%. These changes have led traders to strongly anticipate interest rate cuts by the Bank of England (BOE) in the coming year. Market expectations suggest a total decrease of 143 basis points, translating to five quarter-point reductions and a 70% likelihood of a sixth cut. However, this contrasts with BOE Governor Andrew Bailey’s insistence on keeping rates higher for a longer duration.

Despite the recent slowdown, inflation in the UK remains nearly double the BOE’s 2% target and is the highest among the Group of Seven nations. This situation poses a delicate balance for policymakers, who must navigate between supporting growth and controlling inflation.

Economic Implication

In a fundamental analysis, the future of the UK economy hinges on several factors. The anticipated interest rate cuts could stimulate spending and investments, potentially aiding in recession recovery. However, persistent high inflation remains a challenge. If inflation continues to outpace targets, the BOE may need to reconsider its stance on rate cuts to prevent further devaluation of the pound and manage cost-of-living increases. The economic outlook will largely depend on the BOE’s ability to balance these competing priorities and the government’s measures to support economic growth.

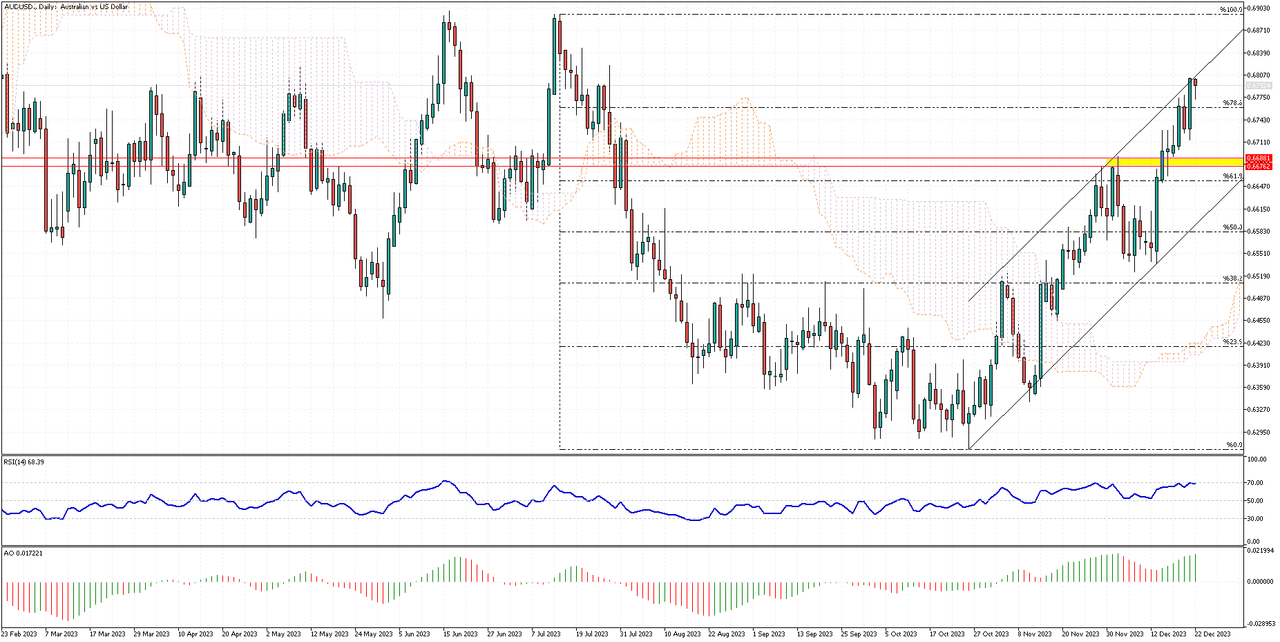

AUDUSD: Buy or Wait?

The AUDUSD’s rise is still going strong, moving near the top of its bullish trend. Yet, in today’s market, the pair approached the 78.6% Fibonacci level, with the RSI near 70. This means the pair isn’t overvalued despite the ongoing uptrend.

For those with smaller budgets, buying now may not be the best move. It’s better to wait for a slight price drop. If the price dips below 78.6%, it could fall to the support zone between 0.6681 and 0.6676, a better buy-in point for those bullish on AUDUSD.

However, buying the Australian dollar now isn’t advisable, strong trend or not. The market looks overbought, and AUDUSD is likely to lose some value. A smarter strategy is to wait for a drop before joining the upward trend.

With its upward momentum, the pair might reach its June 2023 high.

USDJPY’s Sharp Decline

The USDJPY pair saw a sharp drop after hitting the Ichimoku cloud. It’s now trading below a resistance level formed by the cloud. A closer look at the USDJPY 4-hour chart shows the price falling within a channel. The pair is currently at the 78.6% Fibonacci support level.

Given the technical indicators, it seems this support might break, continuing the bearish trend.

Japan’s Economic Index: A Fragile Uptick in 2023

Solid ECN – In October 2023, Japan’s main economic forecast tool (the Leading Economic Index), saw a slight increase to 108.9 from an initial 108.7. However, this was still not as high as the previous month’s 109.3, showing that Japan’s economic recovery is still weak.

The country is dealing with rising prices and lots of outside uncertainties. During the third quarter of 2023, Japan’s economy went down by 0.7%, marking its first drop in a year. This downturn was caused by reduced spending by both people and businesses, and trade issues also played a part in lowering the country’s overall economic performance. Additionally, people’s confidence in the economy in October was almost at its lowest in six months.

A Simple Guide to the Nikkei 225’s Recent Rise

Solid ECN – On Monday, the Nikkei 225 index rose by 85.05 points or 0.26%, ending at 33,254.03. This continued the gains from the previous session. Investors were encouraged by Wall Street’s year-end rally on Friday, especially after the US Federal Reserve’s preferred inflation measure for November was lower than expected and closer to the central bank’s 2% target.

Meanwhile, both overall and core inflation in Japan dropped to a 16-month low last month. On a quiet Christmas day, investors paid attention to a speech by Kazuo Ueda, the governor of the Bank of Japan. He suggested that the central bank might change its monetary policy if wages and prices start moving in the right direction. He also repeated that the board was keeping its very supportive monetary policy to protect the delicate economic recovery.

The healthcare sector led the increase, followed by property, tech, and consumer sectors. The top performers of the day included Nexon Co. (5.4%), NTT Data Group (4.5%), Lasertec Co. (2.8%), NH Foods (2.5%), and Takashimaya Co. (2.4%).

Dollar Index: A Holiday Trading Tale

On Tuesday, amidst holiday trading, the dollar index lingered around 101.6. This was near its five-month low, due to signs of slowing US inflation. This has led to predictions that the Federal Reserve will begin to lower interest rates next year. Data from Friday revealed that the core PCE index, the Federal Reserve’s favored inflation measure, dropped to 3.2% in November from 3.4% in October.

This was lower than the projected 3.3%. Furthermore, figures from Thursday showed a weaker than expected US economic growth in Q3 and a minor rise in unemployment benefit claims recently. The dollar was trading near multi-month lows against other major currencies. It is at risk of further depreciation against the yen, as BOJ Governor Kazuo Ueda stated on Monday that the chances of reaching the 2% inflation target were “gradually rising.”

Euro Hits 5-Month High Amid Dollar Weakness

Solid ECN – The euro recently climbed to $1.1, marking its highest point in five months. This rise is largely due to the weakening U.S. dollar. The latest PCE inflation data from the U.S. has fueled expectations that the Federal Reserve might begin lowering interest rates as early as next year, potentially starting in March.

At the same time, market players are predicting that the European Central Bank (ECB) might also reduce borrowing costs next year, potentially in line with the Fed’s actions. However, it’s worth noting that many ECB policymakers are not in favor of this prediction. Over the course of the year, the euro has seen an approximate 3% increase in value.

Aussie Dollar Strong Amid US Data

Solid ECN – The Australian dollar stays near $0.68, its highest in five months. This is due to US data hinting at Federal Reserve rate cuts next year. Analysts think the Reserve Bank of Australia will cut rates later than others. It hasn’t raised rates as much as other banks. Australian inflation is sticking around longer. RBA Governor Michele Bullock said last month that lowering inflation from around 5.5% to below 3% will take time. It’s mostly due to local demand. Markets expect the RBA to cut rates only by late 2024.

Japanese Yen Strengthens Amid Inflation Progress

Solid ECN – The Japanese yen has recently seen an uptick, reaching approximately 142.2 against the dollar. This boost is largely due to comments made by Kazuo Ueda, the Governor of the Bank of Japan, hinting at improvements in inflation. Ueda expressed that Japan’s economy is slowly but surely moving away from a low-inflation state and inching towards the price stability target. However, he also noted that the chances of this happening are not yet high enough.

Ueda further stated that if the positive feedback loop between wages and prices strengthens and the likelihood of sustainably achieving the 2% inflation target increases enough, the board may contemplate altering its monetary policy. Earlier in the month, the BOJ decided to stick with its ultra-accommodative monetary policy and refrained from making any statements about potential adjustments towards policy normalization in the coming year.

In terms of economic data, Japan’s unemployment rate for November remained steady at 2.5%, which was in line with market predictions.