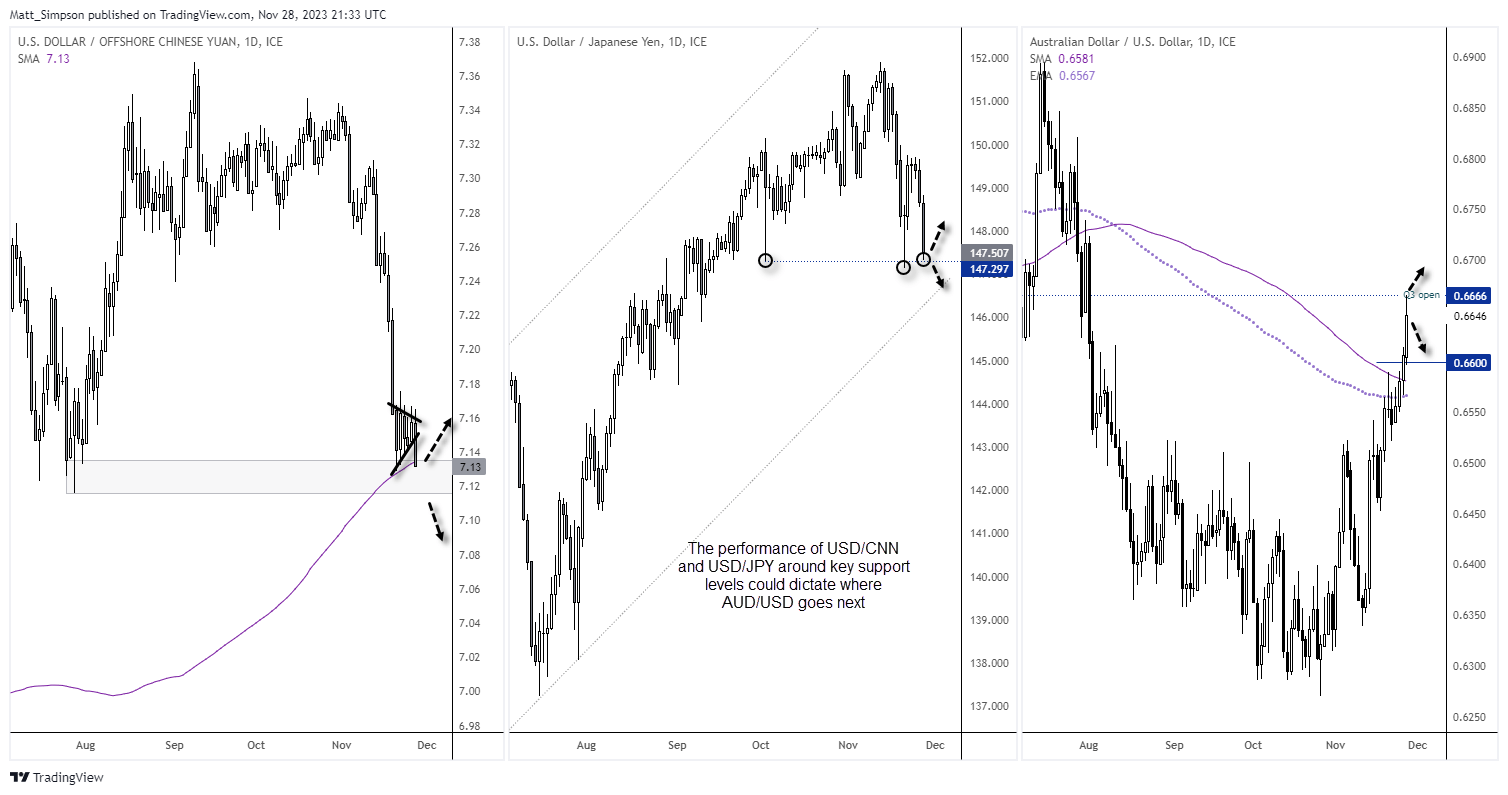

With USD/CNH and USD/JPY probing key support levels, we may require a break of them for AUD/USD to stand a chance of continuing its strong rally (which met strong resistance on Tuesday). Unless of course Australia is treated to a hot inflation report today, which could fan fears of another RBA hike.

By :Matt Simpson, Market Analyst

Market Summary:

- Two of the more hawkish Fed members last year are now on board with holding rates steady, assuming the progress on taming inflation does not stall.

- Inflation is on track to return to the Fed’s 2% target and 4th quarter projections point to a further cooling of CPI according to Christopher Waller and, Whilst Michelle Bowman remains on board with further hikes if need be, she stopped short of backing one in December.

- Bond yields broke lower and the US dollar was again the weakest FX major, heling gold rise to $2040.

- US consumer confidence rose for the first month in four, although “the Expectations Index remains below 80 for a third consecutive month—a level that historically signals a recession within the next year”, according to the Conference Board.

- Whilst most agree that the ECB are most definitely done with hiking rates, ECB’s Nagel said it is premature to talk about cutting them.

- Australian retail sales contracted by -0.2% in October, although it has to be taken with a pinch of salt because consumers likely held off purchases due to the Black Friday sales these figures do not capture (which leaves the potential for a hot print in next month’s report).

- RBA governor Michelle bullock said that the RBA’s policy is “restrictive” and dampening demand, although demand remains strong enough for businesses to maintain profit margins and services inflation was sticker than hoped.

- USD/CNH is probing its 200-day average – a break beneath which could pave the way for another bout of strength for AUD and JPY against the US dollar

- Crude oil snapped a 3-day losing streak and formed a 3-bar bullish reversal around the $75 / 2023 support zone, which adds to my suspicion that oil is preparing for a countertrend bounce. Of course, tomorrow’s OPEC meeting is a risk event that could just as easily make or break that bias.

Events in focus (AEDT):

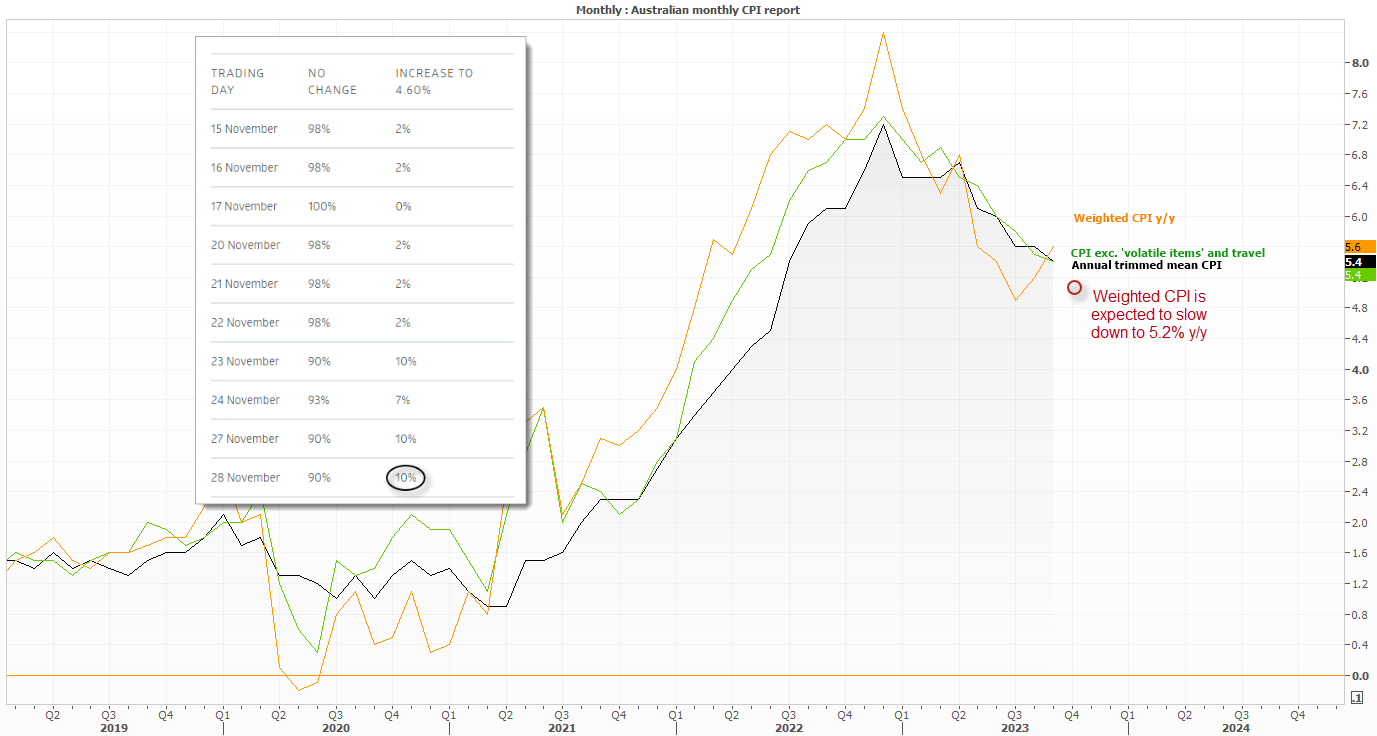

Australian CPI is today’s main event, although it may take a particularly hot set of numbers for the RBA to feel inclined to pull the hiking trigger in December instead of waiting for the more robust quarterly report in late January.

RBA cash rate futures imply just a 10% chance of a 25bp increase to 4.6% on December 5th, and with market-based inflation expectations pulling back nicely then we may find that today’s inflation report points towards a hold until at least February.

The RBNZ also announce their interest decision, although no change is expected and for rates to remain at 5.5%.

- 11:30 – Australian monthly CPI report, construction work done

- 12:00 – RBZ interest rate decision (no change expected)

- 12:30 – BoJ Board Member Adachi Speaks

- 13:00 – RBNZ press conference

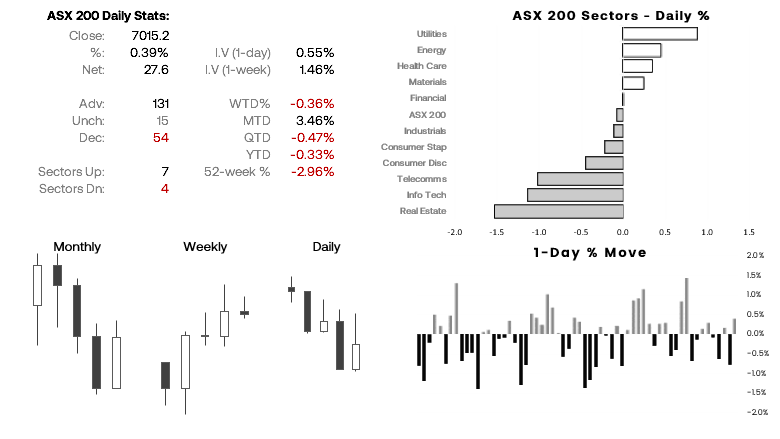

ASX 200 at a glance:

- The ASX 200 was quick to invalidate yesterday’s bearish bias with it mostly erasing the prior day’s losses just after the open

- 65.5% of ASX 200 stock advanced, 27% declined and 7.5% were unchanged

- With SPI futures rising overnight and demand for the ASX below 7,000, the bearish bias has been placed on the back burner until we see a material move lower on Wall Street indices.

USD/CNH, USD/JPY, AUD/USD technical analysis.

Precisely one week ago, we were watching USD/CNH and USD/JPY probe key support levels, where a break likely meant strength for APAC currencies. Whilst AUD/USD continued to rise over the past week, USD/JPY and USD/CNH held their respective support levels. But for AUD/USD to stand any chance of a sustainable break above yesterday’s high, we may need to see the US dollar break lower against the yen and yuan.

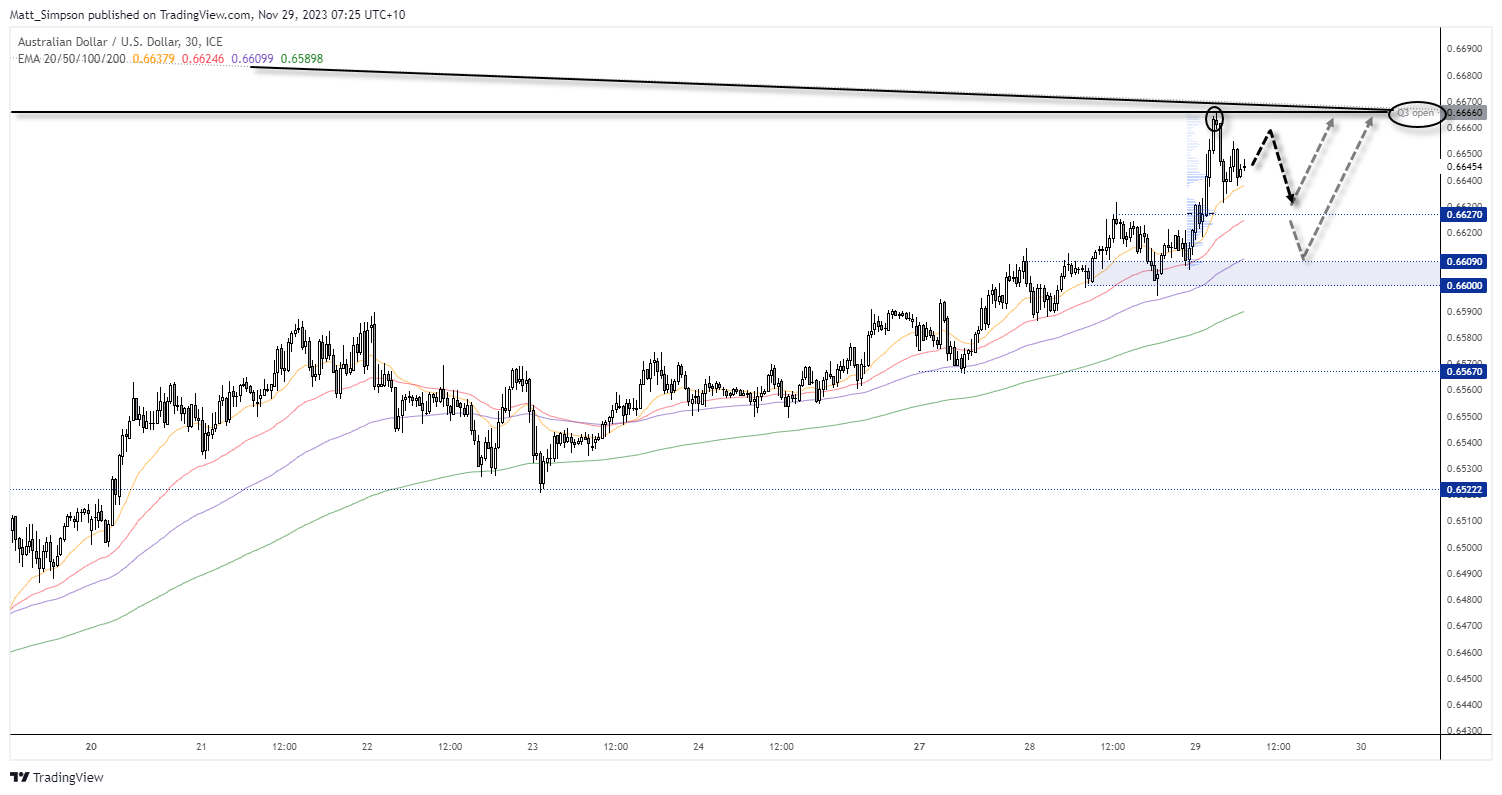

AUD/USD technical analysis (30-minute chart):

The bullish trend on AUD/USD’s 30-minute chart is more than apparent, with prices bouncing along the 10-bar EMA and moving averages fanning out on their bullish sequence. Yet as I mentioned in yesterday’s report, traders may want to seek their setups on a ‘per day’ basis given the strong move already seen. And with CPI data potentially being a non-driver, it may require a bearish breakout on USD/CNH and USD/JPY to expect any bullish breakout on AUD/USD today. Still, that doesn’t mean it won’t try.

What has caught my eye is the momentum shift perfectly at the Q3 open and just beneath a bearish trendline. And if USD/CNH and USD/JPY manage to hold support, bears may want to consider fading into rallies towards yesterday’s high for a countertrend move over the near term.

Alternatively, bulls could wait for suitable evidence a swing low has formed around support levels such as 0.6630 or 0.6600 – 0.6610.

View the full economic calendar

– Written by Matt Simpson

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.