Chinese economic activity is nearing stall speed with the government’s purchasing managers indexes (PMIs) falling further in November, surprising markets to the downside for a second consecutive month.

By :David Scutt, Market Analyst

- China’s PMIs for November missed economist expectations

- The data will undoubtedly intensify chatter about the need for policymakers to deliver more stimulus to the economy

- Market reaction has been muted ahead of US PCE inflation and a speech from Jerome Powell

Chinese economic activity is nearing stall speed with the government’s purchasing managers indexes (PMIs) falling further in November, surprising markets to the downside for a second consecutive month. But as is so often the case when China’s economy is underperforming, the result will only add to speculation that policymakers need to deliver more meaningful stimulus measures.

Manufacturing activity contracted at a faster pace than October, declining to 49.4 from 49.5, below the 49.7 level expected. Non-manufacturing recorded the weakest expansion this year, slowing to 50.2. That was down from 50.6 and a big miss on the 50.9 number forecast by economists.

For those who have not come across PMIs before, a 50 readings signals activity levels were unchanged from a month earlier. Any figure below 50 indicates activity levels declined while a print above 50 suggests activity levels improved. The further away from 50, the greater the breadth of the decline or expansion in activity.

While China’s manufacturing PMI has spent plenty of time below 50 in the past, reflecting the nation’s transition to a more services-based economy, the non-manufacturing PMI has not, falling into contractionary territory for the first time during the coronavirus pandemic. That suggests that outside of extreme events, the 50.2 figure for November is arguably one of the weakest on record.

The November surveys conflict with remarks from Pan Gongshen, Governor of the People’s Bank of China (PBOC), who suggested earlier that there were green shoots emerging in China’s PMIs. These results are more akin to withering rather than green shoots, painting a picture of extreme sluggishness in the Chinese economy as it attempts to move away from construction-led growth that acted to juice economic growth for decades until recently.

The reaction in Chinese and China-aligned markets has been negligible following the data, only acting to reinforce the belief more stimulus measures will be forthcoming. There are arguably more important data events ahead with US core PCE inflation, jobless claims, a speech from Federal Reserve of New York President John Williams and inflation figures from the eurozone released later in the session.

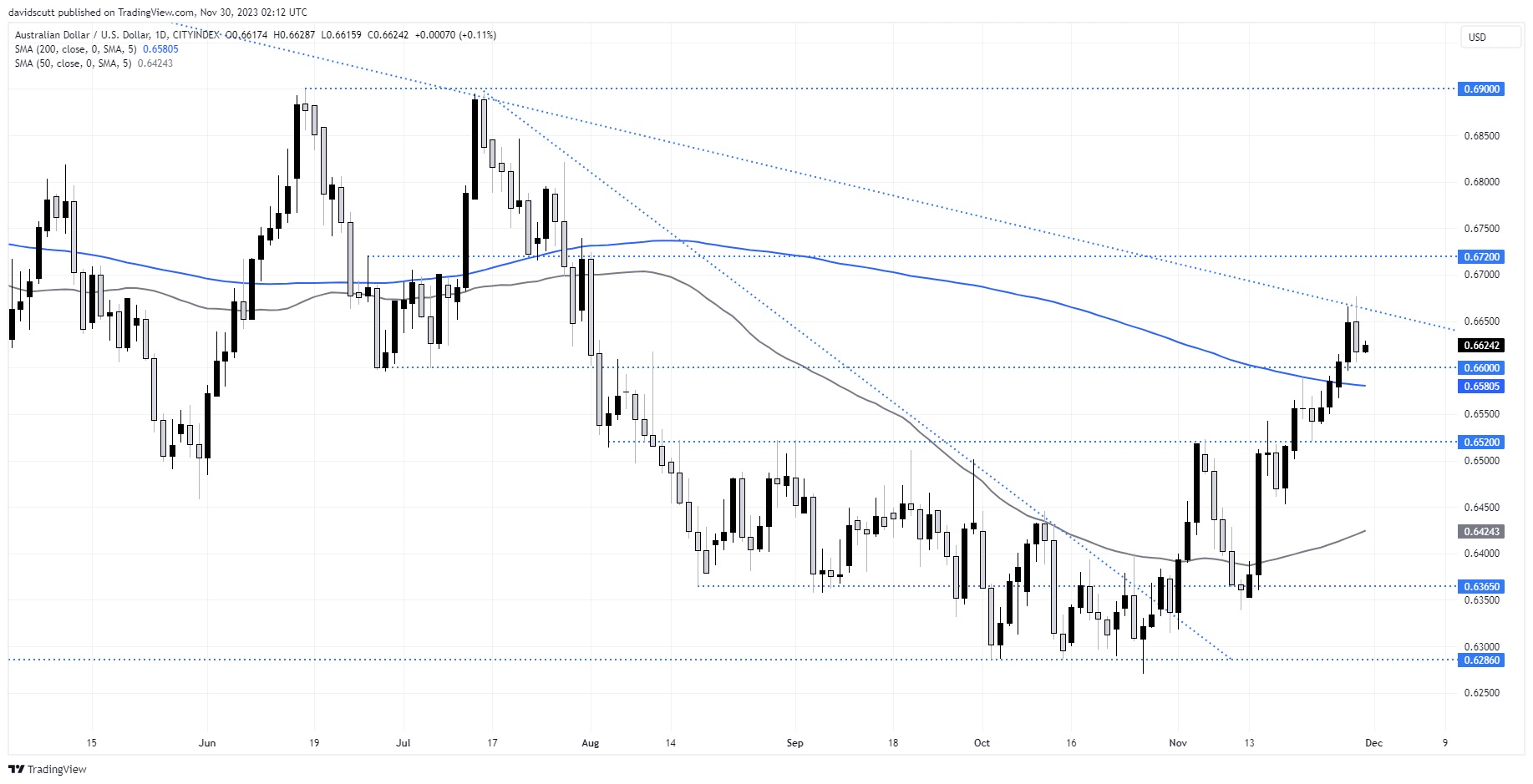

AUD/USD dipped marginally in response to PMI, sandwiched between horizontal support around .6600 and downtrend resistance located near .6660.

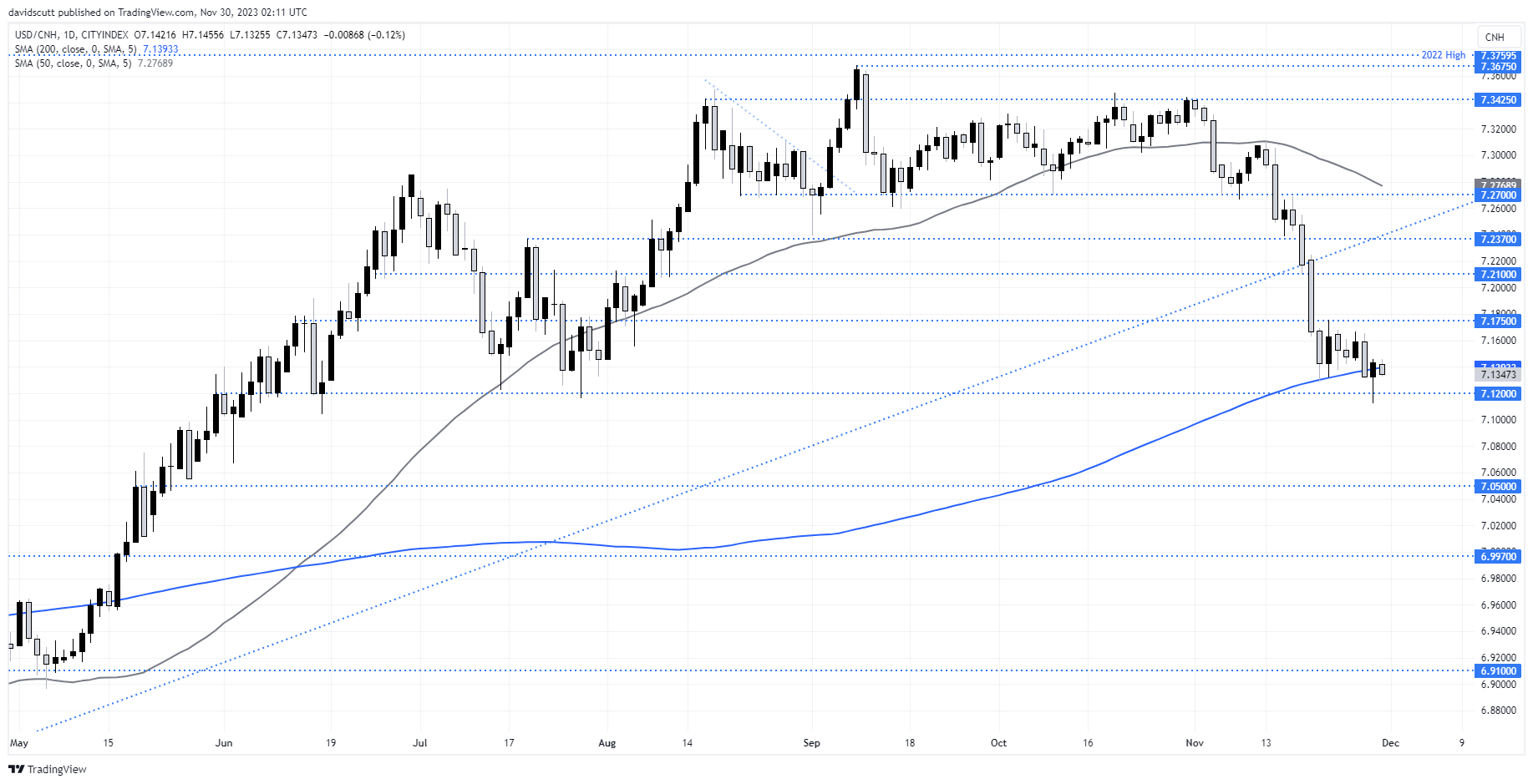

USD/CNH barely flickered in response, with markets more attune to shifts in US bond yields which are continuing to grind lower in Asia, putting Treasuries on track to record the strongest monthly gain dating back to the 1980s, according to Bloomberg’s aggregate index.

USD/CNH attempted to break horizontal resistance on Wednesday having cleared the 200-day moving average, although the dip was quickly bought resulting in a bullish hammer candle. The pair remains wed to the 200DMA for the moment.

– Written by David Scutt

The information on this web site is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement. The information and opinions in this report are for general information use only and are not intended as an offer or solicitation with respect to the purchase or sale of any currency or CFD contract. All opinions and information contained in this report are subject to change without notice. This report has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. Any references to historical price movements or levels is informational based on our analysis and we do not represent or warranty that any such movements or levels are likely to reoccur in the future. While the information contained herein was obtained from sources believed to be reliable, author does not guarantee its accuracy or completeness, nor does author assume any liability for any direct, indirect or consequential loss that may result from the reliance by any person upon any such information or opinions.

Futures, Options on Futures, Foreign Exchange and other leveraged products involves significant risk of loss and is not suitable for all investors. Losses can exceed your deposits. Increasing leverage increases risk. Spot Gold and Silver contracts are not subject to regulation under the U.S. Commodity Exchange Act. Contracts for Difference (CFDs) are not available for US residents. Before deciding to trade forex, commodity futures, or digital assets, you should carefully consider your financial objectives, level of experience and risk appetite. Any opinions, news, research, analyses, prices or other information contained herein is intended as general information about the subject matter covered and is provided with the understanding that we do not provide any investment, legal, or tax advice. You should consult with appropriate counsel or other advisors on all investment, legal, or tax matters. References to FOREX.com or GAIN Capital refer to StoneX Group Inc. and its subsidiaries. Please read Characteristics and Risks of Standardized Options.