Thanksgiving in the US has made for a very quiet second half to the week for traders, but with a key US inflation report and an OPEC meeting on tap then volatility is expected to return next week. Also note that Australia releases inflation figures which could be the deciding factor as to whether the RBA hold or hike at their final meeting of the year.

By :Matt Simpson, Market Analyst

Crude oil steadies ahead of OPEC, US inflation in focus: The Week Ahead

Thanksgiving in the US has made for a very quiet second half to the week for traders, but with a key US inflation report and an OPEC meeting on tap then volatility is expected to return next week. Also note that Australia releases inflation figures which could be the deciding factor as to whether the RBA hold or hike at their final meeting of the year.

The week that was:

- It was a shortened week due to Thanksgiving on Thursday, which saw much of the action in the first half

- Bond investors finally decided the high yields were worth a punt, so stepped in to support falling US bond prices to send yields lower and Wall Street higher

- Canada’s inflation continued to fall below consensus estimates, which likely keeps the BOC on pause mode

- The RBA’s minutes were and preceding comments from RBA members remained on the hawkish side, where they raised the concerns of inflation taking longer to fall back to target and maintaining a tightening bias

- OPEC+ delayed their meeting by three days as reports suggests members could not agree on output levels. OPEC+ are now due to meet on November 30.

- The FOMC minutes were overshadowed by last week’s soft CPI and PPI figures (alongside rising jobless claims data) which effectively poured cold water on recent hawkish Fed comments

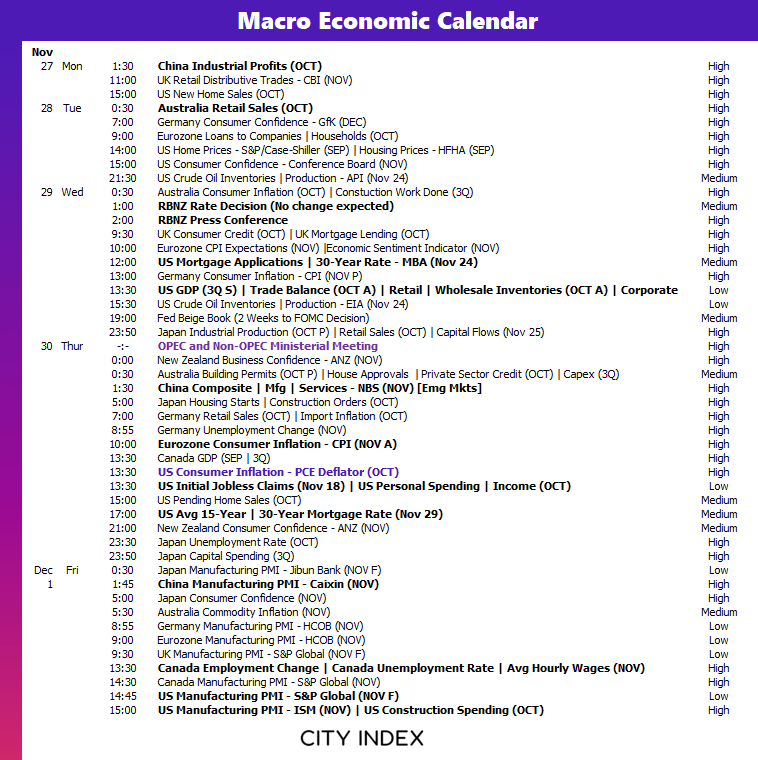

The week ahead (calendar):

This content will only appear on City Index websites!

This content will only appear on City Index websites!

Earnings This Week

Look at the corporate calendar and find out what stocks will be reporting results in Earnings This Week.

The week ahead (key events and themes):

- US PCE inflation

- US bond auctions

- OPEC+ meeting

- Australia’s monthly inflation report

- Flash PMIs

- RBNZ rate decision

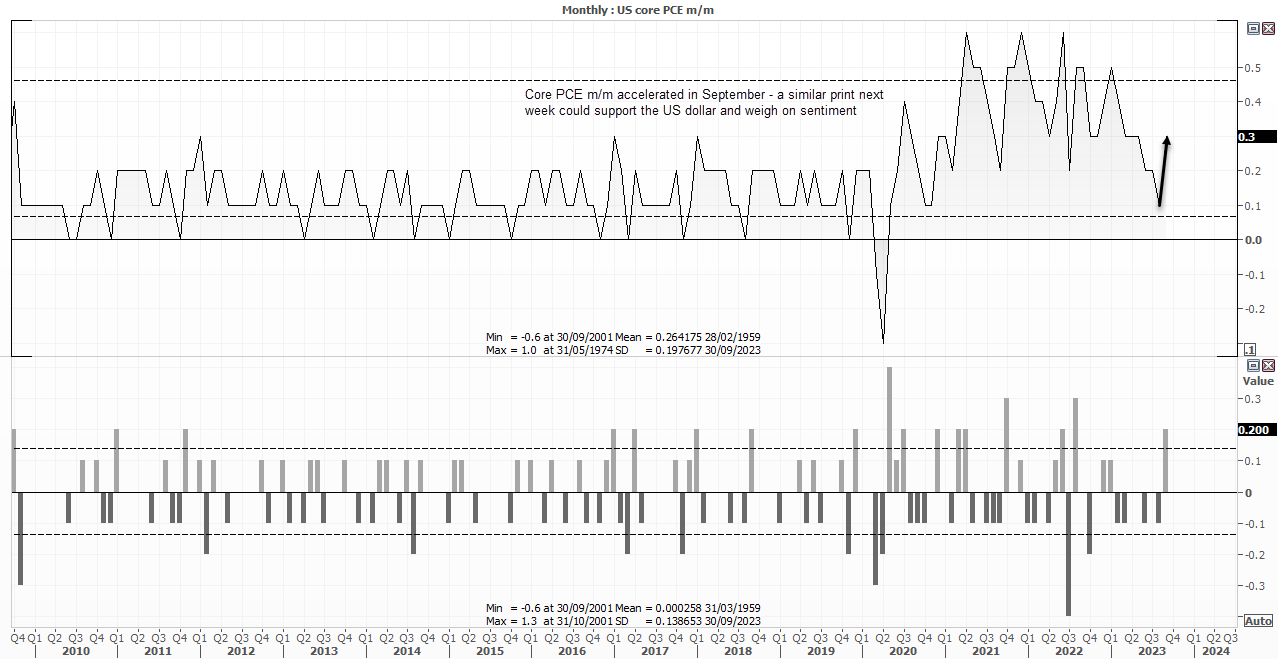

US PCE inflation

Inflation data and its importance needs no introduction. But with headline CPI prints for the US coming in below expectations and taking the wind out of the Fed’s hawkish rhetoric leading up to the report, traders will want to see a similar pattern emerge with PCE inflation figures next week to retain their view that the Fed may cut rates next year. Core PCE is generally the Fed’s preferred inflation measure, although it is less volatile than the traditional CPI measures.

September’s figures showed that core PCE rose 0.3% m/m, which is above its long-term average of 0.26% and the monthly rate of change of +0.2 was above 1 standard deviation. If we see another similar print next week, it could weigh on risk appetite and support the US dollar as traders cancel their expectations of a 2024 rate cut and reconsider the potential for a hike. Yet if we’re treated to 0.2% or lower, it plays back into the ‘peak Fed, 2024 cut’ narrative that markets are currently pricing in which could weigh on the US dollar and support risk assets.

Trader’s watchlist: EURUSD, USD/JPY, WTI Crude Oil, Gold, S&P 500, Nasdaq 100, Dow Jones

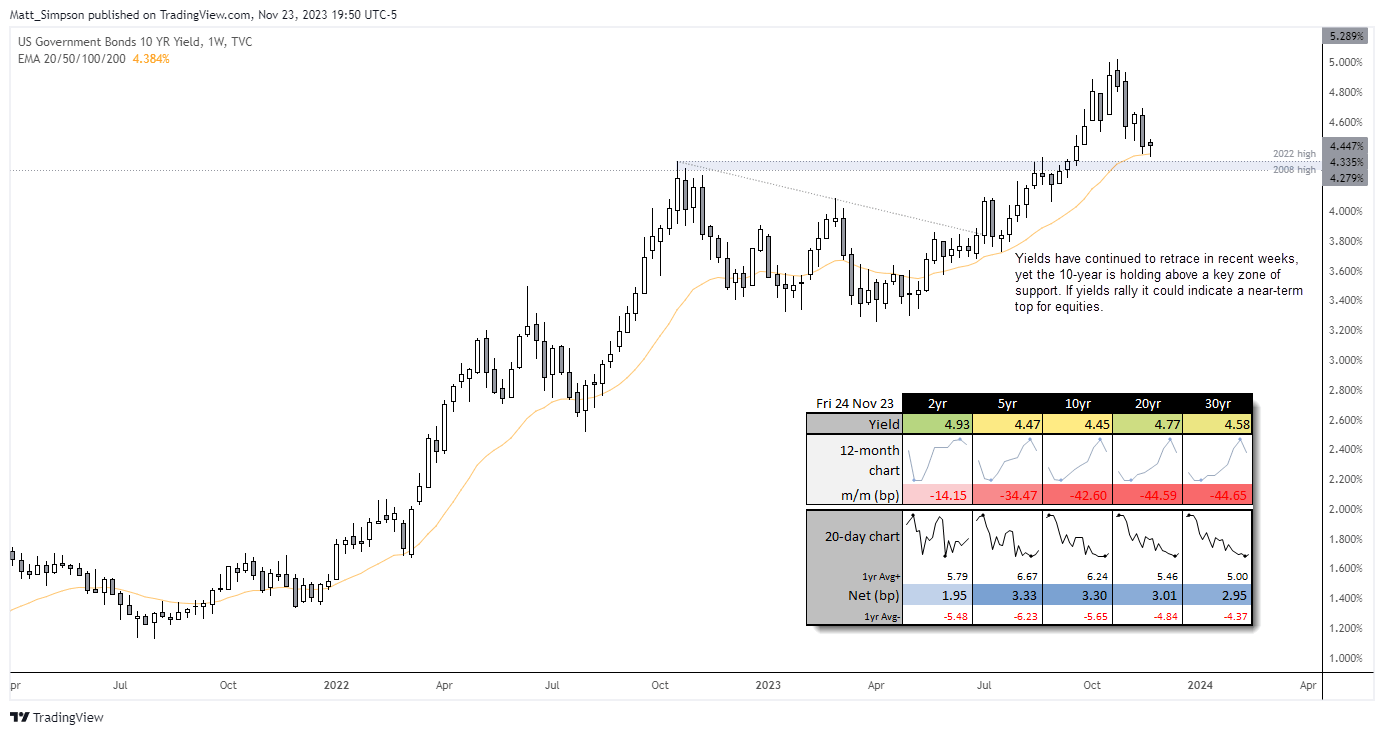

US bond auctions

It seems that investors finally decided that yields were attractive enough to coax bond investors from the shadows and buy the product this week. In turn, this provided another boost to the US equity market and risk assets in general. The question next week is if we see this turn into a trend or make it look like a mere blip admit an established bond bear market. Should the floor of support for bonds disappear, that will send yields higher and spook investor confidence for another bout of risk off.

Trader’s watchlist: USD/JPY, WTI Crude Oil, Gold, S&P 500, Nasdaq 100, Dow Jones

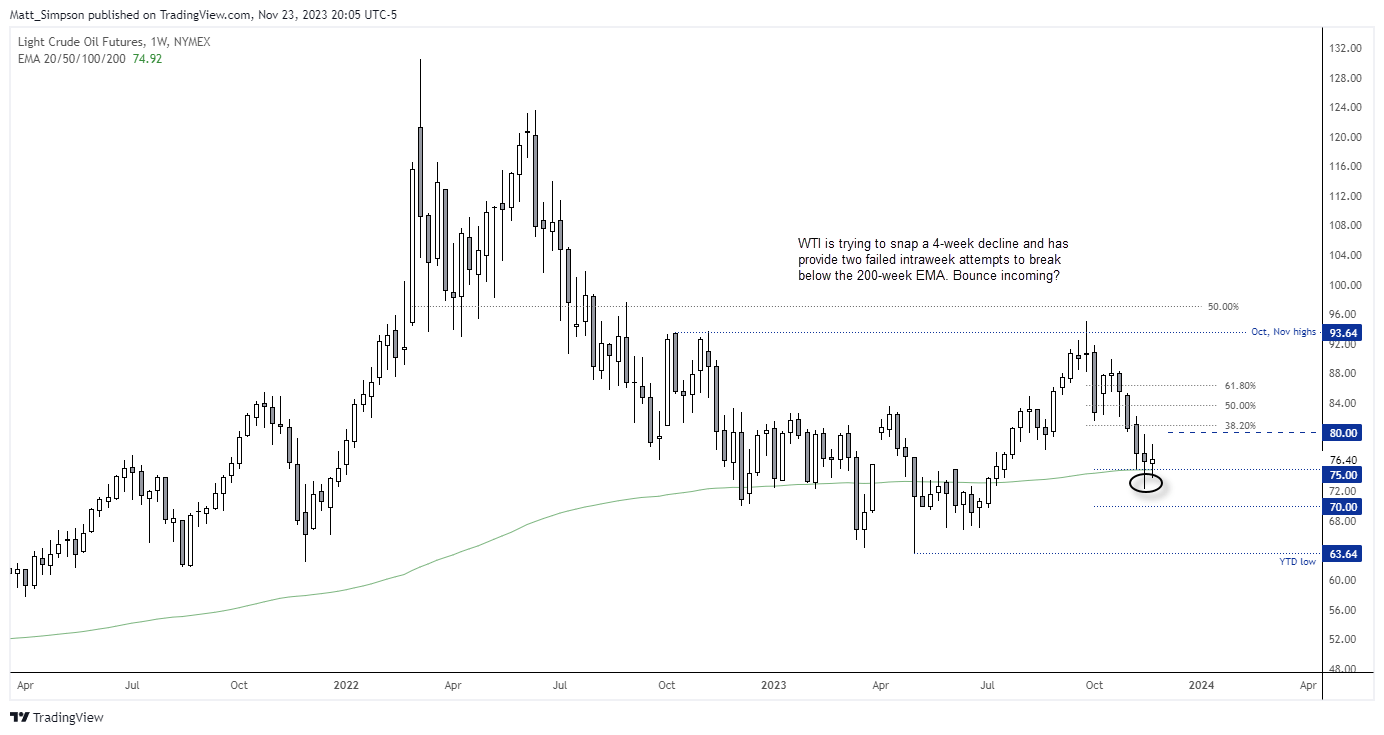

OPEC+ meeting

Disagreement among OPEC+ members over how much to cut oil production by saw OPEC announce that Monday’s meeting will be postponed until November 30. There had been rumours that OPEC were set to announce production cuts at their next meeting, which didn’t come as a huge surprise given oil prices had fallen by around -25% since late September. As things stand, OPEC produce 3.66 million barrels per day following their last round of cuts, which was scheduled to last until the end of 2024. But we’d likely need to see some serious cuts for oil to sustain a rally, and that leaves room for disappointment (and lower oil prices after the announcement). Still, it leaves the potential for a ‘buy the rumour, sell the fact’ rally next week from arguably oversold levels.

The weekly chart is interesting as it is currently on track to snap a 4-week decline with a small bullish doji. But the fact it has fallen by ~25% and is now resting above the 200-week EMA suggests to me that we could also be due a bounce on the weekly timeframe. If it can hold on to any gains and how far it can bounce is likely down to how aggressive OPEC’s cuts are next week.

Trader’s watchlist: WTI crude oil, brent

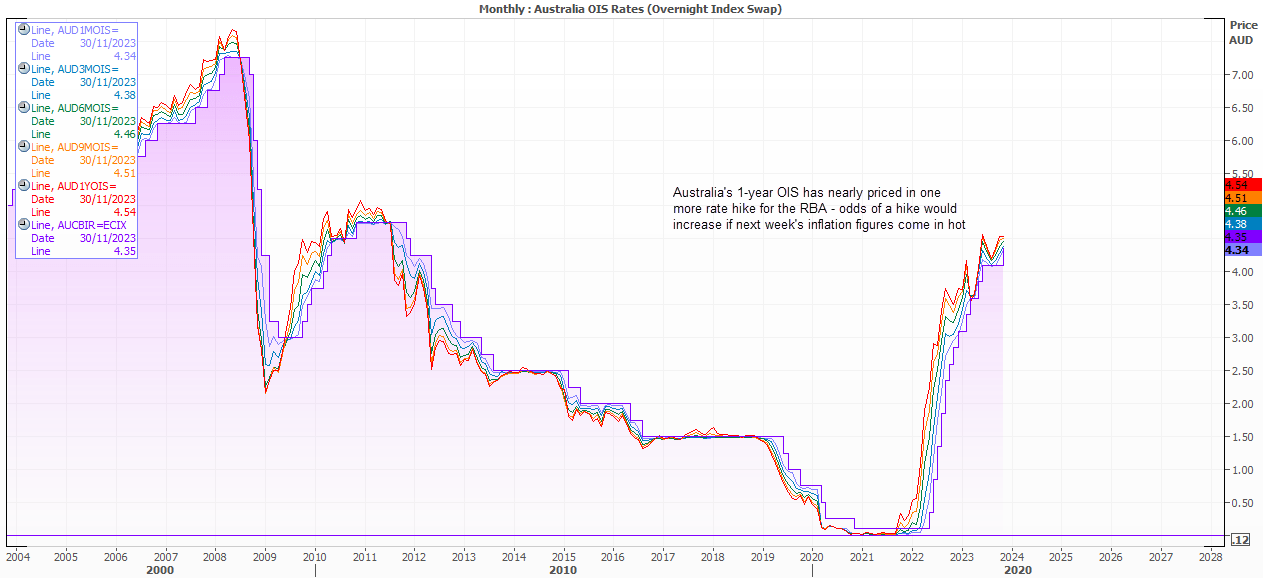

Australia’s monthly inflation report

We’ve seen some consistently hawkish commentary coming from RBA members over the last couple of weeks, and this has been backed up by hawkish RBA minutes. A speech by Governor Bullock on Wednesday made it clear that inflation expectations remain a key metric for the RBA, and her words were hawkish enough to see the 10-year breakeven rates pull back materially. On one hand this is good for those not wanting higher rates, because the RBA may be less inclined to hike if market pricing doesn’t expect higher levels of inflation in the future. But that only goes so far, because if realised inflation continues to beat expectation then it forces the RBA to act, otherwise inflation expectations will rise once again. And as the recent quarterly inflation report forced the RBA to act, a hot set of CPI figures form next week’s monthly report increase the odds of an RBA hike at their December meeting. Unless the RBA opt to gift consumers a merry Christmas with another hold and hope the quarterly CPI figures at the end of January behave.

Trader’s watchlist: AUD/USD, NZD/USD, AUD/NZD, NZD/JPY, AUD/JPY, ASX 200

– Written by Matt Simpson

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.