HSBC have bought the UK arm of SVB - all monies safe, business as usual this morning.

Now to the US

HSBC have bought the UK arm of SVB - all monies safe, business as usual this morning.

Now to the US

Current affairs effect this morning is negative stocks positive bonds - risk off.

Reason is Credit Suisse - long story short is the headline “Credit Suisse Saudi baclers say no more money”.

What was actually said by Saudi National Bank’s chairman was

“I don’t think they will need extra money; if you look at their ratios, they’re fine. And they operate under a strong regulatory regime in Switzerland and in other countries,”

In normal circumstance comments that would have little effect on the market but right now not normal times.

There needs to be more positive proactive approach - a market reacting to fear can lead to bad consequences.

Further to yesterday evenings announcement from the Swiss Nat Bank to the effect that we will back you - Credit Suisse are to receive 50bn from the SNB.

What will they do with that 50bn?

Put it like this - I’d rather not be short that stock right now.

That’s a first step in positive/proactive action by a CB.

Next step is to encourage a takeover by a profitable bank - that has been confirmed this evening - UBS are the new owners - 100bn made available by SNB for liquidity.

Shareholders have little say - new law to by-pass a vote likely already passed, if not then soon.

First offer was rejected by the board, 2nd offer is double and final - passed.

What about the closing price Friday which was SFR 1.85?

Deduct 1.30 - hindsight is a great teacher so wonder is there a lesson for the largest shareholder.

Anyways come tomorrow morning a certain amount of fear will have been lifted - legislature and business working together can be proactive and positive?

OK the fear factor has been lifted somewhat, although still early days.

Tomorrow’s action by the Fed will obviously have a market effect.

It’s worth pointing out the correlation lately between the bond market and USD/JPY - that pair’s movement is being influenced by US bonds - which in turn reflect current risk movement.

2 daily charts - 1st is US10yr - the down arrow is the Dbl Top dated 2/2 - then a very pronounced triple top yesterday.

Then the USD/JPY daily covering the same t/f - today’s action thus far reflecting yesterday’s bond market.

Bottom line is that it’s worth keeping an eye on bond reaction tomorrow.

US bonds continued their price fall since above,

Fed will likely raise .25 today - if they do not then fair chance that the fear factor could return - the question in investors mind would be why no rise?

The changes likely will be in the fwd guidance and with what the Chairman has to say.

It’s an important day not only for the US - we wait.

Stocks 1st spiked up and then have subsequently fallen - USD/JPY likewise reflecting the risk off mood since the FED.

The Bond market had no such volatility - price on the 10yr pretty much indicated where risk lay most of the day - hr1 chart:

The chairman spoke of "Financial conditions that have tightened by more than the traditional indexes say"

It seems that Powell is saying that lending is tighter right now for business and financial indexes “don’t necessarily capture lending conditions”

Maybe he will have more to say in later days but right now he spooked the risk on guys.

Usually the 1st Friday has, or can have, a huge impact on FX - but right now that market is somewhat distracted on rates and inflation - FX is trying to second guess the Fed.

The stock market is a little different - it is looking for positives reflected in the upward daily since Oct 22.

Often the question is asked - is it possible to get an inside on the NFP before Friday - legally that is.

NFP is about business - that’s who do the employing - so if you ask the employers are you confident and they answer yes - then good chance they will employ more.

But who to ask - maybe the sales ppl, or the stock guys.

The thinking is about the future in business - the ppl engaged in that area are the Purchase Managers - they have to figure what’s up ahead and ensure that stock can meet sales demand.

S&P with it’s upward trajectory since Oct '22

Look closely at the above daily and then figure this - released earlier this week.

I hear guys say - ah but the US economy is made up of more than manufacturing - correct, so then look to the composite pmi

(For guys learning PMI is Purchase Managers Index) - regarded as a leading indicator - i.e. looking at the chart to the right)

PMI is classified as a “leading indicator” - meaning that it indicates likely price direction.

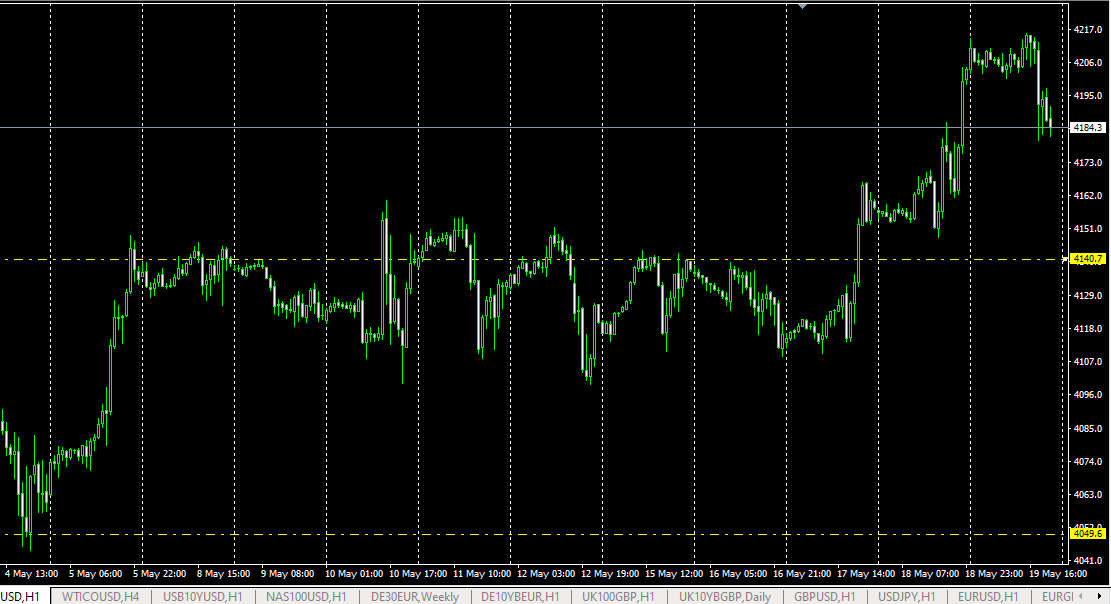

2 weeks ago I highlighted the S&P chart at 4049,it’s trajectory, and then the PMI

Leading means to wait - check 4140.70 since then - guys went short hoping to reach back down to 4049 - price tried - went 50% but gave up and headed North.

The 50% level, though technically not a fib, is an important level to watch.

Price closed this week at 4211.40 - leading means to wait and waiting means to be patient.

What’s likely up ahead?

This is where current affairs effect the market most - when either optimism or pessimism prevail.

Which do you think this incoming week?

I don’t think the current state of affairs will affect the currency market in particular. Other markets maybe, but not currencies.

USD will still be the strongest asset on the block. Although we can expect it to lose some value in the near future. But in the long haul the EU will suffer from higher inflation, while the US authorities managed to achieve some intermediate results.

Edit: most market observers are aware of the US debt ceiling agreement reached between the Dems & Reps over the weekend - general analysis is that this agreement has already been ‘priced in’ last Friday - thus any risk on equally priced in.

This is where patience comes into play.

The edit feature was disabled back 3 weeks - nonetheless an edit remained on my computer as above.

The S&P continued Northward which given the TA and FA is no surprise.

As Kubepaal points out the ‘market’ is not just FX or Stocks - it’s a lot more.

The debt ceiling agreement encouraged risk investors, already buoyed with pmi - yet that did not mean significant buying USD - different current affairs means different effects.

Right now FX is focussed on rates and likely/possible trajectory

Testing the edit feature:

Inflation is right now is a watch word for rates because CB’s are sticking with the old adage that higher rates curtail prices - previously it was who was going higher - right now it’s who has peaked and likely to go lower.

Today is crucial for UK and it’s CB, the BOE

Up to now the blame for UK inflation was laid at the door of Ukraine/Russia / Energy prices - and the BOE have raised rates 13 times in a row to combat rising prices.

The difficulty is that inflations seems stuck - unlike the US and EU where there are signs that prices are not rising as fast.

The driver now appears to be wages - a shortage of labour coupled with higher mortgage rates and further added costs to imports/exports from/to the UK’s largest market post Brexit continues to cause firms to increase their prices.

There is an argument that higher rates are not going to fix the problem on their own, rather a ‘soft’ recession is the only answer.

The risk for the CB is that recessions are as difficult to control as inflation.

Some guys questioned why the higher inflation numbers haven’t impacted positively for GBP - initially it did on a knee jerk but then the market began to think further ahead.

Today’s rise likely .25 - tough times ahead for the BOE

The rise was dbl that - huge shock given current outlook.

FA says that again this shld reflecct a rise in GBP - again that rise occurred initially but appears to have been sold by the market.

Seems the BOE are gambling on a soft recession - Gov of the BOE states “we know this is hard” - which I’m sure will provide great reassurance to mortgage holders and business borrowing.

For guys holding a risk trade over the w/end current affairs in Russia will likely have an effect on prices come Monday morning.

This is the reason that many risk traders close on a Friday especially if there is a hint of geo political turmoil unfolding.

Russel 2000 was the marker.

Edit: for those with risk on there is a semblance of hope - Prigozhin is apparently headed to Belarus with all charges dropped - fighters to sign contracts.

Very early days yet - also very fluid situation.

PMI is useful when thinking about NFP up ahead.- if business confidence is low than good chance that employers will put off hiring.

Pre NFP yesterday - I will quote Tradingeconomics:

“The ISM Manufacturing PMI in the United States fell to 46 in June 2023, from 46.9 in May and below forecasts of 47.”

Bottom line is keep an eye on PMI whether fx or stocks

Fitch have downgraded US from AAA to AA+

May affect USD especially with Yen but good chance reaction is fx will not be huge.

In the FTSE however different story right now - has fallen continuously since the news.

I wldnt sell it though - seems a knee jerk reaction.

Right now the BOE’s Bailey has said that many indicators are signalling a fall in inflation, which will be marked by the end of this year

Negative GBP likely for immed future.

Pound fell against most currencies in the hours after that - words from the CB are always worth watching - Bailey was talking in the HoC, well telegraphed all week.