Powell’s Testimony: Fed Sees No Rush for Rate Cuts, Citing Tariff & Inflation Risks

Federal Reserve Chair Jerome Powell delivered another cautious tone during his testimony before Congress on Tuesday, reiterating that the central bank is in no rush to cut interest rates. Despite increasing market expectations for policy easing, Powell emphasized that the Fed remains firmly committed to a data-dependent approach.

Tariffs and Inflation Concerns Remain, Outlook Uncertain

Powell reiterated that the Fed remains firmly data-dependent and will wait for clearer signs that inflation is sustainably returning to its 2% target before adjusting rates. In particular, Powell warned that recent tariff increases could fuel upward pressure on inflation in the coming months. He noted that while the U.S. labor market remains strong and economic growth resilient, global uncertainties—including trade policy and geopolitical tensions—still pose uncertainty risk to inflationary pressures. Powell also pushed back on calls to cut rates in response to political pressure, stating: “I do not want to point to a particular meeting. I don’t think we need to be in any rush”.

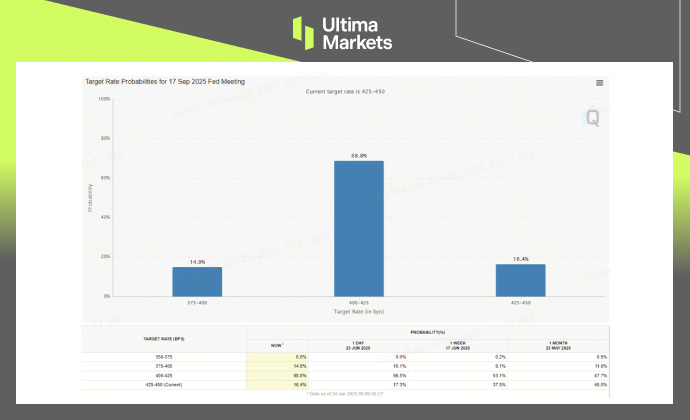

- Fed Target Rate Probabilities for September

Image Source: Source: CME FedWatch

The Fed’s economic outlook signals slower growth and elevated inflation in 2025, reinforcing its cautious approach toward future rate cuts. Shawn, Senior Analyst at Ultima Market, stated: “The Fed’s stance hasn’t changed—it remains firmly data-driven, especially with inflation still clouded by tariff-related uncertainties”. He added, “Markets are likely to increase bets on rate cuts if inflation shows clear signs of cooling in the coming months, particularly ahead of the September meeting”.

Market Reaction: Focus on September Cuts, Dollar Under Pressure

Following Powell’s remarks, markets scaled back expectations for a July rate cut. Fed Funds Futures now show an 81.4% probability of no change in July, increased sharply from earlier weeks. However, expectations for a 25 basis point cut in September rose to 68.8%, up from 53.1% just a week ago, suggesting investors see easing still on the table—but at a slower pace.

The U.S. Dollar further extended downside but broadly held steady, while Treasury yields edged slightly lower as markets digested Powell’s cautious tone.

- USDX—Dollar Index, 4-H Chart Analysis

Image Source: Source: Ultima Market MT5

From a technical perspective, the Dollar Index (USDX) remains in a bearish posture, struggling to reclaim the key 99–100 resistance zone. Without any fresh catalysts to support a rebound—such as stronger economic data or a shift in monetary or Trump policy—the dollar is likely to stay under pressure in the near term.

Markets will be closely watching Friday’s release of the Fed’s preferred inflation gauge—PCE Price Index. A softer-than-expected reading would likely boost expectations for a September rate cut and another cut later this year, reinforcing Powell’s data-centric approach and potentially giving the Fed greater flexibility.

Key Takeaways:

- The Fed maintained a steady rate policy, emphasizing a data-dependent approach moving forward.

- The latest dot plot projects two rate cuts in 2025, but the timing remains unclear due to elevated inflation and weaker growth forecasts.

- Geopolitical risks, tariff-related inflation pressures, and concerns over data quality have become central to the Fed’s policy outlook.

Author:Joshen Stephen|Senior Market Analyst at Ultima Markets

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.