Gold remains above $3,600 per ounce, supported by robust safe-haven demand and higher central bank reserve purchases. Risk-off sentiment continues to draw investors to the metal.

Expectations of a Fed rate cut, trade uncertainties, and renewed geopolitical risks remain key drivers of upward momentum, keeping gold attractive near record highs.

Technically, resistance is at $3,635, with a break above reinforcing the bullish trend. However, overbought RSI signals possible profit-taking. On the downside, strong support is seen at $3,505.

Global markets climbed as weak U.S. jobs data (22,000 new payrolls, unemployment at 4.3%) increased expectations for Fed rate cuts. The 10-year Treasury yield dropped to 4%, its lowest in five months, with traders pricing in at least a 25 bps cut and watching this week’s PPI and CPI.

Gold surged above $3,650 to record highs, supported by lower yields, a softer dollar, and safe-haven demand after U.S. sanction threats on Russia. Oil extended gains, with Brent above $66 and WTI near $62, after OPEC+ confirmed only a modest October output increase of 137,000 bpd.

In Asia, Japan’s Nikkei 225 crossed 44,000 for the first time, driven by stronger GDP and expectations of fiscal and monetary support following Prime Minister Ishiba’s resignation and progress on a U.S.-Japan auto tariff deal.

Markets are watching this week’s CPI report, but the real spotlight is on job market revisions that could redefine the Fed’s path.

Expectations for a 25 bps cut in September are already near 100%, but a 50 bps move depends on signs of cooling inflation.

Revisions from the QCEW survey may show as many as 600,000 fewer jobs, suggesting the labor market is weaker than previously thought.

If core CPI remains hot, the Fed could stay cautious; but a softer print would open the door to bigger cuts.

The balance remains delicate: sticky inflation vs. weakening jobs = stagflation concerns. Traders now price in at least a 25 bps cut baseline, with room for more if data confirms softness.

Global oil markets face new shifts as OPEC+ prepares to raise production once again, signaling a shift in strategy from prioritizing higher prices to maximizing revenue through greater output.

Production Plan

OPEC+ announced that eight key members, including Saudi Arabia, Iraq, and the United Arab Emirates, will increase combined oil production by 137,000 barrels per day starting in October.

Analysts caution that the actual increase may be closer to 60,000 bpd, as many members are already pumping close to capacity.

The move continues the group’s phased rollback of earlier output cuts, with around 2.5 million bpd already added back to the market earlier in 2025.

This latest decision begins unwinding a second set of cuts from April 2023 that initially reduced production by 1.65 million bpd.

Market Impact

Saudi Arabia and other major producers have managed to expand output carefully without causing significant drops in global oil prices. This balancing act reflects their goal of maintaining revenues while stabilizing markets.

Despite the increase, OPEC+ has not set firm production targets beyond October, preferring a flexible, data-driven approach to respond to shifting demand and supply conditions.

Strategic Outlook

OPEC+ leaders remain focused on several objectives:

Regaining market share in a highly competitive energy landscape.

Maintaining price stability while boosting exports.

Responding to global demand trends as economies adapt to shifting trade and tariff environments.

The group’s decision underscores a pragmatic strategy of gradual adjustments, aimed at safeguarding long-term revenue while navigating uncertainties in global energy markets.

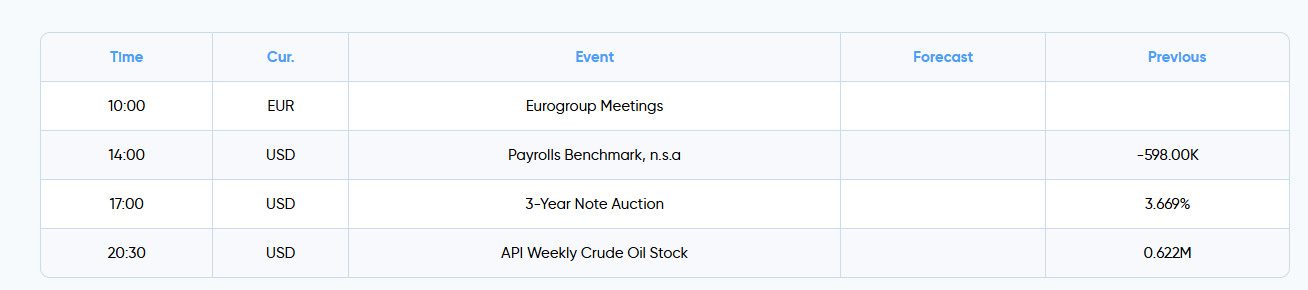

Global Stocks Climb on Fed Cut Bets Despite China Deflation (09.10.2025)

Global markets advanced Tuesday on rising Fed easing expectations. Revised U.S. labor data showed 911,000 fewer jobs through March, reinforcing weak August payrolls and lifting bets on a September rate cut, with some anticipating 50 bps. The 10-year Treasury yield held near 4.08% ahead of inflation reports.

A federal judge blocked President Trump from removing Fed Governor Lisa Cook, easing independence concerns. Meanwhile, Trump urged the EU to impose tariffs up to 100% on China and India over Russian oil, vowing U.S. alignment as talks with Putin yielded little progress on Ukraine.

In Asia, Japan’s Nikkei 225 and South Korea’s KOSPI gained, with chipmakers leading. Singapore and Australia posted modest advances, while India’s Nifty futures rose. Chinese equities lagged after August CPI fell 0.4% and PPI slid 2.9%, marking 35 months of deflation despite state stimulus.

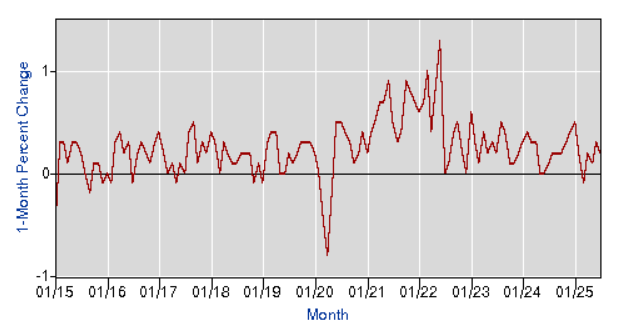

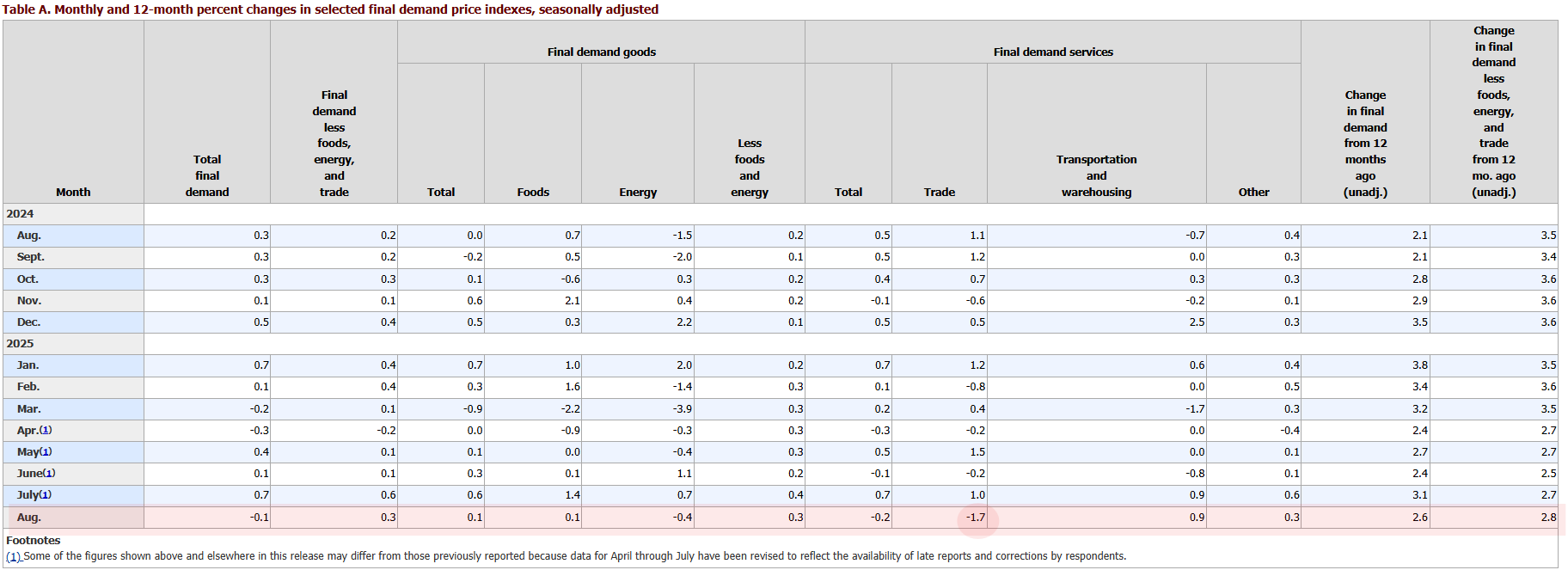

The Producer Price Index (PPI) for final demand declined by 0.1% in August, according to data from the Bureau of Labor Statistics. The dip follows increases of 0.7% in July and 0.1% in June, underlining a turbulent summer for producer-level inflation. On an annual basis, the index rose 2.6%.

The overall fall was driven largely by weaker service prices. Trade service margins dropped by 1.7%, dragging the index lower despite strength in other categories. Transportation and warehousing costs climbed, while portfolio management posted a notable 2.0% increase.

Key drivers in services:

Trade services: –1.7%

Transportation and warehousing: higher

Portfolio management: +2.0%

Goods Prices Edge Higher

Goods prices rose 0.1% in August, with mixed trends across categories. When excluding food and energy, goods prices advanced 0.3%. Energy costs fell 0.4%, while tobacco products surged 2.3%, providing the largest upward push. Natural gas, vegetables, and copper scrap all registered declines.

Core PPI, which strips out food, energy, and trade services, climbed 0.3% in August and 2.8% over the past year. This marks the strongest annual gain since March 2025, reinforcing that inflationary pressures at the producer level remain resilient despite headline volatility.

The latest data from the U.S. Bureau of Labor Statistics shows that wholesale inflation eased in August, raising hopes of a more stable price outlook for the months ahead. The Producer Price Index (PPI) for final demand unexpectedly fell, marking a notable shift after several months of uneven price pressures.

Key Drivers of the Decline

The softer reading was primarily due to weakness in the services sector:

Services: A sharp decline in wholesale and retail trade margins drove the overall drop. While areas such as transportation and portfolio management recorded gains, they were outweighed by broader weakness.

Goods: Prices edged slightly higher, with increases in food and tobacco partially offset by falling energy costs, particularly natural gas.

Implications for Federal Reserve Policy

The decline in wholesale prices is significant for the Federal Reserve. After grappling with persistent inflationary pressures throughout the year, the August reading suggests that price growth may be stabilizing. This could give policymakers more flexibility in shaping interest rate policy, potentially allowing for a cautious approach rather than urgent action.

Despite the softer data, the picture is not entirely clear. Revisions to previous months showed stronger inflationary trends than initially reported, reminding markets that risks remain.

Market and Business Impact

For businesses, the cooling in wholesale costs offers temporary relief, particularly in sectors facing squeezed margins from higher financing and wage expenses. For consumers, the decline may ease some pressure on prices, though much depends on how long the trend lasts.

Overall, the combination of weaker service margins and easing energy costs points to a more favorable inflation path. Still, the Federal Reserve is expected to remain cautious, balancing signs of disinflation against the possibility of renewed volatility.

Wall Street Hits Records, Yields Fall (09.11.2025)

Markets now see a 92% chance of a 25-bps Fed cut on Sept. 19, with some betting on 50 bps amid labor market weakness.

U.S. wholesale inflation slipped 0.1% in August, easing pressure ahead of Thursday’s CPI, expected to show a 0.3% monthly rise and 2.9% annual increase, with core steady at 3.1%.

Equities pushed higher, with the S&P 500 and Nasdaq setting new records on tech strength and Oracle’s earnings. Treasury yields fell to five-month lows, the 10-year at 4.04%, while the dollar index held at 97.8.

The ECB is expected to hold rates steady after 200 bps of cuts since mid-2024, with growth seen at 1.2% this year, though political strains in France and Spain weigh on sentiment.

Oil remained volatile, with Brent near $67.50 and WTI at $64.34, as OPEC+ scaled back supply hikes and geopolitical tensions offset signs of weaker demand.

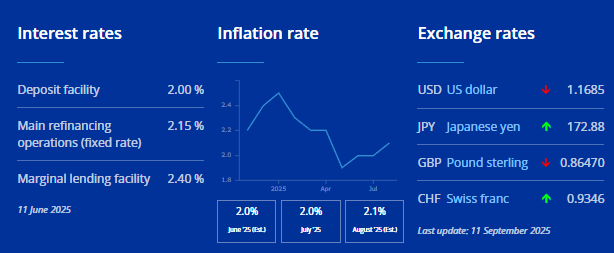

The European Central Bank (ECB) kept its key interest rates unchanged at its latest policy meeting, in line with market expectations. The deposit facility remains at 2.00%, the main refinancing rate at 2.15%, and the marginal lending rate at 2.40%. The decision reflects the ECB’s cautious stance as it continues to assess incoming data before taking further policy steps.

Inflation Outlook

The central bank reaffirmed that inflation in the euro area is close to its 2% medium-term target. Updated staff projections show:

Headline inflation: 2.1% in 2025, easing to 1.7% in 2026, then ticking up to 1.9% in 2027.

Core inflation (excluding food and energy): 2.4% in 2025, 1.9% in 2026, and 1.8% in 2027.

These figures indicate that while inflation pressures are expected to ease somewhat, the ECB remains committed to keeping price growth anchored around its target.

Growth Projections

The euro area economy is forecast to expand by 1.2% in 2025, an upward revision from the previous estimate of 0.9%. Growth is expected to slow to 1.0% in 2026 before recovering to 1.3% in 2027. Policymakers stressed that risks are now more balanced, though they remain watchful of global uncertainty and trade developments.

Lagarde’s Remarks

ECB President Christine Lagarde said the disinflationary phase appears to be over, signaling a shift in the inflation outlook. She emphasized the bank’s commitment to its 2% target and highlighted that decisions will continue to be taken on a meeting-by-meeting basis, guided by incoming data.

Lagarde underlined that the ECB’s approach remains focused on price stability and sustainable growth, assuring markets that the central bank is ready to adjust its stance if conditions change significantly.

Market Implications

The ECB’s steady hand provides short-term clarity for investors, who had anticipated no policy shifts. However, the message of patience and caution suggests that rate moves are unlikely until the bank has a clearer view of both inflation trends and the euro area’s growth path.

Inflation and Labor Data Shape Fed Outlook (09.12.2025)

U.S. stocks hit record highs with the Dow topping 46,000, while futures held flat as traders weighed hotter August CPI at 2.9% and rising jobless claims at 263,000, the highest since 2021. The data strengthened expectations of a September Fed rate cut. Treasury yields stayed near five-month lows around 4.03%.

In Japan, 10-year bond yields hovered near 1.59% as markets assessed the BoJ outlook amid Ishiba’s resignation and new U.S. tariff risks. A joint U.S.-Japan statement reaffirmed market-driven exchange rates.

The ECB kept rates steady, forecasting Eurozone inflation to ease toward 2% by 2027 and growth to slow in 2026 before a modest rebound. President Lagarde emphasized a cautious, data-driven stance.

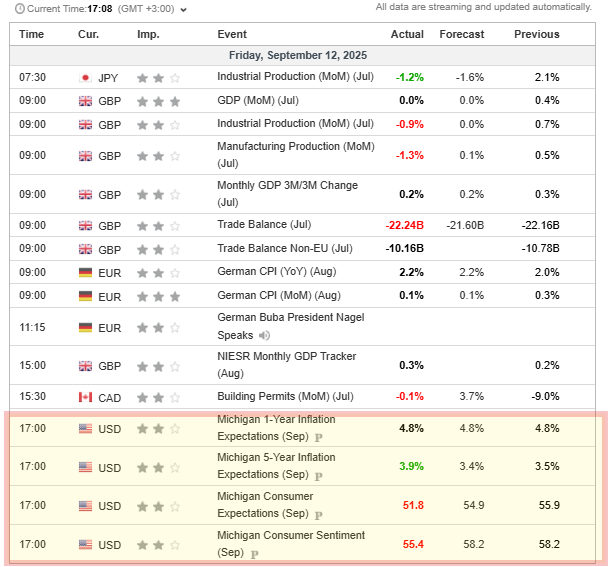

US Consumer Sentiment Dips

The University of Michigan’s Consumer Sentiment Index for September dropped sharply to 55.4, a four-month low, down from 58.2 in August and below the expected 58, according to preliminary data.

Expectations fell notably.

Current conditions eased, with trade policy remaining a major concern for households.

Year-ahead inflation expectations remained steady, while long-term inflation expectations rose for the second consecutive month.

Wow, it’s my first time bumping into your forum, and i love it. Nice breakdown on forex pairs, and economic & geopolitical moments as well. That is the side that i really have to improve.

U.S. stock futures were steady on Monday as markets awaited the Fed’s policy decision. The dollar index held near 97.6, with traders pricing a 96% chance of a 25 bps cut after weak labor and inflation data. Wall Street hit record highs last week, led by AI optimism.

Asian markets opened cautiously. The Bank of Canada and China’s central bank are expected to ease this week, while Japan and the U.K. are seen holding steady. The euro was flat despite France’s Fitch downgrade, while South Korea hit records after dropping a planned stock tax.

Gold held near $3,639, Treasuries stayed low, and the 10-year yield was at 4.06% on Friday. Markets see multiple Fed cuts by year-end, with some betting on a 50 bps move next week.

France’s 10-year government bond yield climbed above 3.5%, its highest since early September, after Fitch Ratings cut the sovereign rating from AA- to A+—the lowest on record. The downgrade reflects political instability, rising debt, and fiscal concerns, as President Macron appoints his fifth PM in two years.

Brent crude futures climbed to $67.25/bbl on Monday, extending Friday’s gains. The move comes as Ukrainian strikes intensify against Russian energy infrastructure, peace talks stall, and fears of fresh Western sanctions increase.

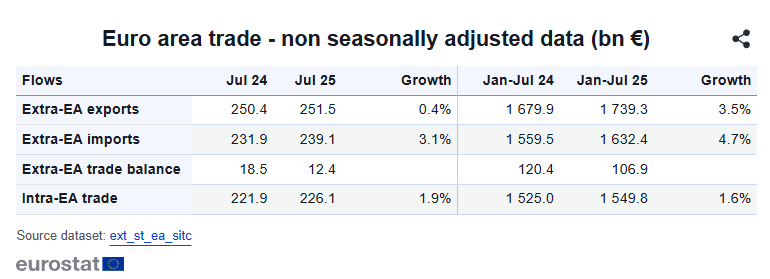

The Euro Area recorded a trade surplus of €12.4 billion in July 2025, down from €18.5 billion a year earlier. The result was slightly better than forecasts of €11.7 billion but still shows pressure from global trade changes. The surplus with the US fell sharply to €11.2 billion from €16.0 billion, reflecting tariff concerns.

Imports rose 3.1% to €239.1 billion, led by food and drink (+9.3%), chemicals (+10.6%), and machinery & vehicles (+2.0%). Purchases from China, the UK, Switzerland, and Turkey also increased.

Exports grew only 0.4% to €251.5 billion. Gains in food and machinery were offset by weaker sales in raw materials (-4.7%), fuels (-18.5%), and chemicals (-6.0%). Shipments to the UK, Switzerland, and Turkey rose, while exports to China dropped (-8.9%).

Overall, the Euro Area kept a surplus, but the gap is narrowing as imports grow faster than exports. Trade tensions with the US and weaker Chinese demand remain key risks ahead.

The September 2025 Federal Open Market Committee (FOMC) meeting arrives under extraordinary circumstances. Political and legal attempts to exclude Fed Governor Lisa Cook from participating stress the distinctive challenges facing the central bank. These developments raise questions not only about the Fed’s independence but also about the integrity of its policymaking process.

Rate Cuts on the Table

Markets expect the Fed to cut interest rates again. Yet the scale of easing is unclear. A 25-basis-point reduction appears most likely, reflecting slowing labor market conditions. However, persistent inflation complicates the picture, leaving a 50bp cut as a possibility that continues to divide policymakers.

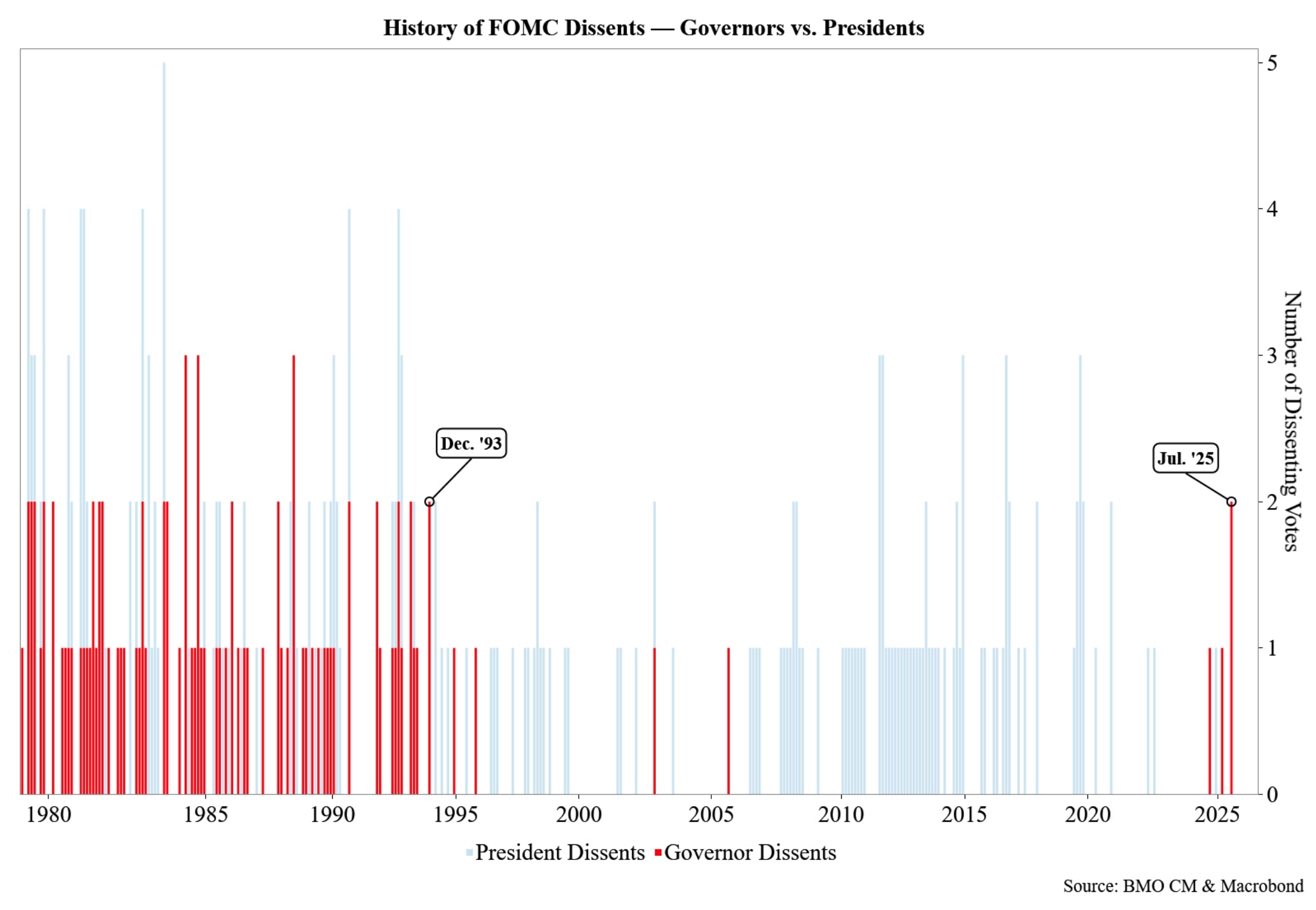

Governor Dissents in Focus

Dissent inside the Fed has become a story of its own. In July, both Christopher Waller and Michelle Bowman voted for deeper cuts than the majority. If they again push for a 50bp move while others settle for 25bp, it would mark the first time in decades that multiple governors dissent in consecutive meetings, a striking signal of fragmentation within the Fed’s leadership.

Key Points to Watch

Division over cut size: 25bp expected vs. 50bp argued by dissenters

Repeat governor dissents: Waller and Bowman could again break ranks

Political backdrop: Legal challenges and pressure surrounding Lisa Cook

Market impact: Investors are weighing the Fed’s credibility as much as its decision

Beyond the policy debate, the Fed’s decision is framed by fragile economic momentum, rising volatility, and contentious political debate. With credibility at stake, the September meeting is not only about the rate cut itself but about whether the Fed can project unity and stability in a moment of deep uncertainty.

Markets Brace for Fed Decision as Stocks Hit Records (09.16.2025)

U.S. futures steadied Tuesday after Wall Street hit fresh highs, with the S&P 500 and Nasdaq setting records. Optimism came from progress in U.S.-China trade talks, while investors focus on Wednesday’s Fed decision, where a 25 bps cut is widely expected.

Tesla rose 3.6% after Musk’s $1B stock purchase, while Nvidia slipped on Chinese antitrust claims. The dollar index held near 97.3, and Trump pushed for deeper cuts.

Silver climbed to $42.65, its highest in over a decade, supported by safe-haven demand, a weaker dollar, and Fed easing bets. Gold hovered around $3,670, capped by dollar strength but supported by Chinese data weakness and geopolitical risks.