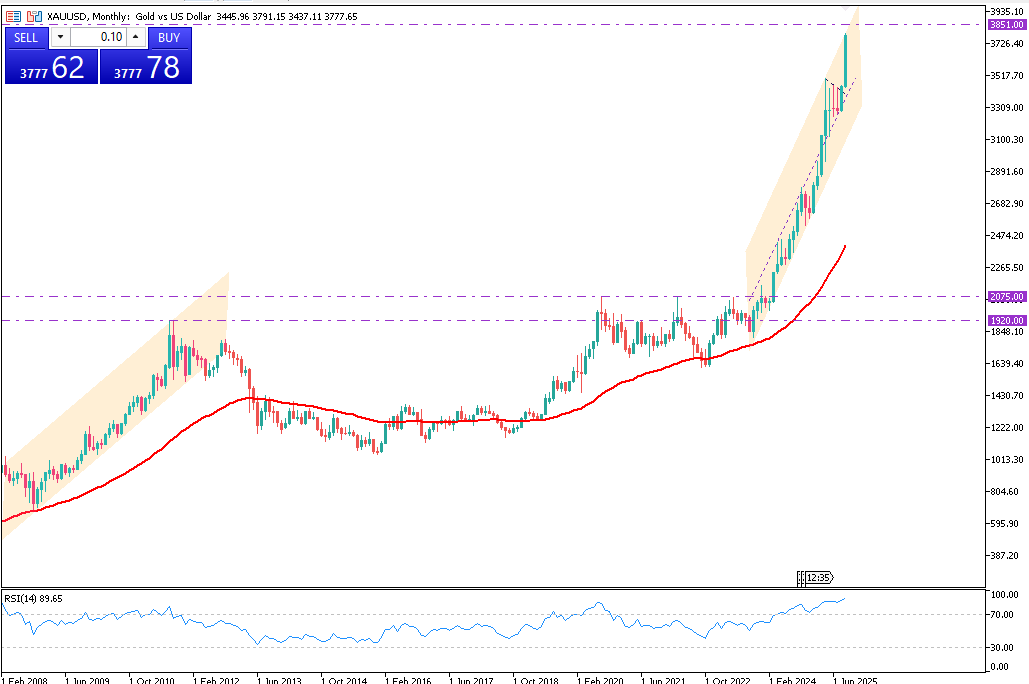

Gold advanced to $3,697 this week, setting a new all-time high. It’s getting closer to the psychological level of $4000. Attention now turns to the Federal Reserve’s policy decision. Markets are pricing in a 25bps rate cut, while signs of labor market weakness suggest the easing cycle may extend into next year, sustaining bullish momentum.

Technical Outlook (XAU/USD):

Near-term target: $3,730

Medium-term target: $4,250 if momentum persists

The sharp rally points to increased volatility. A break above these levels could accelerate further gains, requiring traders to stay alert to swift market moves.

The euro is nearing a four-year high, with $1.20 now in focus and the next target at $1.2255. Central bank meetings dominate the week. The Federal Reserve is expected to cut rates by at least 25 basis points, pressured by a weaker labor market and persistent inflation. The Bank of England and Bank of Japan are likely to hold steady, while the ECB signals its rate-cutting cycle may be ending. President Lagarde noted that growth risks are more balanced.

Technical Targets (EUR/USD):

$1.20 – immediate level

$1.2255 – next resistance

A clear break above these levels could accelerate euro gains and increase volatility in FX markets. Investors should take this into consideration.

Global Markets Steady Ahead of Fed Rate Decision (09.17.2025)

US stock futures were little changed on Wednesday as investors awaited the Federal Reserve’s policy announcement, with a 25 bps rate cut widely expected.

On Tuesday, the Dow, S&P 500, and Nasdaq posted modest losses, weighed down by tech names including Nvidia, Broadcom, and Microsoft. Optimism over US-China trade talks and a new TikTok framework supported sentiment, lifting Oracle shares.

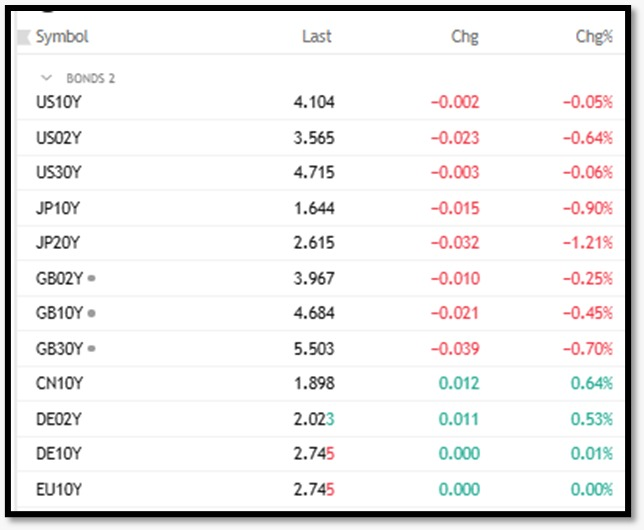

The 10-year Treasury yield hovered near 4.03%, close to five-month lows, as markets priced in a cut and about 67 bps of easing for the year. The dollar index held near 96.7, at a two and a half month low, as the euro hit a four-year high.

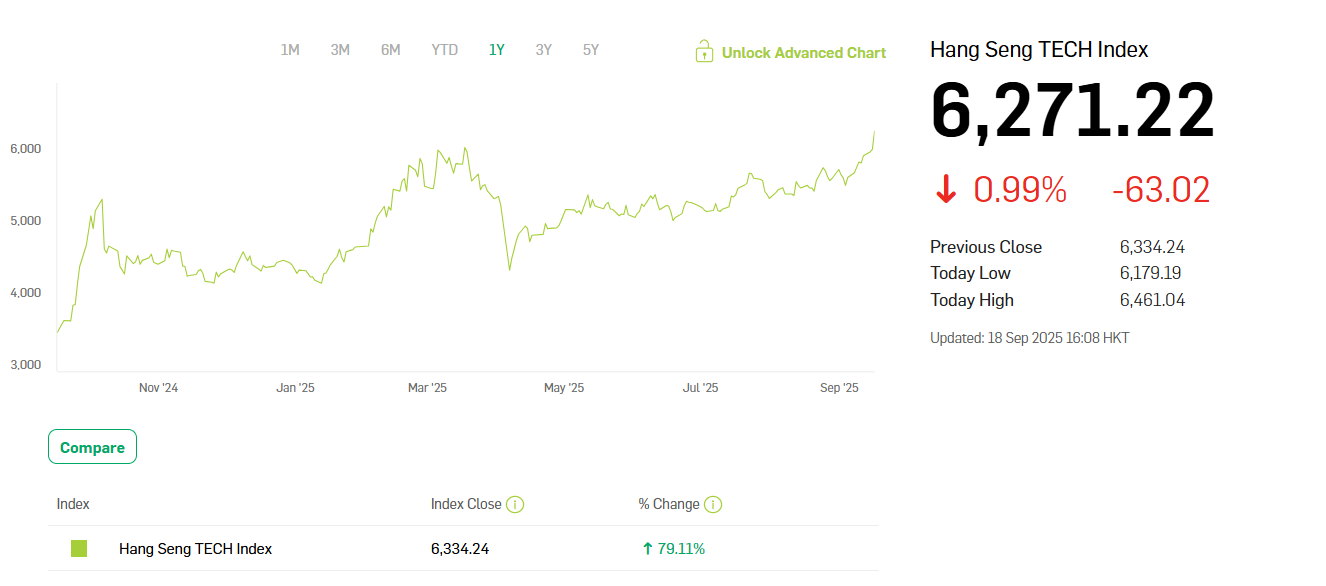

Asian markets were mixed: Hong Kong’s Hang Seng rose over 1%, China’s CSI 300 gained 0.4%, Japan’s Nikkei edged 0.2% higher, while South Korea’s KOSPI dropped more than 1%. Investors looked to the Fed’s updated projections and dot plot for guidance.

Analysis:

The Harmonized Index of Consumer Prices (HICP) for Europe, excluding energy and food, came in exactly as expected at 2.3%, and shows a slight slowdown from July’s 2.4%. This suggests underlying inflationary pressures are stabilizing, which may affect ECB policy decisions in the near term.

Markets Respond to Fed’s September Cut (09.18.2025)

The Federal Reserve cut rates by 25 bps to 4.00%–4.25% in September, its first move since December. Governor Stephen Miran dissented, favoring a 50 bps cut. The Fed signaled another 50 bps of easing by year-end and one cut in 2026, with GDP growth upgraded and 2026 inflation forecasts higher.

The dollar index held above 97, while Powell called the move “risk management” amid labor softness. The Bank of Canada also cut rates, while the BoE and BoJ are expected to stay on hold.

US 10-year yields hovered near 4.07% as stocks reacted to the Fed’s guidance. Futures rose, but Cracker Barrel shares fell over 9% on weak earnings. The Dow gained 0.57% Wednesday, while the S&P 500 slipped 0.1% and the Nasdaq lost 0.33%.

Asian markets advanced, led by Japan’s Nikkei, hitting a record 45,296.21, and gains in South Korea’s KOSPI. Chinese and Hong Kong stocks were mixed, though Shanghai indexes touched decade highs.

China’s outright ban on Nvidia’s AI chips has sent shockwaves across global tech markets while sparking a strong rally in local Chinese technology shares. The move highlights Beijing’s determination to reduce reliance on U.S. hardware and strengthen its domestic AI ecosystem, even if it comes at the cost of limiting access to leading-edge chips.

Local investors quickly shifted their focus toward domestic semiconductor firms. Companies engaged in chip design, cloud computing, and AI infrastructure saw their stocks rise sharply as market participants anticipated stronger government backing and increased demand for homegrown solutions. This optimism has driven Chinese tech indices to their seventh consecutive weekly gain.

Analysts suggest that this ban is not only about restricting U.S. technology but also about creating room for Chinese firms to dominate the AI supply chain. By closing the door to Nvidia, Beijing is effectively pushing its own companies to accelerate innovation and capture market share. In the short term, there may be a technology gap, but the long-term strategy aims to ensure greater independence.

For global investors, the move underlines the risks of geopolitical tensions spilling into technology markets. While Nvidia faces a loss of one of its biggest markets, Chinese firms may see this as an unprecedented opportunity. Whether local players can match Nvidia’s scale and expertise remains uncertain, but investor sentiment in China suggests strong faith in the government’s support for its domestic champions.

Fed Rate Cut Lifts US Stocks, Inflation in Focus (09.19.2025)

US stocks hit fresh records after the Fed’s 25-bps rate cut, with the Dow up 0.27%, S&P 500 0.48%, and Nasdaq 0.94%. Tech led gains as Intel surged 23% on a $5B Nvidia partnership, while Nvidia, Palantir, Coinbase, and CrowdStrike also rallied.

The 10-year Treasury yield held near 4.11% and the dollar index around 97.4. The Fed signaled two more cuts in 2025 but only one in 2026, with Powell calling the move “risk management” amid labor weakness. Jobless claims fell, supporting the dollar, while QT continued. The Bank of Canada also cut rates, while the BoE held steady.

Japan’s inflation eased to 2.7% in August, the lowest since late 2024, as energy subsidies and slower food inflation helped. In the UK, the BoE kept rates at 4% in a 7–2 vote, slowed gilt sales, and maintained a cautious stance as CPI held at 3.8% with weak growth and softer labor data.

German 10-yearBund yields climbed toward 2.75% , their highest since Sept 2, following a volatile week driven by larger debt issuance plans and major central bank decisions.

Markets Keep Steady After Fed Cut (09.22.2025)

EUR/USD slipped to 1.1747 after the Fed’s 25-bps cut, while USD/JPY held near 148. Fed officials signaled a gradual, data-dependent approach to easing.

Gold traded around $3,685, supported by the Fed’s move and Powell’s “risk management” message, reinforcing its safe-haven role.

US tech stocks extended gains, with the Tech 100 Index at 24,654, up 0.7% daily and 24% yearly. Forecasts point to a mild correction as profit-taking and valuations weigh on further upside.

Bostic sees one rate cut in 2025 as sufficient, though this could change depending on economic conditions. Markets, however, are pricing in 50 basis points of easing, equivalent to two cuts.

Markets Pause Before Data and Policy Updates (09.23.2025)

Markets were steady on Tuesday as investors awaited key economic indicators and central bank signals. The euro hovered near $1.18, supported by expectations that Eurozone PMIs will show modest improvements in both manufacturing and services.

The yen strengthened to 147.5 per dollar as the greenback eased, with traders eyeing political uncertainty in Washington and steady BoJ policy. Gold climbed above $3,750, fueled by Fed rate cut bets, while silver retreated to $43.80 after touching fresh multi-year highs. The pound traded near $1.35, weighed down by fiscal concerns and awaiting PMI data.

Markets Keep Steady While Metals Pull Back (09.24.2025)

Global markets were mixed on Wednesday as central bank signals and data shaped sentiment.

The euro slipped below $1.18 after weak Eurozone PMIs, with the ECB hinting its rate-cut cycle may be ending. The pound held near $1.35 but faced pressure from rising UK public borrowing. The yen weakened toward 148 per dollar as Powell stressed caution on future Fed cuts, while the offshore yuan eased to 7.11 after a two-day rally.

Gold stayed near $3,750 despite a slight dip, supported by Fed easing expectations. Silver pulled back from 14-year highs, while Brent crude climbed toward $68 on falling U.S. inventories and WTI slipped below $62 on oversupply worries.

Equities saw volatility, with the US 100 Tech Index down 0.73% after recent highs. Megacap stocks like Nvidia, Apple, Oracle, and Tesla remained key drivers. Bitcoin rebounded above $112,000, gaining over 2% in four weeks.

XAUUSD – Gold touched $3,760/oz in Asia, near record highs. Powell called the balance between inflation and a weakening labor market “challenging,” while Bowman hinted at faster easing if the labor market softens.

The U.S. 10-year Treasury yield stabilized around 4.11% after a 5 bps drop in the previous session, while Japan’s 10-year government bond yield held near 1.65% , staying close to its highestlevel in 17 years.