EUR/USD tries to snap its record losing streak: The Week Ahead

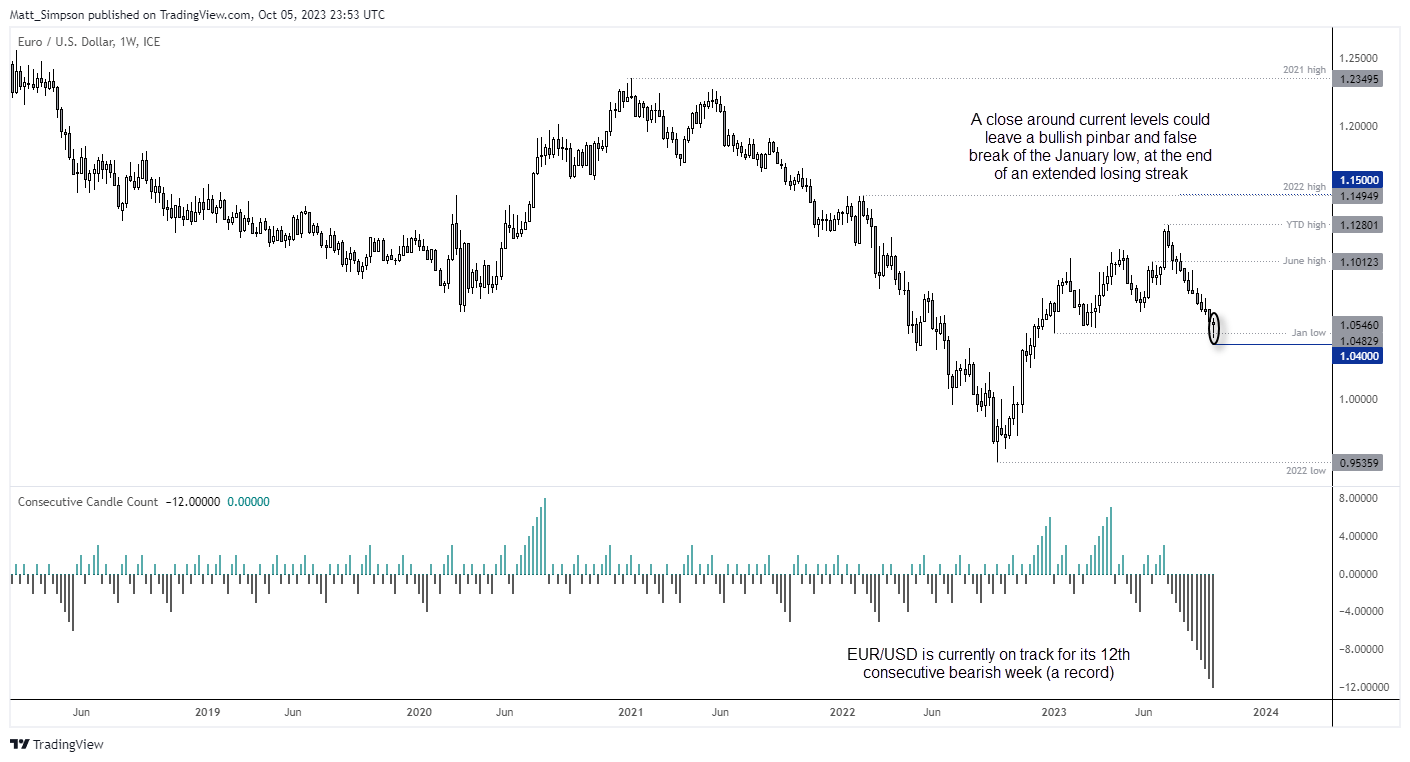

EUR/USD is on track for a record 12th consecutive losing steak. But given its hesitancy to test 1.04 and the potential for a false break of the January low, perhaps we’re finally nearing an inflection point for the battered EUR/USD.

Of course, to see this tide turn we’ll likely need to see a weaker US dollar. And that likely needs to see bond investors step up their game and suppressing worryingly high yields. And that means that for another week the performance of bond markets takes precedence over economic data, although next week’s US inflation report could exacerbate the bond rout if it comes in uncomfortably hot. We also have inflation data from China, along with key loan data and a trade balance report.

The week that was:

- It has not been an enjoyable start to the quarter for investors long risk so far, with rising bond yields continuing to choke sentiment

- A strong JOLTS job openings report alongside further hawkish comments from Fed members saw bets of another 25bpp Fed hike in November rise to around 30%, up from 16% according to Fed Fund futures

- Although a weak ADP job growth report generated some excitement that NFP could disappoint

- The bond market rout subsided by midweek, which allowed yields and the US dollar to pull back and let investors catch their breath and Wall Street find its footing ahead of NFP

- EUR/USD and AUD/USD lifted themselves from their cycle lows and gold is considering following them at the time of writing

- Plunging oil prices were met with mixed feelings, because whilst lower oil is deflationary the reason they were falling were due to concerns of a recession

- OPEC+ kept their oil output policy unchanged, although the risks of further output cuts are apparent if oil prices keep falling

- Bank of England’s deputy governor warned that whether they hike further remains an open question

- The ISM manufacturing showed signs of improvement with the main index contracting at its slowest pace in 10 months

- Rumours of a Bank of Japan (BOJ) intervention were rekindled with a 300-pip slide on USD/JPY shortly after it broke above 150

- The BOJ have remained silent on the topic, so we may need to wait until their November minutes to find out if they had indeed intervened

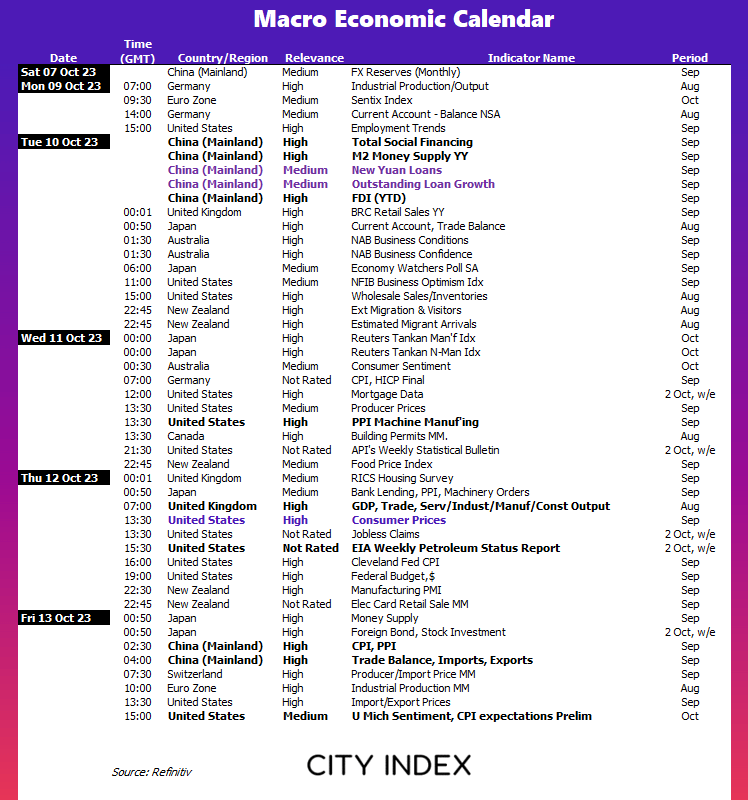

The week ahead (calendar):

This content will only appear on City Index websites!

This content will only appear on City Index websites!

Earnings This Week

Look at the corporate calendar and find out what stocks will be reporting results in Earnings This Week.

The week ahead (key events and themes):

- Global bond rout, USD rally

- US inflation, producer prices

- China inflation, trade balance, loan data

- UK data dump (GDP, industrial production, manufacturing production)

- US consumer sentiment

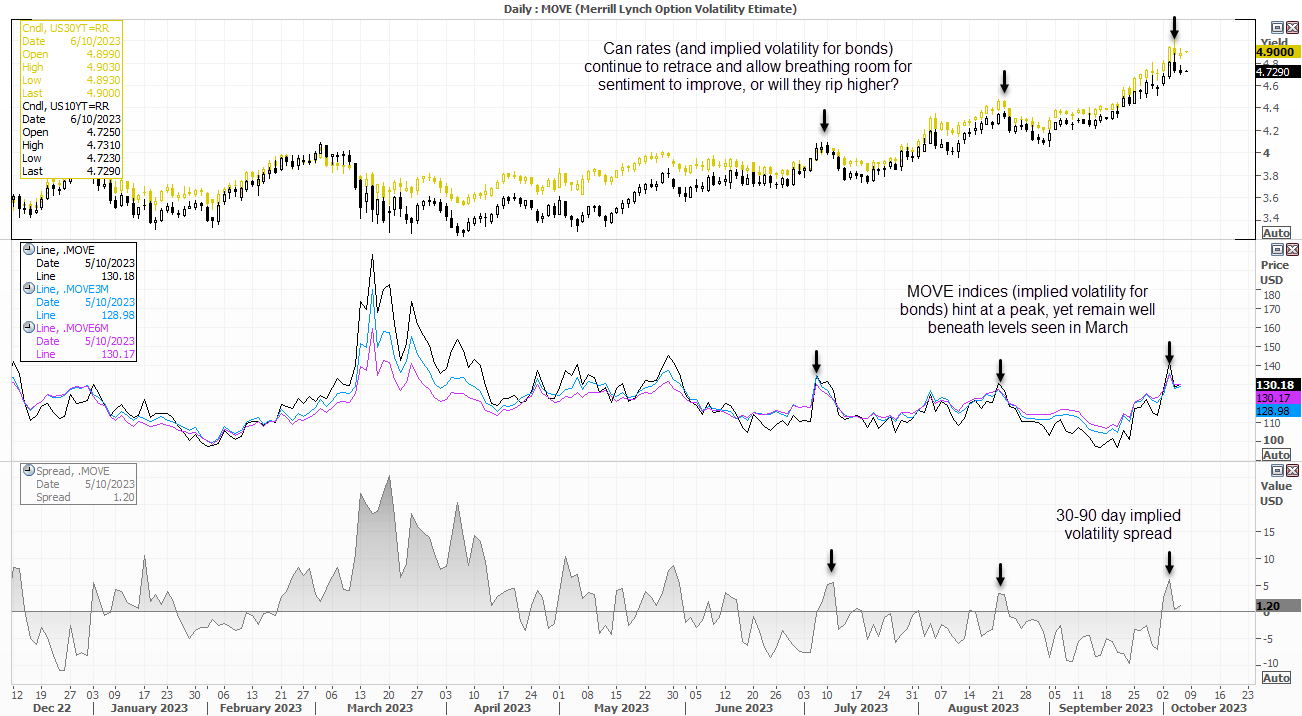

Global bond rout

This week I noticed a rise of alarms bells being rung across social media, from veteran traders who are not usually over sensational. And I’ll admit to it making me a tad worried. When I pulled up a 10-year bond price chart and noted a lack of support for the 10-year prices, I had to ask myself if bondcano really is just getting started. Either way, the plunge in bond prices and its drastic impact on rising yields remains a key driver for market sentiment. And if they pull back from their highs, it could provide breathing room for appetite for risk to make a return.

Market to watch: Yields, EURUSD, USD/JPY, WTI Crude Oil, Gold, S&P 500, Nasdaq 100, Dow Jones, VIX, AUD/JPY

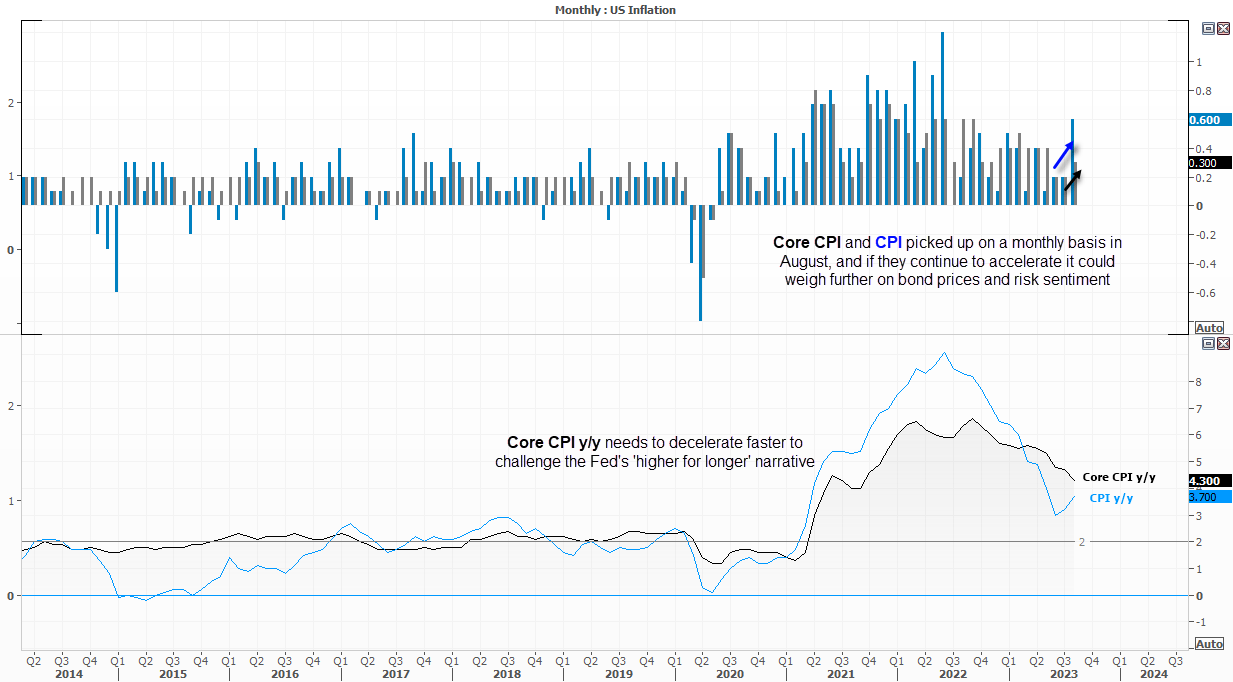

US inflation, producer prices

Whilst the bond rout takes centre stage, next week’s inflation data is the next in line as it could have a direct impact on bonds (and therefore global assets). We saw the monthly gauge of CPI and core CPI rise in August, and if they continue to accelerate it could exacerbate the bond rout to send yields and the US dollar higher, to the detriment of risk appetite. It would likely take a particularly soft inflation report to restore appetite for risk, but right now I think battered investors would be happy with a pause from rising yields.

Also note that producer prices are released for the US, which are a key inflationary input for consumer prices.

Market to watch: EURUSD, USD/JPY, WTI Crude Oil, Gold, S&P 500, Nasdaq 100, Dow Jones

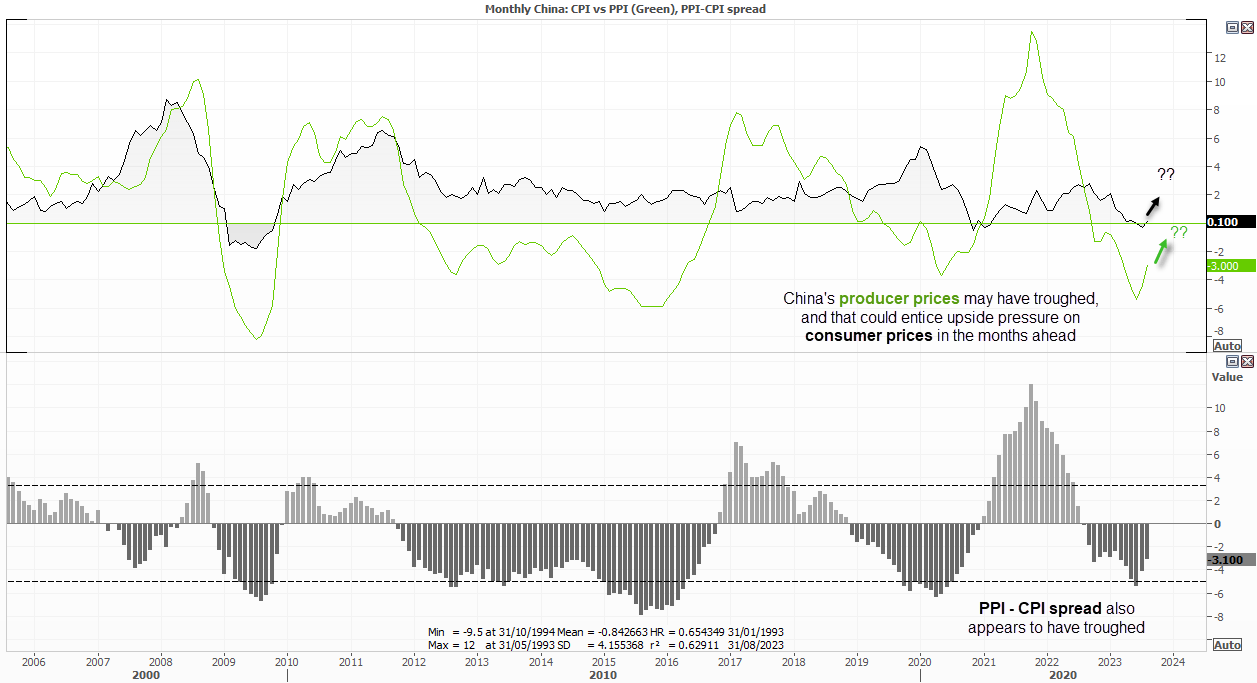

China inflation, trade data, investment, loans

A little scenario planning can go a long way, especially when it comes to trading. But if we are to find that consumer prices for the US and China are rising in tandem next week, it could have a huge knock-on effect for markets. And that is not particularly so far fetched given China’s producer prices have seemingly troughed and CPI rose 0.1% y/y after a since month of deflation.

Loan data will also reveal if the pickup in loan demand is sustained, but failure to do so points to softer growth prospects. We’ll also keep an eye on trade data to see if there’s been a pickup in domestic and overseas demand.

Market to watch: USD/CNH, USD/JPY, S&P 500, Nasdaq 100, Dow Jones, VIX, AUD/JPY

EUR/USD weekly chart:

At the time of writing, EUR/USD is on track for its 12th consecutive bearish week. According to data from ICE (intercontinental Exchange), the previous record for losing weeks was 10 – so it set a record last week. If I look at the bond rout and rising yields, it is one of those macro moves that simply makes a mockery of traditional technical analysis and their ‘overbought’ or ‘oversold’ levels. But then I look at the EUR/USD weekly chart and seriously question if we’re at or near an inflection point for the US dollar. And if so, that also assumes bond yields are also near or at an inflection point.

Unless today’s nonfarm payroll report is outrageously strong, EUR/USD might be able to close the week above the January low and deem the initial break as a ‘fakeout’. If it closes at or above current levels, EUR/USD would also have a bullish hammer week up its sleeve. And whilst that doesn’t guarantee we’ll see a sharp rebound from current levels, it should at least serve as a warning for EUR/USD bears, and excite EUR/USD bulls who want to quietly load up at these lows in hope of an eventual rally – which assumes a weaker US dollar and bond yields.

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.