My apologies Jason! Won’t happen again :)!

[B]Written by David Rodriguez[/B]

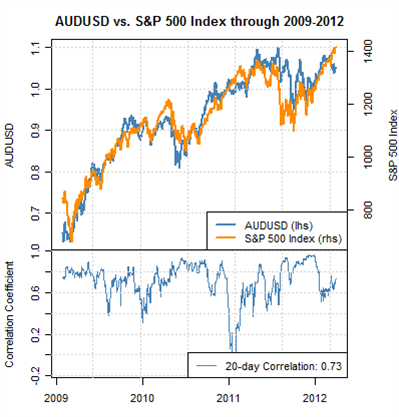

[B]There is a clear fundamental reason for why the Australian Dollar will likely remain correlated to the US S&P 500 through the foreseeable future: yield differentials.[/B]

Last week we wrote that the AUDUSD and S&P 500 correlation was trading near its lowest levels in many months, but a sharp rally in both stocks and the Aussie Dollar suggests that the correlation is back and nearly as strong as ever. Indeed, we were confident it would return to strength as the reasoning falls to pure market fundamentals.

The Australian Dollar boasts the highest interest rate of any G10 currency, while the US Dollar is near the lowest. According to London Interbank Offered Rates (LIBOR)—the price at which banks lend to one another in the interbank markets—the overnight US Dollar rate is a mere 0.15% while the equivalent Australian Dollar yield is 4.42%.

In theory this means that an investor would stand to gain 4.27% annual yield for simply borrowing US Dollars to buy its Australian counterpart. In practice one would not collect this full yield due to spreads paid on interest rates, but the net yield should still be fairly significant.

That yield becomes all that much more important if the AUDUSD exchange rate remains unchanged or appreciates, but the investor could lose significantly if the Australian Dollar falls at a greater than 4.27% rate on an annualized basis. To put that into perspective, an AUDUSD exchange rate of $1.0480 implies that an investor would lose if the Aussie fell more than 1.7 pips ($0.00017) per day against the US Dollar. (Based on a 250-day yearly trading calendar and using the assumption the investor receives the full 4.27% yield differential)

If investors don’t fear AUDUSD declines, they might gladly take that risk in expectations that yields would reward them over the course of the year. Of course the opposite is also true: they would likely run for the exits if the Aussie looks like it will fall significantly against its low-yielding US namesake.

This dynamic explains why the Australian Dollar will likely remain correlated to the US S&P 500 and other speculative assets through the foreseeable future. Can that correlation break down for weeks at a time? Of course. Past performance is not indicative of future results.

Yet it would take a substantial shift in yields to truly turn the AUDUSD’s link to the S&P and other markets. Look to Reserve Bank of Australia and US Federal Reserve as the two entities who could alter this dynamic via changes in Australian and US interest rates.

[I]Source: Why is the Australian Dollar Correlated to the US S&P 500? | DailyFX[/I]

Written by Jamie Saettele

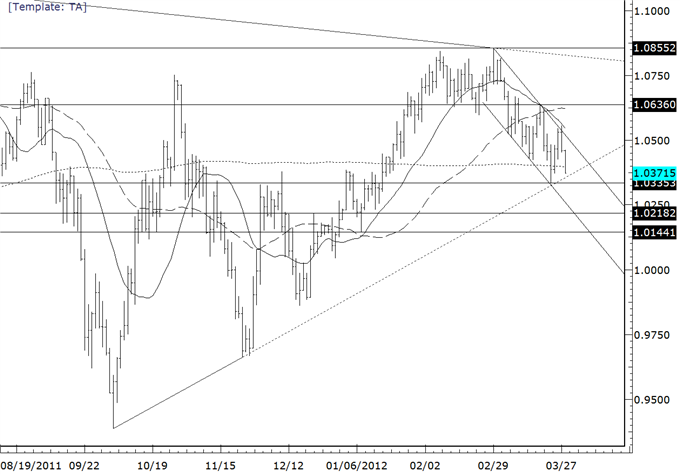

[I]AUDUSD[/I] – I wrote last night that “the AUDUSD has significantly lagged equities throughout March. In fact, price has trended lower and adhered to trendline resistance throughout March yet the S&P 500 traded to a nearly 4 year high yesterday. A lagging market is a market at risk.” The AUD is weak across the board as the biggest losers at the US open are AUDJPY, AUDUSD, and AUDCAD. Resistance in AUDUSD is 10425/75. A break would target former pivots at 10150/10200.

[B]AUD/USD[/B]

[I]Source: Australian Dollar is Biggest Loser as Price Nears Lows | DailyFX[/I]

[B]Written by David Song[/B]

[B][U]Euro: Portugal Sees Larger Contraction In 2012, EU Summit In Focus[/U][/B]

The EURUSDextended the decline from earlier this week as the Organization for Economic Cooperation and Development talked up the risks surrounding the euro-area, and the exchange rate may weaken further over the remainder of the week as the fundamental outlook for the region turns increasingly bleak. Indeed, the OECD argued that the ‘firewall still needs to be further strengthened’ as the situation in Europe ‘remains fragile,’ and went onto say that the accommodative policy stance held by the European Central Bank ‘will be warranted for a considerable time to come’ as the region faces a risk for a prolonged recession.

At the same time, the Bank of Portugal warned of a larger contraction in 2012 as central bank officials expect to see a 3.4% decline in the growth rate, and the weakening outlook for the euro-area should continue to drive the exchange rate lower as European policy makers struggle to stem the risks surrounding the region. As the EU Summit comes into focus, there’s speculation that the group will expand the scope of the bailout fund to a whopping EUR 940B to stem the risk for contagion, but the developments coming out of the meeting may fail to prop up the euro should policy makers struggle to meet on common ground. As the EURUSD carves out a lower top going into April, we should see the exchange rate continue to give back the advance from earlier this month, and we may see the pair fall back towards 1.3000 in the days ahead as the outlook for the region deteriorates.

[B][U]British Pound: U.K. Data Disappoints, Sideways Price Action Ahead[/U][/B]

The British Pound pared the overnight advance to 1.5933 amid the slew of negative developments coming out of the U.K., and the GBPUSD may continue to give back the advance from earlier this month as market participants maintain bets for more quantitative easing. However, as the GBPUSD maintains the range carried over from the previous month, we should see 1.5600 provide near-term support, and the pair may continue to track sideways in April as market participants weigh the outlook for monetary policy. Although the Bank of England expects to see a stronger recovery in 2012, the slew of dismal data certainly points to a protracted recovery, and the Monetary Policy Committee may keep the door open to expand the Asset Purchase Facility beyond the GBP 325B target in an effort to balance the risks surrounding the region.

[B][U]U.S. Dollar: Upward Trend To Gather Pace, Fed Rhetoric On Tap[/U][/B]

The greenback regained its footing coming into the North American trade, with the Dow Jones-FXCM U.S. Dollar Index (Ticker: USDOLLAR)bouncing back from an overnight low of 9,941, and the reserve currency may push higher going into April as it maintains the upward trend from earlier this year. With Fed officials scheduled to speak later today, the central bank rhetoric is likely to heavily influence the dollar, and less dovish comments from Mr. Dennis Lockhart and Mr. Charles Plosser should increase the appeal of the USD as market participants scale back expectations for more quantitative easing.

[I]Source: Euro To Weaken Further On Growth Concerns, EU Summit In Focus | DailyFX[/I]

[B]Written by Christopher Vecchio[/B]

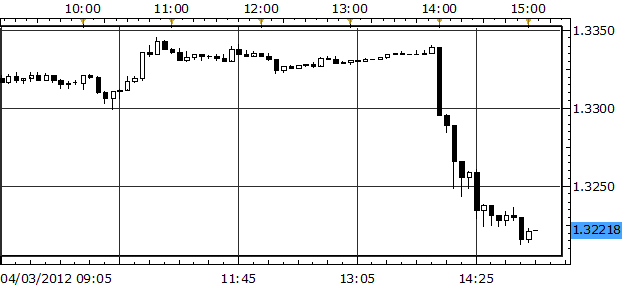

The Federal Reserve’s policy meeting on March 13 was decisively neutral. Indeed, with the statement accompanying the decision suggesting that sentiment among policymakers was broadly neutral, the minutes from the meeting – released at 18:00 GMT today – highlighted the recent ‘hawkish’ shift among voting members.

Equity markets plunged after the minutes were released, with the S&P 500 dropping approximately 9-points from its pre-release level. The AUDUSD and EURUSD sold-off with fervor, with the former dropping by 60-pips and the latter plummeting by 120-pips. The Japanese Yen was also substantially weaker, with the USDJPY climbing 80-pips after the release. Broadly speaking, the U.S. Dollar was the best performer with the Dow Jones FXCM Dollar Index (Ticker: US Dollar) cracking the psychologically significant 10,000 level.

[B]EUR/USD 1-minute Chart: April 3, 2012[/B]

[I]Charts Created using Marketscope – Prepared by Christopher Vecchio[/I]

Key points from the FOMC statement:

[ul]

[li]FOMC saw no need to ease anew unless growth slows, and officials saw economy “expanding moderately” last month.

[/li][li]“Labor market conditions continued to improve and the unemployment rate declined further, though it remained elevated.”FOMC participants saw jobless rate gradually declining.

[/li][li]Housing market “remained depressed”, expected housing to slowly recover.

[/li][li]“Overall consumer price inflation was relatively subdued in recent months”. “Measures of long-run inflation expectations remained stable. Most FOMC participants expected inflation rate at 2% or less.

[/li][li]Near-term forecast for real GDP growth revised up slightly. In its March forecast, the FOMC”s projection for real GDP growth over the medium term was somewhat higher than in January, mostly reflecting an improved outlook for economic activity abroad, a lower foreign exchange value for the dollar and a higher project path of equity prices. FOMC continued to forecast that real GDP growth would pick up only gradually in 2012 and 2013.

[/li][li]Significant outlook change could alter 2014 rate plan.

[/li][li]Economy facing continuing headwinds, members generally expected a moderate pace of economic growth over coming quarter with gradual further declines in the unemployment rate.

[/li][li]A couple of members indicated that the initiation of additional stimulus could become necessary if the economy lost momentum or if inflation seemed likely to remain below its mandate-consistent rate of 2 percent over the medium run.

[/li][/ul]

Was the market reaction following this commentary warranted? Perhaps not, considering these beliefs were well-established back at the March 13 meeting. Regardless, it is important to consider what will happen going forward. It should be noted that the meeting occurred before Chairman Ben Bernanke opened up the last week of March with remarks that more easing could be warranted should the labor market continue to struggle.

By no means is this a suggestion for more QE – I am ardently against more easing – but rather a reminder that Chairman Bernanke has already eased off the hawkish tones in the time period between the March 13 meeting and the release of the minutes on April 3. Should economic conditions deteriorate over the coming weeks - slow growth out of Asia and Europe will hurt the U.S. economy - the FOMC’s tone could revert quickly.

[I]Source: ’Hawkish’ FOMC Minutes Dampen QE3 Hopes, Send U.S. Dollar Soaring | DailyFX[/I]

[B]Written by David Rodriguez[/B]

The Euro/Swiss Franc exchange rate hit its lowest levels since September, 2011, and extremely one-sided retail forex trader positioning sets the stage for major volatility in the days ahead. How can we trade it?

The Euro/Swiss Franc exchange rate trades dangerously close to the Swiss National Bank’s stated floor at the SFr 1.2000 mark, and forex trading speculators have taken notice.

Our proprietary FXCM Speculative Sentiment Index data shows that the number of traders long the Euro/Swiss Franc outnumber those short by a massive 41 to 1. In other words—nearly 98% of traders in our sample are currently long the Euro against the Swiss Franc. This falls just short of the record set in February when the EURCHF fell to $1.2030, but the day’s not over and we could conceivably hit fresh peaks in our SSI.

[B]Euro/Swiss Franc Chart Shows Retail Positioning Near Record Long[/B]

Data Source: FXCM Execution Desk DataChart Source: TradeStation

[B]What happens next? Are forex speculators justified in positioning for Euro/Swiss Franc bounce?[/B]

The obvious question is whether such incredibly one-sided sentiment points to a Euro/Swiss Franc exchange rate bounce. When we saw similar extremes on the last decline towards SFr 1.2030, the EURCHF inched higher without any obvious prodding from the Swiss National Bank. Yet as we trade closer to the critical SFr 1.2000 mark, the threat of a showdown looms large and promises a great deal of volatility.

The Swiss National Bank remains committed to its EURCHF floor and as such stands ready to intervene at any moment. Such consistency in message and mission suggests that traders are justified in taking positions. Yet it seems unlikely that the SNB would essentially give speculators risk-free profits and we urge caution against taking aggressive positions against the lows.

[B]Nothing is Guaranteed, Risk of EURCHF Declines Remains Real Despite SNB Floor[/B]

Financial markets are not known for their kindness, and even the threat of Swiss National Bank intervention does not guarantee that the Euro/Swiss Franc rewards speculators and remains above SFr 1.20. The fact that traders are so heavily net-long EURCHF suggests that any intervention could be quite expensive.

As the central bank would buy the EURCHF, speculators would aggressively sell long positions and book profits. Such a move could potentially offset the intervention and indeed make it quite expensive for the SNB to maintain their floor. That’s exactly what we have seen in previous failed SNB interventions, and you can be sure that central bankers are acutely aware of said risks.

Could we potentially see the EURCHF dip below SFr 1.20? Absolutely. The Swiss National Bank could stick to its word and defend the floor, but that doesn’t rule out an intraday spike below to take a lot of speculators out of their positions. A “run on stops” and momentary dip below 1.20 seems entirely plausible when one considers that the SNB does not want to have speculators sell into major interventions.

[B]Trade setups for EURCHF[/B]

As traders we always want to know how we can take advantage of various opportunities, and we would be remiss to ignore the potential for a EURCHF surge. Yet we can’t ignore the risk of a decline, and such analysis suggests that the real opportunity could be to place buy entry orders below SFr 1.20 on the chance that the SNB makes a run on stop loss levels before intervening.

Is this guaranteed to work? Absolutely not. Yet we play probabilities, and in our opinion the SNB is unlikely to abandon its floor altogether. Time will tell whether this strategy proves successful.

Source: Euro/Swiss Franc Nears 1.20, Swiss National Bank Hovers-Trade Setups? | DailyFX

Written by David Song and Michael Boutros from DailyFX.com

Trading the News: U.S. Non-Farm Payrolls

What’s Expected:

Time of release: 04/06/2012 12:30 GMT, 8:30 EST

Primary Pair Impact: EURUSD

Expected: 205K

Previous: 227K

DailyFX Forecast: 200K to 250K

Why Is This Event Important:

The world’s largest economy is expected to add another 205K jobs in March and the ongoing improvement in the labor market should prop up the U.S. dollar as it dampens the Fed’s scope to push through another large-scale asset purchase program. As the recovery gets on a more sustainable path, we should see the FOMC continue to soften its dovish tone for monetary policy, and the committee may look to normalize monetary policy towards the end of the year as the outlook for growth and inflation picks up. However, as market participation tapers off ahead of the holiday weekend, we may see whipsaw-like price action across the major currencies, and we will be prudent going into the event in an effort to preserve our capital.

Recent Economic Developments

As the economic recovery gradually gathers pace, businesses across the U.S. may continue to ramp up their labor force, and a marked rise in employment could push the EURUSD back below 1.3000 as market participants scale back expectations for more quantitative easing. However, easing demands paired with the slowdown in production could drag on hiring, and we may see the FOMC carry its zero interest rate policy into 2013 in an effort to encourage a stronger recovery. In turn, a dismal NFP report could spark a sharp rebound in the EURUSD, and we may see the pair maintain the range carried over from the previous month as market participants weigh the prospects for future policy.

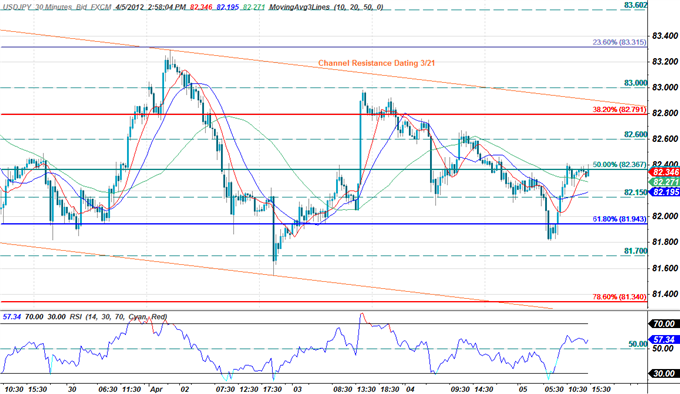

Potential Price Targets For The Release

Although the EURUSD will be our primary focus for NFPs, we will also be watching the USDJPY as the pair tends to show a notable reaction to U.S. event risks. A look at the encompassing structure sees the USD/JPY trading within the confines of a flag formation off the March highs as the pair consolidates after its nearly 800 pip run off the February lows. Key daily support rests with the 23.6% Fibonacci extension taken from the February advance just below the 82-figure, with channel resistance limiting topside advances in the interim. While our medium-term bias on the pair remains weighted to the topside, the current correction is likely to persist so long as the RSI remains within the confines of the descending channel formation.

Our 30min scalp charts once again highlights intra-day support at the 61.8% Fibonacci retracement taken form the March advance at 81.94. A break below this level risks further dollar losses with subsequent support targets seen at 81.70, the 78.6% retracement at 81.34 and the 81-figure. Interim topside resistance stands with the 50% retracement at 82.35 backed by 82.60 and the 38.2% retracement at 82.80. A breach above channel resistance alleviates some of the pressure on the pair with such a scenario eyeing targets at the 83-figure, the 23.6% retracement at 83.30 and 83.60. Should the print prompt a bullish dollar response look to target topside levels with a break above 83.60 offering further conviction on our medium-term bias.

How To Trade This Event Risk

As market participants anticipate to see another 200+K rise in NFPs, the data certainly highlights a bullish outlook for the greenback, and the market reaction could pave the way for a long U.S. dollar trades as market participants scale back bets for QE3. Therefore, if we see the print come in-line or above forecast, we will need to see a red, five-minute candle subsequent to the release to establish a sell entry on two-lots of EURUSD. Once these conditions are fulfilled, we will place the initial stop at the nearby swing high or a reasonable distance from the entry, and this risk will generate our first objective. The second target will be based on discretion, and we will move the stop on the second lot to cost once the first trade hits its mark in order to preserve our profits.

In contrast, easing demands from home and abroad paired with the slowdown in production may bear down on hiring, and a soft labor report could renew expectations for additional monetary support as the Fed aims to foster a stronger recovery. As a result, if the development falls short of forecast, we will implement the same strategy for a long euro-dollar trade as the short position laid out above, just in the opposite direction.

Impact that the U.S. Non-Farm Payrolls report has had on USD during the last month

Employment in the world’s largest economy increased another 227K in February following the 284K rise the month prior, and the ongoing improvement in the labor market certainly dampens the Fed’s scope to expand its balance sheet further as the recovery gathers pace. The above-forecast print propped up the dollar, with the EURUSD slipping below 1.3100, but we saw the pair consolidate throughout the North American trade as the exchange rate settled at 1.3116 going into the close.

Source: EURUSD: Trading the U.S. Non-Farm Payrolls Report | DailyFX

Your analysis methods are nice… I will follow your analysis… Thanks for Your Information sharing…

Thanks Susan, I’m glad you are finding the information useful.

Jason

[I]By Michael Boutros, Currency Strategist[/I]

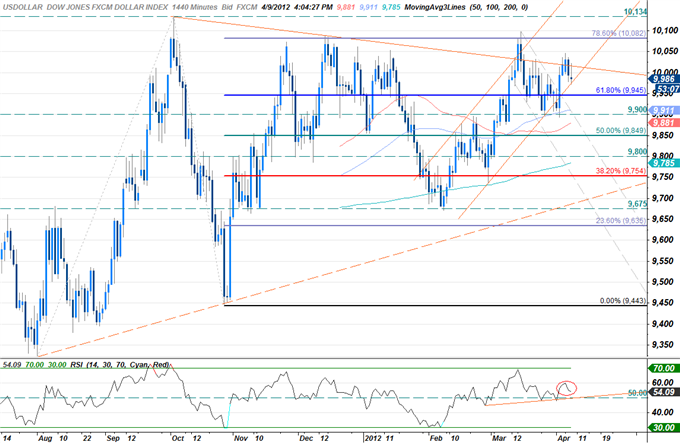

The greenback is fractionally softer at the close of North American trade with the Dow Jones FXCM Dollar Index (Ticker: USDOLLAR) off by 0.10% on the session. The losses come on the back of another sell-off in stocks which reacted to Friday’s disappointing NFP print. Expectations for the addition of 205K were grossly overestimated with the data coming in at just 120K for the month of March. Although the unemployment rate ticked down to 8.2% from 8.3%, the decline can largely be attributed to discouraged workers leaving the labor force which in turn puts downside pressure on the unemployment rate. While the data is by no means justification for further Fed easing, speculation of another round of easing has limited dollar advances in the interim despite the broad-based risk sell-off seen in US trade today. By the close of trade in New York all three major indices were sharply lower with the Dow, the S&P, and NASDAQ off by 1.00%, 1.14%, and 1.08% respectively.

The dollar continues to trade within the confines of an ascending channel formation with the index testing trendline support just ahead of the close. While our medium-term bias on the greenback remains weighted to the topside, again we note that dollar advances may be limited in the interim as whispers of further Fed easing weigh on demand for the reserve currency. The correction may gather pace with a break below channel support eyeing key daily support targets at the 61.8% Fibonacci extension taken from the August 1st and October 27th troughs at 9945 and 9900. A break below this level coupled with a break below RSI support negates our bias with such a scenario eying the 50% extension at 9950.

An hourly chart shows the index trading within the confines of a newly formed descending channel formation with the dollar rebounding off soft support at 9975. Subsequent intra-day floors are seen at the 61.8% extension at 9945, former channel resistance and 9900. A topside break of the channel alleviates some of the pressure with topside resistance targets seen at 10,040, 10,060, and the 78.6% extension at 10,080. Look for the dollar to possibly drift lower before mounting its assault with dips in the index offering favorable long entries.

The greenback fell against all four component currencies highlighted by a 0.21% decline against the British pound. Despite the sterling’s pullback off the 1.60-figure, our medium-term bias remains cautiously weighted to the topside with the daily chart offering a clearly defined ascending channel formation dating back to the January 13th low. We favor buying into sterling weakness noting that a break below the 23.6% Fibonacci extension taken from January 13th and March 12th troughs at 1.5775 negates our interim bias. The Japanese yen was the weakest performer of the lot with an advance of just 0.02%. The yen quickly pared early losses that saw the pair dip as low as 81.19 before rebounding to close just below interim resistance at 81.60. For complete USDJPY scalp targets refer to today’s Winners/Losers report.

Tomorrow’s economic docket is rather light with only business/economic surveys and the February wholesale inventory report on tap. However with European markets coming back online tomorrow for the first time since NFPs printed last Friday, investors will be closely eyeing equity performances with concerns over China now coming more into focus. Chinese CPI data last night topped expectations with the year on year print coming in at 3.6%, missing calls for a read of just 3.4% y/y. The data comes off a previous print of 3.2% y/y a month earlier and suggests that price growth in China may be gathering pace, limiting the PBoC’s scope to further ease policy. As concerns about a possible “hard landing” in China take root, look for risk to remain on the defensive with traders eagerly anticipating GDP data out of China this Friday. The dollar’s future hangs in the balance with the index likely to trade within a tight range ahead of key trade balance and inflation data later this week.

[B][U]Upcoming Events[/U][/B]

Source: USD Drifts Amid Thin Trade, QE Speculation- Volume to Offer Clarity | DailyFX

Earlier today we saw the EUR/USD briefly drop below 1.3000 based on concerns that Spain could trigger another sovereign debt crisis. Here’s a chart DailyFX put together that shows the cost of insuring Spanish sovereign debt via CDS’:

The EUR/USD has since made a very strong bounce off of 1.30, but you should keep an eye out for any speculation of Spanish debt problems.

The full article from David Liu of DailyFX can be found here: Weekend: Early Markets Drifting, Looking to Earnings, Spain, China for Cues | DailyFX

Today’s Weekly Strategy Outlook from DailyFX lists the current bias for EUR/USD, USD/CHF, and NZD/USD as “Range” which probably shouldn’t surprise any of you that have been trading these pairs over the past couple of months.

Here’s a look at the complete bias list:

You can click here to read the entire Weekly Strategy Outlook at DailyFX.com

While ranges may not be the most exciting markets to trade, they can still present opportunities for those that are patient.

Tomorrow we have the FOMC release coming out, and this one is extra special since Bernanke will be giving a press conference after the release. Here’s what Ilya Spivak, DailyFX Currency Specialist has to say about it.

The focus now turns to the Federal Reserve monetary policy announcement due on Wednesday for an update on the other side of the equation. US economic data has increasingly to outperform relative to expectations since the last sit-down of the policy-setting FOMC committee (according to data from Citigroup). This may signal that the pace of recovery is once again faltering after a strong start to the year, replaying similar scenarios in 2010 and 2011. Alternatively, it may reflect a catch-up in economists’ expectations for US growth amid signs of genuine acceleration. A survey of analysts polled by Bloomberg hints the latter may indeed be the case. The median forecast for 2012 US GDP growth rose from 2.2 to 2.3 percent since the last Fed meeting, with upgraded expectations for the first, second and third quarters.

To read the full article at DailyFX.com, click here.

[I]By Christopher Vecchio, Currency Analyst[/I]

The British Pound has had a very interesting past twelve months. On April 28, 2011, the GBPUSD traded to its yearly high at 1.6745, but within six months, the pair had sunk to a new yearly low at 1.5270 on October 6. While the GBPUSD traded back towards 1.6000 in the fall, the start of 2012 was rocky for the Sterling, which saw the cable sink to a two year low of 1.5234 on January 13, 2012.

Recently, on the back of better than expected economic data, Bank of England policymakers began to shift away from their aggregate neutral if not dovish stance. Adam Posen, one of the two remaining doves calling for more quantitative easing on the Monetary Policy Committee, dropped his bid for looser policy. Traders have taken this shift in the MPC as a sign that rates will soon rise, and accordingly, have bid up the British Pound. The GBPUSD rose to a fresh yearly higher at 1.6170 earlier today in hopes that the first quarter growth reading for the United Kingdom would confirm the BoE’s outlook; instead, it now appears the British economy has dipped back into a recession, muddling the British Pound’s recent bullish momentum.

While there have been some improvements in the British economy over the past few months, the first quarter preliminary growth reading did not show it. On a quarterly basis, growth contracted by 0.2 percent after contracting by 0.3 percent in the fourth quarter of 2011; on a yearly basis, growth remained unchanged in the first quarter after growing by 0.5 percent in the fourth quarter of 2011. Of course, it is important to make note of the consensus forecasts, because those are the readings that helped propel the British Pound to fresh yearly highs against the US Dollar: quarterly growth was expected at 0.1 percent; yearly growth was expected at 0.3 percent. When considering the United Kingdom’s growth relative to that of the United States the past few quarters – 3.0 percent annualized in the fourth quarter of 2011 – the British growth picture looks even more dismal.

Thus, not only did the economy contract, growth was much worse than what was expected. While the British Pound fell across the board on the data release, the big question now is whether or not the BoE will reassess their outlook, and whether or not there will now be another liquidity injection in the coming months. Recent inflation data and other gauges of economic output suggest that more easing is possible.

Overall growth aside, inflation has been the biggest issue for BoE policymakers. Certainly the government’s fiscal austerity measures have helped ease price pressures, but beyond what has been already implemented, it appears that inflation won’t come off any further given the measures in place. In fact, after year-over-year price pressures peaked at 5.2 percent in September, they fell to their lowest level in February since November 2010. But inflation has already started to tick back up: the same gauge rose to 3.5 percent in March. A higher inflation outlook is one of the only impediments the BoE will have to implement more easing.

Beyond recent inflation data, trade data suggests that the renewed appeal of the Sterling over the first few months of 2012 has impeded economic growth prospects. Although only data from January and February is available, we do note that in both January and February import growth outpaced export growth. In fact, as exports dropped by 2.0 percent in February, imports rose by 0.2 percent. Similarly, while exports fell by 0.6 percent in January, imports expanded by 1.4 percent. Considering the Sterling’s performance against the United Kingdom’s largest trading partners in January and February, the recent trade data is surprising: the Sterling fell by 0.39 against the Euro in January and February; it lost 1.28 percent to the Swiss Franc; though it appreciated 2.35 by against the US Dollar.

A weaker Sterling is exactly what the British economy needs, however, especially against the Euro and the US Dollar. By further boosting exports, further investment could enter the country in order to help manufacturers meet foreign demand for British goods. Case and point: industrial and manufacturing production contracted by 2.3 percent and 1.4 percent, respectively, in February.

With growth slowing to the point where the economy teeters on the edge of a double-dip recession, it remains to be seen whether or not the BoE sticks to its recent hawkish rhetoric.Yesterday, MPC member David Miles said that his vote for more quantitative easing “looks vindicated” in light of recent data and the first quarter growth reading suggests this may be true. Accordingly, it is likely that the BoE backpedals away from their recent hawkish commentary. Just last week, it looked like the Sterling was set to be one of the best performing major currencies through the first half of the year; now, the Sterling is a bit more humbled, and so too are the BoE’s hawks.

[B]Forecast: GBPUSD to 1.5600 by the end of June[/B]

Source: British Pound Humbled as UK Slides into Double-Dip Recession | DailyFX

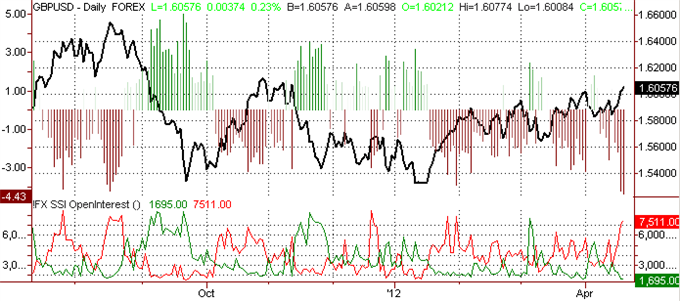

The SSI is reported Every Thursday at DailyFX.com.

British Pound Breakout Seems Unlikely

GBPUSD – Forex trading crowds have aggressively sold into recent British Pound strength, giving us contrarian signal that the pair may continue its rally against the US Dollar (ticker: USDOLLAR). Indeed, traders are now their most net-short GBPUSD since the pair rallied into its $1.65 highs through late 2011. Can we set a similar sentiment extreme and an important GBPUSD top through short-term price action? A hold of major trading ranges in other USD currency pairs suggests the GBP may likewise remain below highs. We hesitate to join such one-sided retail trading crowd sentiment, but a major break higher seems relatively unlikely without follow-through from other currency pairs.

— Written by David Rodriguez, Quantitative Strategist for DailyFX.com

Source: Forex Sentiment | Forex Technical Analysis | DailyFX

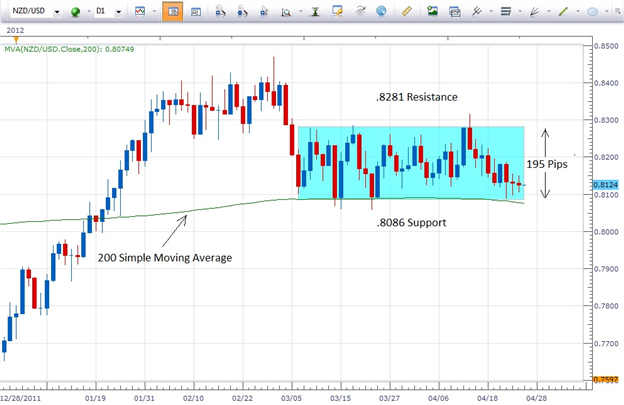

Oftentimes after a currency pair has been in a trend for a time, it will begin to consolidate or trade in a range. A trend trader can cease to trade the pair until it begins trending again or they can adjust their trading strategy so they can utilize what the market is giving them.

The NZDUSD currency pair is currently providing the trader with a consolidation zone.

Let’s take a look at the Daily chart of the pair below…

The pair has been consolidating since about the first week of March. During the consolidation it has respected a support level of .8086 and a resistance level of .8281…a range of 195 pips.

To a trader who would be interested in trading the pair while it is in the range, they could buy the pair when it is trading very close to support and place a stop below the lowest wick outside the range. Should the pair continue its pattern of trading up from support, the trader could set a limit at or close to the top of the range to exit the trade profitably.

When the pair is trading very near the top of range at resistance, a trader could short the pair with a stop just above the highest wick outside the range. Should price action continue to trade down from resistance, the trader could set a limit at or close to the bottom of range to exit the trade profitably.

Since this consolidation zone is just barely above the 200 Period SMA, there is not really a strong trading bias either to the upside or the downside on this pair.

A key to remember in range trading is not to enter a trade while price action is in the middle of the range. When price is in the middle, the trader loses the “edge” of which way the pair is more likely to move. Also, with price in the middle of the range, the placement of the stop will be a greater distance from the entry, thereby taking on a greater amount of risk.

We must remember that a consolidation zone can end at any time. Price can “breakout” of that zone/range at any time. For that reason it is imperative that protective stops be in place on a trade at all times.

Speaking of breakouts, when that occurs, here is how a trader can handle it…

If price simply breaks above/below the zone, a very aggressive trader can choose to enter at that point. A break to the upside would mean that a trader would take a long (buy) position with a stop below the bottom of the range.

However, as can be seen on the chart, there are several points where price broke out of the range, both above and below it, and then moved back within the range before the Daily candle closed. In other words price “wicked” above/below the range. In each of these cases the aggressive trader who entered on those entry signals would either have been stopped out or had to endure strong movements against their position.

A more conservative way to trade a breakout would be to hold off on entering the trade until a candle closes outside the zone. A candle closing outside the range (where the body of the candle remains outside the range as opposed to simply “wicking” outside the range) will signal a greater likelihood that the trade will continue to move in the direction of the breakout.

[I]—Written by Richard Krivo, DailyFX Trading Instructor[/I]

Source: Two Proven Ways to Trade a Consolidation Zone | DailyFX

[B]What’s Expected:[/B]

Time of release: [B]05/01/2012 4:30 GMT, 0:30 EDT[/B]

Primary Pair Impact: [B]AUDUSD[/B]

Expected: 4.00%

Previous: 4.25%

DailyFX Forecast: 4.00%

[B]Why Is This Event Important:[/B]

The Reserve Bank of Australia is widely expected to lower the benchmark interest rate by 25bp to 4.00% in May, and we may see the central bank carry out its easing cycle throughout 2012 in an effort to combat the slowing recovery. According to Credit Suisse overnight index swaps, market participants see borrowing costs falling by more than 100bp over the next 12-months, and the RBA may embark on a series of rate cuts going into the second-half of the year as the fundamental outlook for the $1T economy deteriorates.

[B][U]Recent Economic Developments[/U][/B]

The rise in private sector consumption paired with the jump in employment may allow the RBA to preserve its wait-and-see approach, and the development may ultimately produce a relief rally in the AUDUSD as market participants scale back speculation for lower borrowing costs. However, easing price pressures paired with the slower rate of growth may encourage the central bank to further support the ailing economy, and we may see Governor Glenn Stevens strike a very dovish outlook for monetary policy as the

[B][U]Potential Price Targets For The Rate Decision[/U][/B]

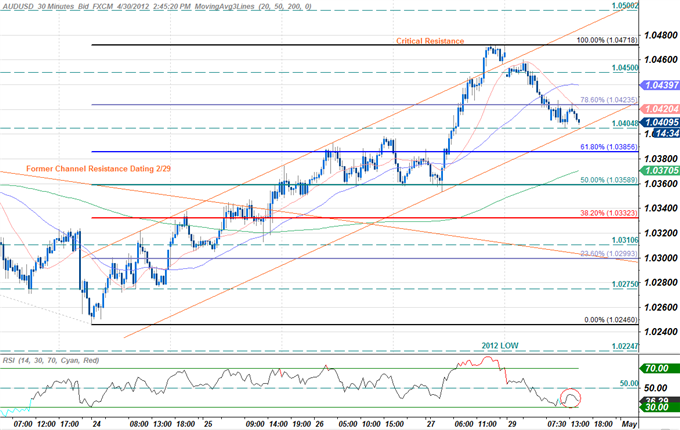

A look at the encompassing structure sees the AUDUSD breaking above the confluence of channel resistance dating back to March 6th, the 200-day moving average, and the 50% Fibonacci retracement of the December advance at 1.0360 last week before encountering resistance at the convergence of the 38.2% retracement and the 50-day moving average at 1.0475. We will reserve this level as our topside limit which if breached shifts our focus to subsequent resistance targets. Key support now rests at 1.0360 backed by the 61.8% retracement at 1.0240.

The scalp chart shows the aussie trading within the confines of an ascending channel formation after briefly breaching channel resistance on Friday. A break below this formation eyes interim support targets at the 61.8% Fibonacci extension taken from the April 10th and 24th troughs at 1.0385 backed by the 50% extension at 1.0360, and the 38.2% extension at 1.0330. A break below the 1.03-figure risks substantial losses with such a scenario eyeing soft support at 1.0275 and the April 24th low at 1.0246 with a move below the 2012 low at 1.0225 shifting our focus more aggressively to the short side. Interim resistance stands with the 78.6% extension at 1.0424 backed by 1.0450 and the April high at 1.0472. Should the print prompt a bearish response look to target downside levels with only a breach above the April high negating our bias.

[B][U]How To Trade This Event Risk[/U][/B]

Forecasts for a 25bp rate cut certainly instills a bearish outlook for the high-yielding currency, but the rate decision may foster a long AUDUSD trade should the RBA preserve its wait-and-see approach in May. Therefore, if the central bank keeps the benchmark interest rate at 4.25%, we will need a green, five-minute candle following the announcement to establish a buy entry on two-lots of AUDUSD. Once these conditions are fulfilled, we will place the initial stop at the nearby swing low or a reasonable distance from the entry, and this risk will generate our initial target. The second objective will be based on discretion, and we will move the stop on the second lot to cost once the first trade hits its mark in an effort to preserve our profits.

On the other hand, the RBA may sound increasingly dovish this time around as policy makers take note of the slowing recovery, and we may see the central bank take a more aggressive approach in stimulating the ailing economy as growth and inflation falter. As a result, should the RBA lower the key rate to 4.00% and highlight additional rate cuts for the coming months, we will carry out the same strategy for a short aussie-dollar trade as the long position laid out above, just in the opposite direction.

[B][U]Impact that the RBA Interest Rate Decision has had on AUD during the last meeting[/U][/B]

As expected, the Reserve Bank of Australia held the benchmark interest rate at 4.25%, but kept the door open to ease monetary policy further as ‘the board judged the pace of output growth to be somewhat lower than earlier estimated.’ The dovish done struck by the RBA dragged on the Australian dollar, with the AUDUSD slipping back below 1.0400, and the high-yielding currency continued to lose ground throughout the day as the pair closed at 1.0329.

— Written by David Song, Currency Analyst and Michael Boutros, Currency Strategist at DailyFX.com

Hi Everyone,

Due to the Golden Week holidays in Japan, all Yen crosses will have 5 days’ worth of rollover interest today except for GBP/JPY which will have 6 days’ worth.

For example, that means if you buy 10k of GBP/JPY and keep the trade open through 5pm New York time today, you will earn $0.66 or 66 cents. On the flip side, if you sell 10k of GBP/JPY and hold that trade open through 5pm, you will pay $1.56. You can always check what amount of rollover you can earn or pay for holding a particular currency pair through 5pm by looking at the RollS and RollB on the Trading Station.

And to keep track of when holidays will affect the number of days of rollover, you can look at the Rollover Calendar at DailyFX.com

Jason

[B][U]THE TAKEAWAY:[/U][/B] [U.S. NFP hiring in April rose less than expected, second month of slowdown; jobless rate falls slightly] > [Concerns U.S. economy could be losing momentum] > [USD gains vs. AUD]

Hiring in the U.S. in April was hugely disappointing, as the rise in nonfarm payrolls (NFP) fell for the second straight month. The U.S. Bureau of Labor Statistics (BLS) reported today that employees added 115,000 workers to their payrolls in April, down from March’s revised figure of 154,000, which was revised upwards from its original print of 120,000. The median forecast of 85 economists surveyed by Bloomberg News had called for an increase of 160,000. Private payrolls rose by 130,000 in April, down from 166,000 in March, while manufacturing added 16,000 jobs compared to 41,000 jobs a month ago. Employment increased in professional and business services, retail trade and health care, but fell in transportation and warehousing.

Meanwhile, the unemployment rate fell slightly in April to its lowest level since January 2009, declining to 8.1 percent from 8.2 percent the previous month. The drop in jobless rate was due to a continuing decline in the participation rate.

The large miss in NFP fueled concerns that the U.S. economy could be losing momentum, dampening hopes that a stretch of strong winter hiring had signaled a turning point for the economic recovery. The NFP print follows on the back of a disappointing rise in employment in April, according to the ADP’s national employment report that was released on Wednesday.

[B][I]AUDUSD 1-minute Chart: May 4, 2012[/I][/B]

Following the data release, the greenback initially weakened against most of its major currency peers. However, the U.S. dollar quickly reversed its losses against the higher-yielding currencies as the weaker employment figures weighed on risk sentiment and sent investors back to the reserve currency. After an initial dip, the U.S. dollar rose as much as 25 pips against the Australian dollar, and at the time of the report, the AUDUSD pair was trading at $1.0224.

— Written by Tzu-Wen Chen at DailyFX.com

[B]NEXT EVENT TO WATCH[/B]

[B]French Elections to be held on Sunday[/B]

It is highly likely that the French elections will impact the Euro, but over the medium- and long-term, not necessarily the day after the results are announced. French President Sarkozy is out of touch with the French people, an increasingly disgruntled populous becoming more averse to helping saving the notion of a broader Euro-zone. Case and point: Marine Le Pen, the president of Front National (FN), a far-right nationalist party, garnered approximately 18 percent of the vote during the first round of the French elections. Leading challenger Socialist Francois Hollande’s general platform differs greatly from that of Ms. Le Pen but they share one commonality: they both oppose how President Sarkozy has handled the European sovereign debt crisis. In fact, Mr. Hollande has sworn to renegotiate the European Union Fiscal Compact. He has also said that it’s time to concentrate on growth rather than austerity – as if economic growth in the current environment is that simple or was overlooked entirely the past few months.

If Mr. Hollande moves to repeal austerity measures and in the process frays France’s relationship with Germany, market participants will be hamstrung by political war games with the Euro as the collateral damage. Confidence would be lost in the Euro-zone’s core and leadership; bond yields will rise across the region; and the European Central Bank will be forced to act and if they don’t, the crisis could worsen. The international community (mainly via the International Monetary Fund) has been reticent in offering up a significant package of support, and I believe we’re done seeing more contributions to the ‘save Europe fund’ (loosely quoting Canadian Finance Minister Jim Flaherty). A Euro-zone without political leadership in union or support from a supranational agency, a crisis of confidence in the Euro-zone stoked by a difficult Mr. Hollande would easily sink the EURUSD below 1.2000.

— Written by Christopher Vecchio at DailyFX.com

[B][U]Trading the News: Australia Employment Change[/U][/B]

[B]What’s Expected:[/B]

Time of release: [B]05/10/2012 1:30 GMT, 21:30 EDT[/B]

Primary Pair Impact: [B]AUDUSD[/B]

Expected: -5.0K

Previous: 44.0K

DailyFX Forecast: -20.0K to 5.0K

[B]Why Is This Event Important:[/B]

Australia is expected to shed 5.0K jobs in April following the 44.0K expansion during the previous month, and the slowdown in the labor market may drag on the exchange rate as it dampens the outlook for the $1T economy. Indeed, the Reserve Bank of Australia lowered its forecast for growth and inflation as the central bank expected job growth to ‘remain subdued,’ and it seems as though the central bank will carry its easing cycle into the second-half of the year in an effort to encourage a sustainable recovery. According to Credit Suisse overnight index swaps, market participants still see the benchmark interest rate falling by nearly 100bp over the next 12-months, and we may see the RBA take a more aggressive approach in addressing the risks surrounding the region as the fundamental outlook for the world economy remains clouded with high uncertainty.

[B]Recent Economic Developments[/B]

The ongoing improvement in business confidence paired with the expansion in private sector consumption certainly bodes well for hiring, and a positive jobs report may push the AUDUSD back above the 23.6% Fibonacci retracement from the 2010 low to the 2011 high around 1.0350-60 as it dampens expectations for lower borrowing costs. However, the persistent slack in the real economy paired with the slowdown in world trade may lead businesses to scale back on employment, and a marked drop in job growth would heighten expectations for another rate cut as the RBA maintains a cautious tone for the region. In turn, we may see the AUDUSD continue to give back the rebound from 2011, and the pair may fall back towards the 38.2% Fib around 0.9930-50 as market participants look for a series of rate cuts from the RBA.

[B]Potential Price Targets For The Release[/B]

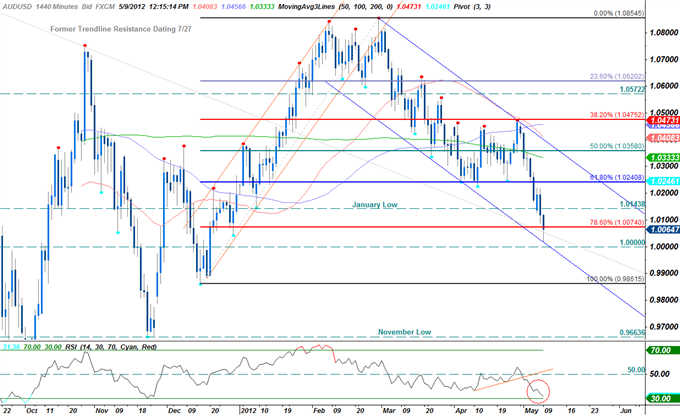

A look at the encompassing structure sees the AUDUSD trading within the confines of a descending channel formation dating back to the February 29th high with the pair rebounding off of channel support in early US trade. The aussie is at critical levels here with a break below parity risking accelerated losses for the high yielder. Daily resistance now stands at the 78.6% Fibonacci retracement taken from the December advance and is backed by the January low at 1.0140.

Our scalp chart shows the pair trading within the confines of an embedded descending channel formation with the rebound off channel support reinforcing the price action seen on the daily chart above. Soft interim support rests at 1.0020 backed by the 61.8% Fibonacci extension taken from the April 27th and May 7th crests at 1.0006. Interim topside resistance stands at the 50% extension at 1.0050 with a likely break here eyeing subsequent ceilings at the 38.2% extension at 1.0090 and 1.0115. Should the print prompt a bearish response look to target downside levels with a break below channel support offering further conviction on our directional bias. Such a scenario eyes downside targets at 9980, the 78.6% extension at 9950 and 9920.

[B][U]How To Trade This Event Risk[/U][/B]

Expectations for a drop in employment certainly casts a bearish outlook for the high-yielding currency, but a positive development could pave the way for a long Australian dollar trade as it dampens expectations for another rate cut. Therefore, if the region unexpectedly adds more jobs in April, we will need to see a green, five-minute candle following the release to generate buy entry on two-lots of AUDUSD. Once these conditions are met, we will set the initial stop at the nearby swing low or a reasonable distance from the entry, and this risk will establish our first objective. The second target will be based on discretion, and we will move the stop on the second lot to cost once the first trade reaches its mark in order to protect our winnings.

In contrast, the slowing recovery in Australia paired with decline in global trade casts a dour outlook for the labor market, and a dismal print could trigger a sharp selloff in the exchange rate as market participants expect to see a series of rate cuts from the RBA. As a result, if employment contracts 5.0K or greater from the previous month, we will carry out the same strategy for a short aussie-dollar trade as the long position laid out above, just in the opposite direction.

[B][U]Impact that the change in Australia Employment has had on AUD during the last month[/U][/B]

Employment in Australia jumped 44.0K following the 15.4K contraction February, while the jobless rate held at 5.2% for the second consecutive month in March. Indeed, the better-than-expected print propped up the Australian dollar, with the AUDNZD climbing back above 1.0350, and the high-yielding currency continued to gain ground throughout the day as the exchange rate closed at 1.0439.