Market Summary:

- The British pound was the strongest forex major on Monday after hawkish comments from the BOE and a surprise move from the British PM, Rishi Sunak

- David Cameron, the former UK PM who rolled the dice with the promise of a Brexit referendum if voted into power, is back in in government as foreign minister. The move by PM Sunak is seen as a requirement for a more centrist, experienced politician.

- BOE chief economist Huw Bill said inflation remains too high and warned that there was no sign of a turn in domestically-driven services inflation. However, he also said that the BOE do not need to deliver another rate hike but to remain restrictive (which means higher rates for longer)

- US 1-year inflation expectations softened to 3.6% from 3.7% prior, according to the New York Fed survey, with the 3-year remaining stable at 3% and the 5-year down to 2.7%

- Whilst two Fed members were scheduled to speak, neither commented on monetary policy ahead of today’s key US inflation report

- RBA’s assistant governor Marion Kohler warned that inflation may take longer to return to target than originally thought, as strong demand has allowed businesses to pass on cost increases. There’s also a concern that higher inflation will lead to higher inflation expectations.

- USD/JPY reached a 1-year high on Monday in Asian trade before dropping over 70-pips in the US session. Whilst the initial reaction may have been to point the finger at the BOJ, in all likelihood it would have moved far more than 70 pips and this could simply be an options play

- WTI crude oil rose for a second day after the OPEC monthly oil market report said that fundamentals remained strong and blamed speculators for the recent fall in prices

Events in focus (AEDT):

- 08:45 – New Zealand food price index

- 10:30 – Australian consumer confidence (Westpac)

- 11:30 – Australian business confidence (NAB)

- 18:00 – UK earnings, employment data

- 18:45 – SNB chairman Jordan speaks

- 19:00 – Spanish CPI, ECB Lane speaks,

- 19:45 – ECB’s Enria speaks

- 20:00 – IEA monthly report

- 21:00 – Eurozone GDP, employment, ZEW economic sentiment, German ZEW economic sentiment

- 21:30 – Fed Jefferson speaks

- 00:30 – US inflation

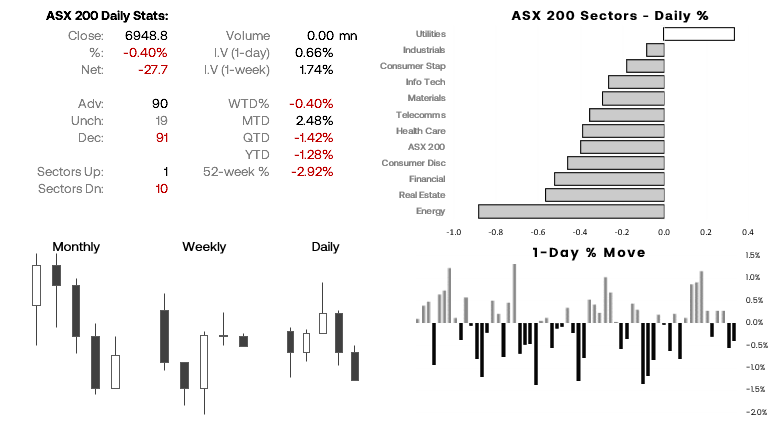

ASX 200 at a glance:

- The ASX 200 cash index fell for a second day on Monday, with 10 of its 11 sectors also trading lower

- Energy stocks led the way lower, although a recovery in oil prices overnight could help support the sector today

- Gains from Wall Street and SPI 200 futures overnight point to an open back above 7,000 for the cash index today

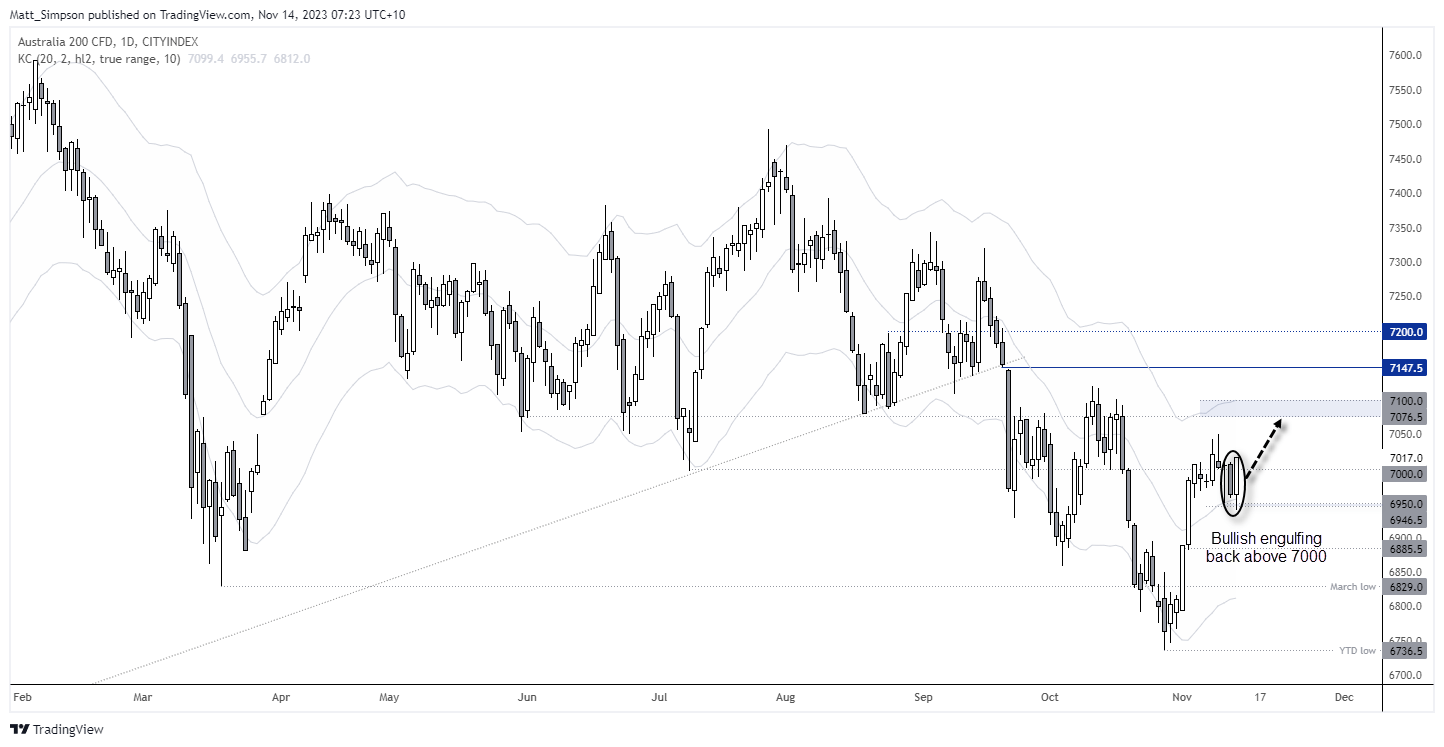

- Our chart below shows a bullish engulfing day formed after a false break of the 6946.5 low

- Today I’m looking for evidence of a swing low on the intraday charts around the 7,000 area or 6980 to seek longs

- Next upside target area for the index could be the 7076 – 7100 zone

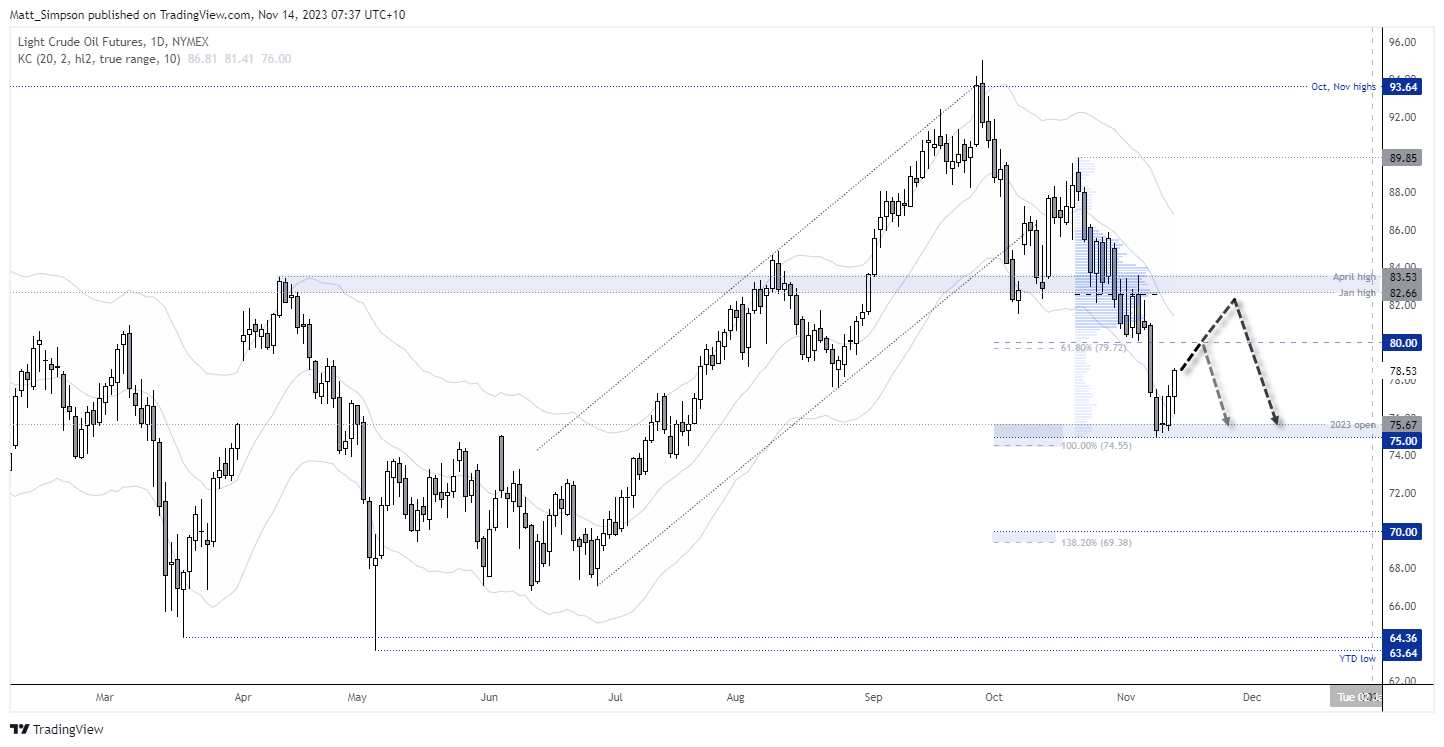

WTI crude oil technical analysis (daily chart):

I’m glad to say that my contrarian short bias against oil worked out quite well, having broken below $80 and reached $75 by the 100% projection ratio. However, mean reversion is now underway following its extended move beneath the lower Keltner band and has rallied for the second day in the row. A move back to $80 seems quite likely, given the depth of the prior move lower.

The big question now is whether WTI crude oil will leave evidence of a swing high around the $80 handle (for a potential swig trade short) or retrace higher still. Take note that the Jan / April highs sit around a high-volume node (HVN), which can act as a magnet for prices. And as volumes were relatively low beneath $80, perhaps the deeper retracement towards $83 is on the cards for bulls to consider targeting (and bears wait to fade into).

View the full economic calendar

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.