The much-ballyhooed May US labor market report came right in the “Goldilocks” zone for market participants: good enough to reignite modest optimism about the US economy; but not good enough to provoke a major drawdown in the Federal Reserve’s QE3 program.

[B]The important numbers:

[ul]

[li]Change in Nonfarm Payrolls: +175K versus +163K expected, from +149K (revised lower from +165K)

[/li][li]Change in Private Payrolls: +178K versus +175K expected, from +157K (revised lower from +176K)

[/li][li]Unemployment Rate (U3): 7.6% versus 7.5%, from 7.5%

[/li][li]Underemployment Rate (U6): 13.8% from 13.9%

[/li][li]Participation Rate: 63.4% from 63.3%

[/li][/ul][/B]

Yesterday, it seemed that traders were positioning themselves for a poor print: weaker USDJPY, stronger US equities, lower US Treasuries yields. Today, equities are up, the US Dollar is gaining, and US Treasuries yields are higher. This looks like a repositioning for renewed speculation of the QE3 taper – certainly, the data doesn’t lean that heavily in either direction.

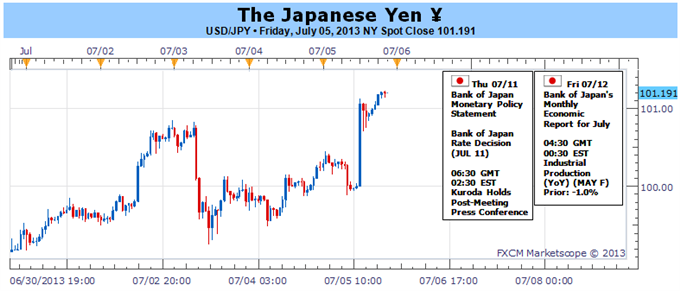

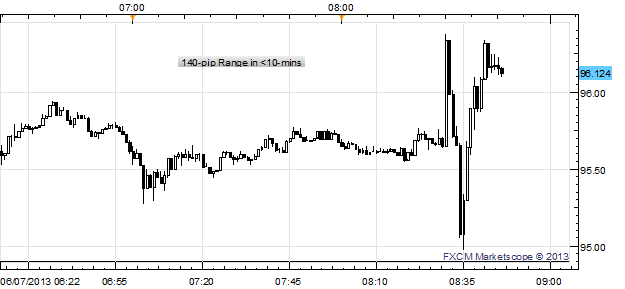

[B]USD/JPY 1-minute Chart: June 6, 2013[/B]

Following the release, the USD/JPY gyrated violently, trading from ¥95.75 to as high as 96.38, before plummeting to 94.38. But within 15-minutes, the USD/JPY had surged back to 96.12, at the time this report was written. US Dollar strength was observed across the board, with the EUR/USD falling to $1.3205, and the AUD/USD plunging back to the weekly lows near $0.9440.

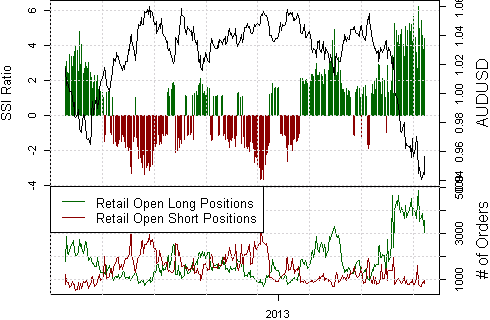

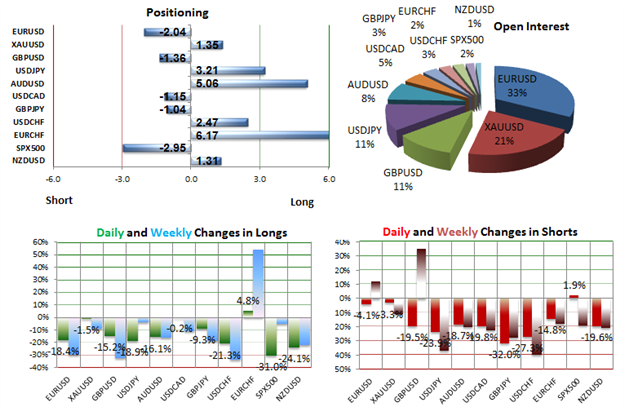

It’s worth noting that overall, traders are still long US dollar, which means today’s boost after NFP could be short lived. The one major pair where the Speculative Sentiment Index (SSI) supports this mornings tendency of US dollar strength is AUD/USD. The trading crowd has grown further net-long the Aussie from yesterday and last week. The combination of current sentiment and recent changes gives a further bearish trading bias.