[U][B]An interview with John Kicklighter[/B][/U]

[B]•This week happens to be a relatively busy week of US economic data releases that includes the GDP report, an interest rate decision, home sales data and the durable goods report. What do you feel will be the one or two most important events and themes to pay attention to for the week and for the rest of January?[/B]

All of the economic data that is scheduled for release through the immediate future will play a role in shaping expectations for the relative health of the United States – an important consideration when there is a very real threat of recession for many of its most prominent counterparts. However, most individual indicators (like the housing data, durable goods orders and for that matter, probably even next week’s NFPs) will not significantly alter the larger consensus trend. The exception is the first reading of 4Q GDP. This figure can confirm or deny the market consensus, and catching market participants off guard on a big theme like this is a rare enough event that its impact is leveraged. Tapping the more elemental consideration of risk/reward, the FOMC decision could also be a market mover as it will offer a better framework for further stimulus and the eventual withdrawal of easy money. This particular meeting is a unique event as they will start producing interest rate forecasts along with their updates on growth and policy bearings. These are the known and definitive considerations. Real impact potential though comes from the unknown – speculation of QE3 and progress on the most recent ‘hope revival’ for the euro.

[B]•The EUR/USD has now broken above the 1.30 level this week in trading. Do you feel the EUR/USD can sustain this momentum at these levels and perhaps ascend higher?[/B]

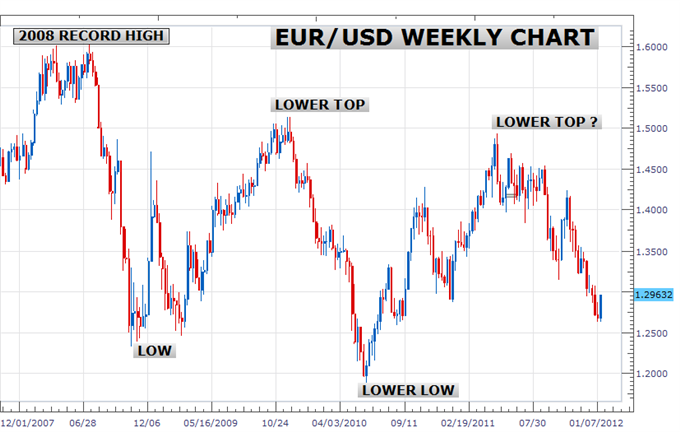

From a purely fundamental perspective, I think the euro has no business posting a meaningful advance. That said, this isn’t an academically-based fundamental world. Sentiment determines when a currency needs to be repriced. That being said, the market will itself to be caught up in the hope that additional stimulus is coming through for the Euro-area and that the Greek situation will be reconciled because the short-side is temporarily oversaturated. Though not a full representation of the spot market (due to difference in market depth and participation) the COT report of net speculative interest in Euro futures set a record level of shorts through the week ending Tuesday. Often, when we reach these extremes, it is a sign that one side of the market has been exhausted and a correction would be easier to facilitate. Given the depths the euro has plunged on an exchange rate and futures positioning basis, a bigger rebound wouldn’t be too hard to facilitate.

[B]•Seeing the CFTC futures speculators data showed that specs were still very euro-bearish last week, do you feel we could perhaps see a change in sentiment (a bottom reached and/or a short squeeze?)?

[/B]The CFTC’s Commitment of Traders report measures open positions to the Tuesday of that week. Therefore, the record net short exposure reading that we were given was not representative of the big Euro rally on Wednesday and Thursday. There is a good chance that exposure will see a correction with the next reading to account for the recent change in EURUSD’s bearing (even if it is temporary). That said, a quick reversal (in either price or extreme positioning) doesn’t necessarily guarantee a larger trend reversal. It’s important to remember in these times that there are corrections in larger trends.

[B]•What do feel is propelling the AUD/USD and the NZD/USD higher at this point? They are now respectively trading at their highest levels since October. Despite the AUD and NZD’s correlation to risk, these two pairs have largely avoided the euro’s slide of the last few months.[/B]

The euro itself is not a good representation of risk. We have seen the correlation between EURUSD and the S&P 500 (my favored gauge for risk appetite) deteriorate significantly over the past week. Anything can be a catalyst for broader risk aversion, but it doesn’t guarantee that everything and anything will do it. Through the euro’s recent slide, we have seen demand for equities slowly but steadily chop higher to five month highs. It is this acceptance of risk and appetite for higher yield that is encouraging capital to flow over to the higher yielding currencies.

[B]•The USD/JPY has been trading in a relatively tight range since the beginning of the new year roughly between 76.50 and 77.50. Do you see any catalyst upcoming that might be able to allow a breakout of this range? Likely more of the same sideways action?[/B]

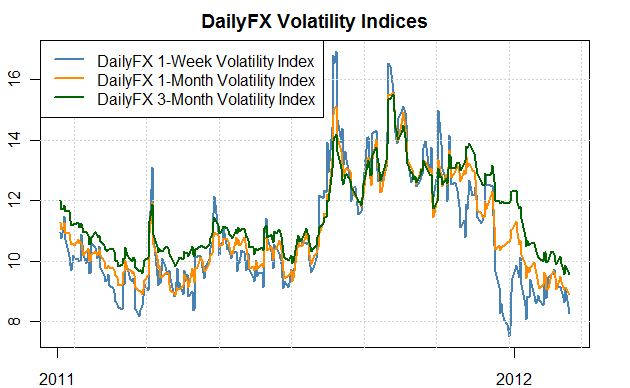

The US dollar and Japanese yen are frustratingly, evenly matched as safe havens – that is in tolerable market conditions (should the very stability of the world’s financial markets come into question, capital will move over to the US dollar and its Treasuries, no questions asked). With volatility behind risk trends smoothing out, the need to favor a particular low-yield and deep-market currency diminishes significantly. Clearly, a crisis of global proportions could encourage a shift to the safety of the US market. In the absence of that overwhelming catalyst, we still have the possibility of BoJ intervention (though it seems they are looking at both EURJPY and USDJPY for inspiration).

[B]•As we have entered a new year, do you have any predictions for winners or losers over the first half of the year in terms of specific currencies and trends? Any other markets you feel may have a bearing on the major currencies?[/B]

Given the heights equities (and exposure to risk in general) have marched to, a bigger correction in long-risk exposure is highly probable. That means, high yield currencies, equities, speculative commodities, and high-yield paper are at risk of a deep correction. And, if all come under significant enough pressure at the same time, we could possibly see the funding markets freeze up; which is a crisis unto itself. In a regular risk aversion scenario, we can see the US dollar and Japanese yen advance for currencies while government paper and money markets for the US, UK, Germany and Japan swell. After such a down leg, we could see one of two scenarios. A short-term downdraft would see the Fed or some other equally dedicated policy authority step in with an artificial booster in the form of stimulus. Otherwise, a longer deleveraging would eventually flag and send too much capital to the sidelines – and the void would eventually need to be filled so market participants can make money and possibly take advantage of considerable discounts (after a meaningful reduction in cost).

[I]Source: Analyst Interview: John Kicklighter on Whether the EURUSD Rally Lasts | DailyFX[/I]